|

||||||||||||||

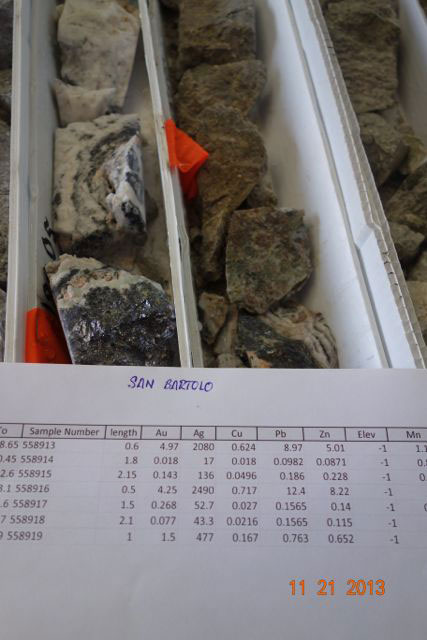

Mexico’s Newest Old Silver MineBob Moriarty It’s rare that I go on a tour to a company that I have never heard of, but it happened when I went to visit Sierra Metals (SMT-T) a week ago. I’d make the pitiful claim that I didn’t know them because they changed their name a year ago from Dia Brias except for the fact I had never heard of Dia Brias either. In any case, right under the radar screen of most investors and a few writers, a junior has transitioned into a significant producer of silver, copper and other base metals in Peru and Mexico. I went to see their major Cusi project in Chihuahua State, Mexico. Perhaps it’s time for another name change because they more correctly should be named Sierra Silver at the end of the day. A Spaniard named Antonio Rodriguez first discovered the Cusi Mining District in 1687 and began mining. In the early years the mines of Cusi produced 50,000 ounces of gold and as much as 50 million ounces of silver from a mere 500,000 tons of ore. It is estimated that as much as 200 million ounces have been produced in the 320-odd years since then. Sierra Metals picked up the silver district in mid-2006. The Cusi mine is a silver deposit with credits of lead and zinc. The company owns 100% of the mine. In M&I resources, they show 7.3 million ounces of silver and in Inferred, they show another 14.6 million ounces. The company is ramping up production now. It’s a high-grade epithermal deposit with silver grades up to 20 kilos per tonne. Sierra Metals is producing silver at Cusi at a cost of $14.96 in Q3 2013 and expect the cost to go down to $10.90 net of credits by 2014. They process the ore at their wholly-owned Malpaso Mill some 37 km away. Eventually, depending on the price of silver, they expect to build a much higher capacity flotation mill near the Cusi District. Currently they mine and mill just over 300 TPD (tons per day). SMT expects to release a new 43-101 resource for Cusi in Q1 2014 along with a Feasibility Study. They intend to ramp up production to 600 TPD in 2014. The production bottleneck today is the mill. With all the different veins and adits on the ground they own, they can mine an almost unlimited number of faces at the same time. The plans for a new mill have been put on hold until silver prices improve. All of the work they are doing today is part of a grand design many years in the making. Sierra used to be a simple junior exploration company with the intent to go into production when they could. Their first major mining project was the Bolivar mine in Chihuahua producing 300 TPD since 2005. Originally they shipped the ore via rail line for processing at Malpaso but they commissioned the Piedras Verde plant in October of 2011. Piedras Verde was running at a capacity of some 1000 TPD. The company has just increased capacity to 2,000 TPD this last month. At Bolivar 84% of the revenue comes from copper and base metals, 16% comes from silver. The company expects to produce 16,000,000 pounds of copper and zinc in 2014 and 330,000 ounces of silver. Margins are excellent even with today’s low prices, showing some 41% to an estimated 62% in 2014. For an underground mine, their costs are excellent. After costs of just over $50 a tonne in 2012, they have lowered costs per ton to about $43.50. That’s pretty low. Bolivar has 428 million pounds of copper equivalent in the M&I category and an additional 100 million pounds in Indicated. Success breeds success so Sierra bought the 82% of the Yauricocha Polymetallic Mine in Peru in 2011. They paid $286 million for the deposit. They are writing off the cost of the mine over a four-year period so the non-cash charge makes it look as though they are not nearly as profitable as they really are. Yauricocha in Peru is running at a capacity of 100,000 tonnes per month with negative cash costs for silver at $11.25 per ounce. [corrected] Bolivar in Chihuahua in Mexico mines and mills 30,000 TPM (tonnes per month) and is being ramped up to 60,000 TPM shortly. Bolivar has cash costs for copper at $1.73 a pound. Cusi runs about 16,500 TPM and will be ramping up eventually to be a primary silver mine and will produce the bulk of their income. Yearly sales were just under $180 million last year and have a run rate of about $160 million this year. Net income last year was $48 million prior to the non-cash write-off of the Yauricocha Mine of $76 million. Revenue for the first half of this year was $79 million with net income of $21 million prior to the non-cash charge of $34.5 million for Peru. The company is tightly held and this has proven to be a good thing this year with many great companies being hammered down 75 to 90%. SMT is down a mere 30% from its high point at $2.96. Sierra Metals is far more of a money management issue than of mining. The company has made major progress over the last 8 years getting into profitable production and resource expansion. But they have weathered two giant crashes in the price of silver and copper. Silver went from $21 an ounce in March of 2008 to below $9 an ounce in October of the same year. Copper went from just under $4 in early 2008 to $1.40 in the fall of 2008. Silver has crashed again from about $49 an ounce in April of 2011 to $18 and change at the low in late June of this year for a 62% drop. These wild swings in prices have decimated the share price of most junior mining companies. Most pure exploration companies are struggling to keep the doors open as investment money dries up. Sierra Metals simply ignored the market and kept right on trucking. To the extent that not having institutional ownership has proven to be a giant asset for them. No one has been dumping their shares to pay off disgruntled investors in a fund. Given the absolutely dismal state of the markets, I have to give kudos to the management and staff of Sierra Metals. They are planning for the future and executing a well laid out plan from the past. If you are a silver bug you need to put Sierra Metals on your radarscope. Their leverage to silver is excellent and higher prices for the metal will immediately flow right to the bottom line. The only thing I would change is the name. They are going to be a big silver producer in a couple of years. I expect them to be a big and profitable silver producer. If you have the name, you have to act the part. I don’t own Sierra Metals but I am no less and no more biased than I ever am. They may or may not advertise. They could use the exposure as few investors know them today. Do your own due diligence. Sierra Metals Inc.

### Bob Moriarty 321gold Ltd |