|

||||||||||||||||||||||||||||||||||

The Biggest Little Silver Company in the WorldBob Moriarty Over the past year I have visited some extraordinary properties. Especially silver properties. Contrary to all those self proclaimed silver "Gurus" silver isn't about to run out. There is no shortage of silver, only a shortage of accurate information about silver. Silver has been in a bear market since the Hunt brothers ran the price to $50 in 1980 from $5.50 in 1975. We tend to look at silver based on the latest price moves but when you see silver today at $9 and then consider it was $5.50 in 1975, it's pretty easy to understand that it hasn't been worth developing silver mines for the last 30 years because of declining prices. Rather than a shortage, silver has been in surplus since 1940 when the US alone held over 6 billion ounces in reserves for a population of only 200 million. Why did we need 30 ounces of silver per man, woman and child? Answer: We didn't. And we've been dumping it on the market ever since. And for all the wailing and anguish about some mythical silver shortage, India and China have vast reserves of silver built up over 450 years. India alone has somewhere between 6-8 billion ounces of silver. They call it "poor man's gold," in India and every family, no matter how poor, has some silver in savings. China's been dumping it on the open market for years and that's why silver hit a 5,000 year low in real dollars in November of 2001. Those familiar with 321gold may recall me calling a bottom for silver at $4. How many of the silver "Gurus" can say the same? But silver isn't in a bear market any longer. Demand has caught up with supply. Prices have been in a bull market for over four years now. And a few Canadian silver juniors are about to set the silver mining community on its ear. If you look at the price of copper, lead, zinc, moly, iron, oil, uranium, natural gas or gasoline it's pretty obvious that not only hasn't silver kept up with inflation, it hasn't even kept up with its peers. So where is the mythical shortage? And please don't feed me the manipulation mantra. It's amazing how when people have been dead wrong in everything they have said about a commodity for years they fall back on the "manipulation" mantra. Well, folks, here's how it works. Price is always right, opinions are often wrong. Two things will drive the price of silver higher relative to other commodities. The first is the silver ETF. I find it interesting that the biggest purveyor of manipulation-conspiracy nonsense on the web immediately fell on the gold ETF with a blood soaked dagger. Of course no one bothered to say that the author of all the venom about the gold ETF had a conflicting product which the WGC had rejected and was as biased as he could be. The history of the gold ETF has been a wild success and it's easy for Americans to buy gold today. The gold ETF is the best thing that happened to gold in the last 50 years. The same will be true of a silver ETF and I can't for the life of me see why or how the SEC could approve a gold ETF and fail to approve a silver ETF. Much has been made about the Silver Users Association being against the silver ETF but the SUA is simply a users group with a vested interest in cheap silver. Of course they want it turned down. Big deal. The SUA doesn't run the universe. While the "Gurus" are wailing about the SUA, they totally forget to mention how hard it is to buy physical silver. When I was a kid, and I'm 59 now, it seemed there was a coin and stamp dealer on every corner. I collected stamps and while we lived in about 20 different places when I grew up, I can't remember a time when there wasn't a dealer within an easy walking distance. I still go in to a coin store, actually that's one of my little quirks, I go every Saturday afternoon when I'm in town. And if we have houseguests or business meetings I drag the visitors along, too. And if I'm going on a trip I leave a bit early and visit the coin store on the way to the airport. It drives Barbara crazy. I see the same guy in the same place that I have done for years. There is always something John has at the right price. I was there yesterday and I traded a bunch of Double Eagles for 25 Queen Victoria sovereigns. We got to talking about silver demand and supply. He had a couple of silver 100 ounce bars but I could have bought every ounce of silver he had in stock for less than three thousand dollars. John told me that the other dealers in town won't even stock silver bars, there is so little demand, they sell them all to him. There is neither a supply or a demand for silver bars in Coral Gables. So I went to look at eBay where you can buy everything. I fed in 100 ounce silver and it came up with 42 listings. Some of the listings weren't even for 100 ounce bars but even then, 42 of the 100 ounce bars is only worth about $40,000. Actually, and keep this in mind when you are listening to some guy spout off about silver going to $100 an ounce while everything else stays the same, you could have bought a 100 ounce silver bar at a discount. If silver was really in such shortage, it would sell at a premium. That tells me we really need a better way to buy and sell silver and it sure seems to me like the way to do it is via a silver ETF. It worked with gold and it will work with silver. For all of the hot air used up talking about the price of silver, for today it's both hard to buy and hard to sell for the average guy. A silver ETF will increase demand for silver. And the price. And the second price driver for silver that I see in the future is us going back to a gold standard. Few Americans realize the value of the dollar has been cut in half during the reign of Alan Greenspan. He's a guy who understands the importance of gold in a financial system. His heirs haven't a clue and with a President determined to destroy both the value of the Dollar and our Republic, owning some gold and silver seems like a prudent thing to do. But in a gold standard, which I believe is inevitable, the highest demand would be for silver as a monetary metal. With all of the world's currencies in a seeming rush to the bottom, gold may well present the only solution possible. And silver is what we will be using for day to day transactions. There isn't enough physical gold around to use as pocket money. So while I totally discount manipulation and conspiracy as driving factors in the price of either gold or silver, I both buy them and suggest others buy them on the basis they are both cheap and going to be in far higher demand in the future. Our government isn't the only source of stupid economic policies on the planet. Its just one of many.

In Bolivia, militant mine workers demanding better conditions and higher pay, led a revolution in 1952 which led to the nationalization of the mining industry. All mines were turned over to a Bolivian state-owned mining company called Corporacion Minera de Bolivia or Comibol for short. (Pronounced appropriately Commie-Ball). The Comibol labor force grew from 29,000 workers in 1953 to 36,000 in 1957 as earnings dropped to half of what they had been in 1952. The percentage of miners fell from 82% in 1952 to 52% by 1959. Wages fell from $86 in 1952 to $42 in 1956 and only rose to $70 by 1970. The decline in wages was caused by under capitalization and under investment which in turn caused large declines in productivity. The mine we are concerned with today is the Pulacayo mine in the Altiplano of Bolivia. Discovered by a Spaniard named Mariano Ramirez in 1833 but not brought into large scale production until the introduction of French capital in 1873, the mine has produced 678 million ounces of silver, 200,000 tons each of zinc and lead over its history. This production was second in Bolivia only to the vast silver deposits at Potosi, the largest silver mine in world history. The Pulacayo mine was so important in Bolivian history that the vast silver revenue from the mine paid for the first railway line in Bolivia connecting the mine to the port of Antofagasta in Chile in 1888. As late as 1951 the mine was producing 5 million ounces of silver and silver equilivant values of lead/zinc/copper.

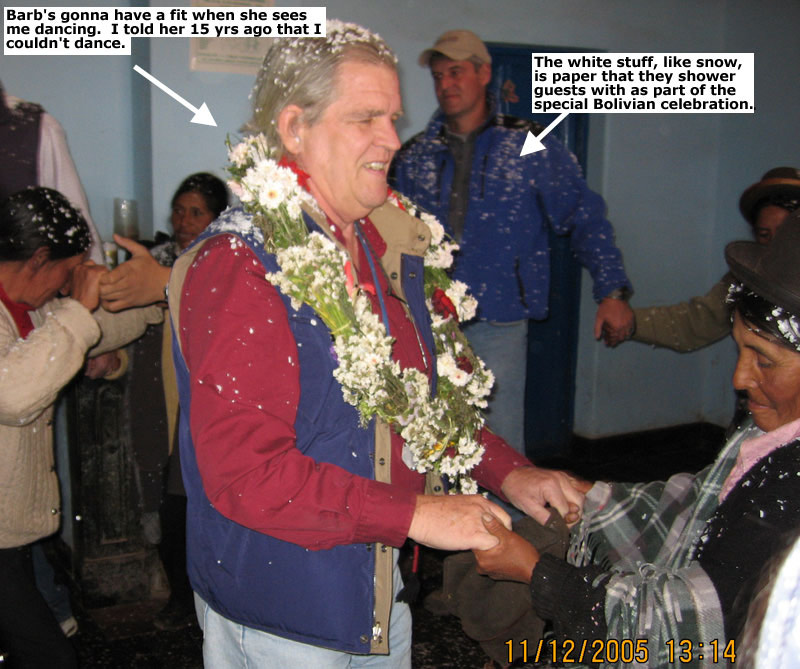

I went to Bolivia with John Carlesso President of Apogee Minerals [symbol APE.V - website] and Rick Irvine, VP of Operations recently. We spent a day at the Pulacayo-Paca project and it was an eye opener. First a brief history. One of the assets I use a lot to get a feel for the value of drill results can be found on the KitcoCasey site. If you go there and click on the link which says, "Calculator: "What's That Rock Worth?" it will bring up a page which looks like this. click Image 1. Comibol shut the Pulacayo mine down in 1958 because they couldn't make money. The average grades mined at the time were 250 g/t silver, 10.5% zinc, 1.5% lead and .9% copper. Here is what those grades are worth in gross metal values per tonne. click Image 2. That's worth $320 today which is extraordinary. Sergiomin, which is the Bolivian equilivant of the USGS, estimated the mine reserves at 10 million tonnes of 96 g/t silver, 2.6% zinc and 1.3% lead ore. That's not a 43-101 resource but it will give the reader an idea of just how big this deposit still is. click Image 3. If you figure average mining and processing costs of maybe $40 a ton, that figure of $88 a ton ore is pretty rich and pretty large. If you convert the lead and zinc to a silver value, it's equal to about 100 million ounces of silver in a resource. In 1997, like Mexico before it, Bolivia revised its mining code (Codigo De Mineria) to promote private ownership of mining interests. It only took them 45 years to realize worker control of mines doesn't work. The miners make less money and mines get shut down. So Apex Silver of Denver did a deal with Comibol and took over control of the Pulacayo-Paca project and began drilling. Pulacayo is the actual existing mine. The mill is long gone, it was removed over 45 years ago, but Comibol operated a machinery shop building equipment for their other mines until a few years ago and a large community still surrounds the mine. Paca is a open pit, bulk mining project located about 4 km north of Pulacayo. Apex drilled about 4300 meters in the Paca area and developed a 75 million ounce resource suitable for open pit mining. (much lower cost than underground mining). Pulacayo is nothing short of incredible. While we were there, we were greeted by everyone in the surrounding village for a formal party complete with a loud but out-of-tune brass band. We were welcomed with piles of cut up paper dumped over each of us, a standard mine worker dinner, garlands and a dance.

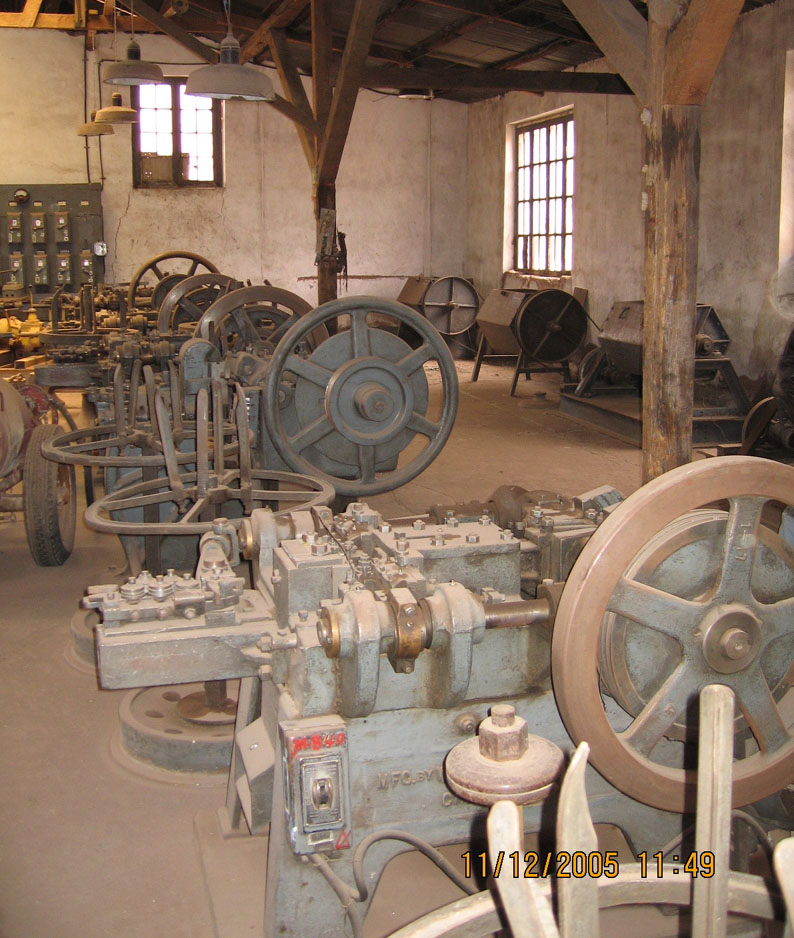

The workers remember the machine shop and it's important to them that it be reopened. We walked around it. I was amazed. It was if the workers walked away a few weeks ago and other than some bird droppings on some of the machines, everything was still ready to use. There were stacks of iron wire ready to be fed into the nail making machines. I couldn't understand why Comibol didn't just tell the miners to go into the nail business. They had two warehouses filled with nail wire and were literally starving while all the machinery sat idle. If it were me, I'd try to figure out if anyone in Bolivia needed some nails. [Editor's comment: 321nails.com?]

Apex Silver has their hands full developing the San Cristobal mine about 40 KM away from Pulacayo. So this past September, Apex and Apogee did a deal on the Pulacayo/Paca property. The terms of the joint venture call for Apogee to earn a 60% interest in the property by spending $1 million US in exploration within three years and completing a bankable feasibility study. Apex Silver can backin to 60% of the project by developing the property to production leaving Apogee with 40% ownership of an existing very rich silver/lead/zinc mine. Frankly I think Apogee got the best part of the deal by far. Not only because silver has rocketed to $9 while lead and zinc set new record prices daily but I have looked over the San Cristobal project which Apex is in the process of putting into production. It sure seems to me like Pulacayo/Paca is a hell of a lot better and richer project than is San Cristobal. Apex is fooling around with a giant project with low grade ore and lots of potential pitfalls when they could have easily and cheaply put Paca in production of 5 million ounces per year. But Apogee landed this fish and is running with it. We visited the property and were greeted with open arms by the local workers who have stuck around for years in the belief someday someone would reopen the mine. In fact, they held a very special welcoming ceremony and a dinner AND dance). I have little doubt Apogee will reopen Pulacayo and increase the 100 million ounce resource in the process. And the Paca project is such a zero brainer that I believe they will be doing a feasibility study just as soon as they can drill it out.

Just a short drill program conducted by Apex showed 75 million ounces of silver at the Paca open pit project. So using 175 million ounces of silver for a resource may not be a 43-101 reliable resource but will give an investor an idea of the potential. Apogee will have in the end either 40% of a producing mine or 60% by investing money of their own and taking it to production. When similar silver producers are selling for far higher valuations per ounce silver. Fortuna gets $1.44 per ounce of resource, Endeavour Silver gets a rich $2.67, First Majestic gets $2.57 and First Silver gets $2.07 per ounce. Those figures suggest a value of $280 million dollars is possible down the road just based on Pulacayo and Paca for Apogee.

Lest the reader believe these trips are all work and no play, on the last day of the visit we were supposed to be picked up at 9:00 AM in the morning for the flight back to La Paz but the plane was going to come in four hours late so we rented a van and drove 100 KM into the center of the world-famous Uyuni Salt Lake to visit the island of the cactus. The lake is the most visible structure on earth visible from outer space and continues to grow each year since it stands in a giant basin. There is even a salt hotel with furniture made of salt.

There is a lot more to the Apogee in Bolivia story. I didn't get to visit the property while I was in Bolivia but Apogee is busy drilling at the Buena Vista project some 60 miles northeast of Pulacayo in the Potosi Department with excellent results.

But the real home run potential in my mind is at the La Solucion Mine near La Paz. In July of 2005, Apogee acquired an option to earn up to 51% of the La Solucion Project in exchange for a $1.3 million dollar work commitment over three years and by paying $1 million in cash or shares to the existing shareholders. Once the 51% is earned, Apogee can buy out the remaining 49% by paying an additional $1 million in cash or shares. The La Solucion Mine is an existing 110 TPD mine with grades of 101 grams silver, 6.99% zinc and 1.84% lead. If we use the handy KitcoCasey calculator again, we see that is $175 ore or about 20 ounce silver equilivant. The mine has been in production for 14 years but has never been properly expolored due to financial constraints on the owners. So they did a deal with Apogee. Apogee has done some figures to increase production to between 1000-2000 TPD. click Image 4. With a capital cost of about $19 million US, Apogee can increase production at La Solucion to 1000 TPD with production of about 7 millon ounces of silver equilivant per year at a cash operating cost of $3.39 per ounce. For about $28 milllion dollars, Apogee can do 2000 TPD and do the same as 14 million ounces of silver at a cost of $2.63 per ounce. While we were at the La Solucion Mine we drove down strike to Apogee's current drill location. They had just completed drilling just off the portal. I saw some of the core and it looks very juicy.

The 3 veins run on surface for 10 kilometers. And I just came back from Mexico where I saw the value of a 25 KM silver/lead/zinc vein at Guanajuato when I visited the property for Great Panther. My suggestion to Apogee was to extend the strike for a good distance so at least they had some idea of what they were dealing with. Is the project a 200 million ounce project or a billion ounce out of the ballpark silver home run? So they are drilling 5 kilometers down the vein. All they have to do is come up with the same grades and widths and they could be sitting on a 275 million ounce deposit. And they are drilling it today with results to come out in less than a month. I know it's possible. It's not a big deal if they don't come up with the results but if they do hit big, they will be company-making drill results. What Apogee and Great Panther and Fortuna are doing is nothing more than extending the business model first developed by Endeavour Silver. Each of these four companies has the potential to make it into the ranks of the top five silver producers and I expect to see several if not all of them make it into those ranks. By and large the big projects being picked up today are falling into the hands of juniors and I believe the big stock returns will not come from the Silver Standards and CDEs but rather from the tiny market cap companies today with big aspirations. I like seeing the competition. All of these companies have good projects and good managements. We will see in a couple of years just how good they really are. But the big five in silver had best check their sixes because there are bandits in the air and if they don't watch out, they are going to get shot down. I happen to believe Apogee is sitting on the very best silver properties I have seen. That isn't to diminish any of those I have seen but Apogee has world class potential. It will be up to management to measure up to my opinion of the properties. They have the material to work with. Apogee Minerals is an advertiser. They have not paid for this article and it is my opinion and only my opinion. As always, we want to remind investors they are responsible for their own investment decisions. We own shares in Apogee. I am biased.

Bob Moriarty 321gold Inc |

Apogee

has an absurd valuation. The company was selling for about $.40

a share when I was in Bolivia and is selling for $.52 a share

today. There are only about 24.6 million shares outstanding

for a market cap of just over $10 million Canadian. The figure

of 100 million ounces of silver at Pulacayo is modest, it's another

giant existing old Spanish silver mine with hundreds of millons

of ounces of prodution and a high probability of more hundreds

of millions of ounces of production in the future. The mine should

still be in production a hundred years from now. This isn't just

another silver mine, it's a dynasty.

Apogee

has an absurd valuation. The company was selling for about $.40

a share when I was in Bolivia and is selling for $.52 a share

today. There are only about 24.6 million shares outstanding

for a market cap of just over $10 million Canadian. The figure

of 100 million ounces of silver at Pulacayo is modest, it's another

giant existing old Spanish silver mine with hundreds of millons

of ounces of prodution and a high probability of more hundreds

of millions of ounces of production in the future. The mine should

still be in production a hundred years from now. This isn't just

another silver mine, it's a dynasty.

They have established

an office in La Paz with 20 staff including 10 graduate geologists.

By mid-2006 they expect to have outlined over 200 million ounces

of silver resources with an acquisition and capital and operating

costs of no more than $3 an ounce.

They have established

an office in La Paz with 20 staff including 10 graduate geologists.

By mid-2006 they expect to have outlined over 200 million ounces

of silver resources with an acquisition and capital and operating

costs of no more than $3 an ounce.

{kind=link}

{kind=link}

{kind=link}

{kind=link}