Quantitative Easing = Counterfeiting Quantitative Easing = Counterfeiting

Bob Moriarty

Archives

Dec 20, 2010

I love to read. When possible I read a book a day. I can’t do that, of course, at home or Barbara would be accusing me of being a lazy trout. I’m certain she would find something better for me to do.

But when I’m on a plane I can read to my heart’s content. Barbara on the other hand believes that plane journeys are a wonderful way to make new friends. She dresses up to travel. I wear whatever I happen to have on. Who wants to meet new friends?

So an eight-hour plane journey might be a burden to others but I get to catch up on my reading. Lately I read an interesting book about hyperinflation in Germany in the early 1920’s titled, “When Money Dies. . .“

It was a fascinating book because I think everyone familiar with the time would intuitively understand that printing too much money was the basic cause of the hyperinflation that destroyed Germany and built the foundation for Hitler and World War II.

We are doing the same exact thing today but we call it “Quantitative Easing.” Strange term for printing money but I suppose if you confuse enough people with misleading language, you can get away with anything. It’s nothing more than printing money and the most accurate term for it would be counterfeiting.

The financial world as we know it is in a slow motion crash that few Americans recognize. If you want to see the near future, watch the riots in Italy, Greece and England, soon coming your way. The US is so far beyond bankrupt that anyone who can count understands it even if they ignore it.

Dr. Laurence Kotlikoff, professor of Economics at Boston University estimates the current real debt of the Federal government at $202 trillion dollars. That’s on an economy of $14 trillion. The Fed is doing everything possible to print money so we can pay the debt off in cheaper dollars but we know how that works out in the end, hyperinflation and collapse of the economy. The government is already prepared for civil disorder. It’s going to get ugly.

Gold and silver have been on a tear since August. Silver went from $18 an ounce to just over $30. Gold bounced from $1190 to just over $1420. Many gold companies have doubled or tripled their share prices. Everything has been rocketing; the Dow is up over 15% since the end of August.

The end is nigh. I’m pretty shocked the world made it through 2010 without a total financial collapse but I don’t see it making it through yet another year. Europe is coming apart; the recent riots in Athens are a signal of what is coming to a neighborhood near you. The mob has gotten so used to free meals that they will kill to continue a system that we cannot afford.

I see another bounce higher in the metals and shares and then a correction. It’s pretty typical of this time of year. People get way too excited and the market dashes their hopes before climbing again. We had a top in December of 2004, we had a top last year and the market is just as frothy now. Bob Hoye is calling for a major correction across the board starting in the next month or so and he was the guy who got it the most right in 2008.

I recently visited a project that I should have been writing about years ago. Golden Phoenix Minerals was an early advertiser on 321gold. The company was the product of a guy named Mike Fitzsimmons who bought the Mineral Ridge gold project out of bankruptcy in 2000 for $250,000.

I didn’t know it at the time but Mineral Ridge was a giant gold district in Nevada half way between Las Vegas and Reno. The district had historical production of over 680,000 ounces of gold prior to being shut down in 1942 due to World War II. Gold was originally discovered as early as 1864. Under various companies there were over 58 miles of underground workings. The mine is at the heart of the Silver Peak mining district, once one of the highest grade deposits in Nevada.

In 1989 the predecessor to GPXM decided to create an open pit, heap leach project out of a mine that had been out of production since 1942. It was a giant and expensive mistake that put them into bankruptcy years later. The gold at Mineral Ridge, and it’s a pure gold deposit with no silver or copper at all, is surrounded by iron pyrite. It’s encapsulated, not attached externally so leaching was never very effective because the ore would have to be crushed and milled. That basic miscalculation drove the first company into bankruptcy and when Fitzsimmons bought the company from the bankruptcy court, he continued the same mistake.

He might have succeeded if he had listened to his technical people. The gold is high enough grade that it really demands a mill and flotation or leaching. He didn’t listen, expenses went through the roof and he had to put the mine into care and maintenance in 2004.

Fitzsimmons did what the management of many juniors does, he went out and started collecting Beanie Baby projects, just to keep the chumps contented. He entered into a deal with Win-Eldridge (WEX-V) on the Ashdown property in 2004. I was familiar with the management of both companies and it was a real question of which was the most incompetent and I never figured it out.

One of the geos at GPXM went through the data after they did the deal and realized the project wasn’t really a gold project. It was a moly project with grades of up to 7% that could have been put into profitable production at any time if someone had realized the real value was in the moly, not the gold.

At the time of the deal, moly was about $14 and the very worst thing for both companies happened. The price of moly shot to the moon and all of a sudden moly was $40 a pound and climbing. Shareholders of each company wanted to know why the companies didn’t go into production with some rock having an in situ value of $5600 a ton.

If you want to see incompetence in action, watch an exploration junior try to get into production. The JV flounder, expenses went on and on and no moly was produced. Finally the GPXM shareholders held a revolution and fired Mike Fitzsimmons. WEX simply floundered on for many years. The moly project finally got into production in 2007 and was growing until the financial debacle of 2008 whacked the price of moly to under $10.

By then, the share structure at Golden Phoenix had pretty much blown sky high and it was clear the company needed to change direction. The GFC of 2008 made the company realize they needed direction and a more proactive management style. Tom Klein stepped in as a director in December of 2008 and eventually became CEO in early 2010.

Tom Klein thinks that it’s better to make things happen than to let them happen. The moly JV with WEX had become a noose around their neck; they weren’t making money but had constant battles because of the structure. Tom Klein took the bull by the horns and gave control back to WEX of the Ashdown project in return for a secured $4.2 million dollar note with payments to begin in April of 2011. WEX either produces and pays GPXM or gives the project back to GPXM. That was a good solution.

Tom turned around and did a deal with Scorpio Gold, run by Peter Hawley on the Mineral Ridge Gold Project in mid-2009. It called for a 70-30 JV with Scorpio paying $3.75 million for the mine and mill and an additional 7.8 million shares of Scorpio Gold. GPXM has a 30% carried interest and Scorpio has the option of buying out the remaining shares based on a predetermined payment agreement.

Basically what Tom Klein has done is cleared the deck so he can move the company forward. It should be clear from the actions of the last 10 years, the company simply didn’t have the bandwidth to put a gold project and moly project into production at the same time. Peter Hawley had the gold production experience and is saying Mineral Ridge will be producing gold in early 2011. He has re-laid the leach pads, crushed the existing ore into a fine grind and is making plans for a full mill.

I have my doubts about Win-Eldridge management. I don’t think they can perform and if they don’t GPXM will get the project back.

Tom is saying he wants to be a royalty company. He picks up projects, advances them and does deals with production companies to get them into production. The plan sounds good but obviously only time will tell the tale. He wants to retain a 30% interest in the production projects.

The Mineral Ridge Gold mine and the Ashdown moly projects are not the only things on GPXM’s plate. In mid-2010 Tom Klein signed deals on two prior production silver and gold project adjacent to Mineral Ridge. GPXM has an option to earn an 80% interest in both the Vanderbilt silver/gold project and the Coyote Fault gold/silver project near the Mineral Ridge mine in the Silver Peak district.

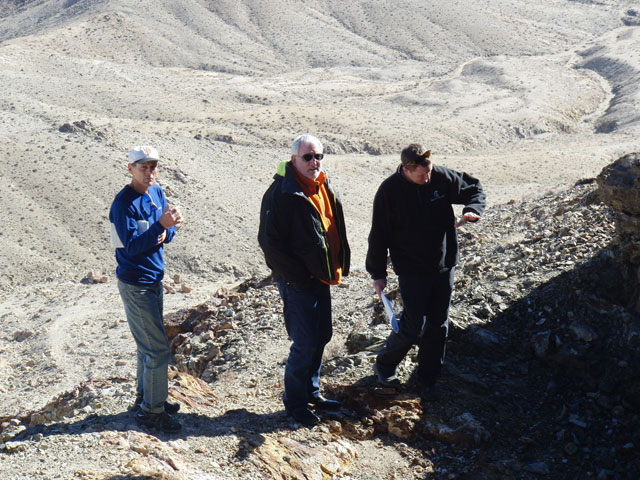

On the trip two weeks ago with Thom Calandra and Gordon Holmes, we knocked rocks off veins at the Vanderbilt mine. They looked pretty juicy. That’s loaded with east drill targets visible from the surface. Coyote Fault is another prior producer with easy drill targets that would give potential investors a sniff of the potential.

At this stage, GPXM is still trying to clean up the mess left by years of inadequate management. Tom Klein has embarked on an aggressive 24-month program of picking up and advancing more projects in Nevada, Ontario and Peru. The existing share structure is a disaster with almost 250 million shares outstanding.

I personally would like to see a share restructure and to get the number of shares down to a more reasonable number. Tom has indicated a desire to list on a better exchange; the Bulletin Board is pretty low on the pecking order for most investors.

I expect a major correction in all markets starting soon. We have only just entered the Global Financial Crisis (GFC) with the US still firmly in denial and totally bankrupt. There is far more debt than assets to pay for them and no one wants to restructure that debt. There will be enormous potential for opportunistic investment for someone quick on his feet that understand just where we stand. Tom Klein says he can do it and only time will tell the real tale. He at least does understand the problem and that’s better than management of most of the juniors.

I liked his story enough to invest in a PP that I can’t sell for at least a year. I think it’s a good story and he will either succeed wildly or fail in great glory. Right now you can flip a quarter.

GPXM is an advertiser. I am biased as I will do very well should he succeed and the share price increase. The number of variables that could affect the price of the shares is giant and with 247 million shares outstanding, don’t expect them to double next week. It’s a crapshoot but so is investing in any junior. At least it’s a crapshoot with good odds and a giant potential payoff.

We don’t share in your gains so we don’t want to know about your losses. I don’t get paid for my opinion and I don’t charge you to read it. We hope you gain but all investing is risky.

Golden Phoenix Minerals

GPXM-OTCBB $0.19 (Dec 17, 2010)

247 million shares

Golden Phoenix website

###

Bob Moriarty

President: 321gold

Archives

321gold Ltd

|