|

||||||||||

Ho, Hum, another Major BottomBob Moriarty You don’t need to know anything about mining to invest profitably in mining shares. You don’t need to understand drill intercepts, you don’t have to spend any time thinking about management or country risk or any of those things all the “Gurus” tell you that you need to know. Actually you could read a single book about people and their behavior and you would be armed with everything you need to know for a lifetime of successful investing. Everybody who is rich knows about the book, that’s mostly why they are rich. Everyone else is listening to the avalanche of noise coming from their “advisors” who never seem to come up with any valuable advice. People are dumber than bricks. That’s all you need to know. Whatever the mob is doing, you need to do the opposite. If you don’t believe me, read the most important book you will ever read, “Extraordinary Popular Delusions” written by Charles Mackay around 1860.

(Click on images to enlarge) I used a picture of the Sprott Physical Silver Trust to predict a major bottom in gold and silver shares back in May and a retest in late July. The chart at the bottom of the page shows how silver investors “vote” on the popularity of the Sprott ETF. When the percentage premium is high, they are very optimistic about the price of silver. When the premium is low, they hate silver and metals shares. Silver is higher now than in May. Silver is higher now than in July yet the premium people are willing to pay for the Sprott Physical Silver Trust is lower. The premium was about 3% in May with $26.20 silver yet with $32.50 silver in November investors will only pay a 2.06% premium. That’s dumb. So do the opposite, we are at a major bottom. That’s the lowest premium for the Sprott Physical Silver Trust since it began.

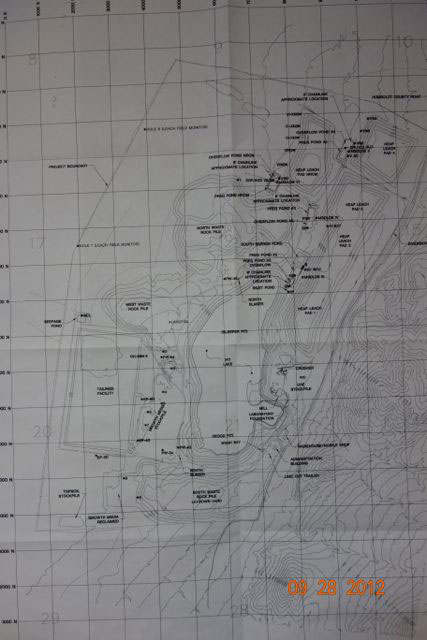

Another favorite chart of mine is the XAU over Gold. It shows the ratio of the XAU (gold shares) compared to the price of gold. Basically it shows which is more popular, gold or shares. At market tops, investors vote for shares (XAU) and at market bottoms they vote for gold. If you look at the chart for November 15, while gold and silver were up, the shares fell out of bed. That’s what you want to see at bottoms. I’m not going to promise anyone that November 15 was the bottom to the minute. No one can do that and the premium on the Sprott ETF can go lower and the pessimism on gold and silver shares can go lower. But the Sprott premium is the lowest it’s ever been and the ratio of the XAU over gold is not only lower than it was in 2008 with $690 gold, it’s lower than it was in 2001 with $252 gold. That’s simply insane. I went to visit a project about six weeks ago in Nevada and I’ve been waiting for the right time to write about it. Given that we are at or approaching a major bottom for gold/silver and the resource shares, I think the time is right to introduce the Sleeper Mine belonging to Paramount Gold & Silver. The numbers from Paramount are pretty darned compelling. In the M&I category they report 4.1 million ounces of gold and 94 million ounces of silver. In the inferred category they show an additional 2.8 million ounces of gold and 61 million ounces of silver. With 6.9 million ounces of gold and 155 million ounces of silver you would think the market would value them higher than their current $319 million market cap. Paramount has two primary projects, the San Miguel deposit in Mexico and the Sleeper Mine in Nevada. Between the two projects, PZG shows some 8.4 million ounces of gold equivalent. That’s about $38 an ounce. That’s pretty cheap especially considering country risk. Paramount completed a PEA on the Sleeper Gold Mine in September showing a Net Present Value of $695 million and an IRR of 26.8%. The PEA used a three year trailing number for gold at $1384 and $26 for silver. The PEA says they can expect production of about 172,000 ounces of gold yearly and 263,000 ounces of silver requiring a Capital Cost of $688 million. PZG has begun their feasibility study. The San Miguel project in Mexico surrounds the Palmarejo Mine and is surrounded by a cluster of eight operating mines in the Sierra Madre Gold/Silver belt. The company released an updated 43-101 resource on the project in October and has begun a PEA that is expected to be released in late 2012. San Miguel shows 1.47 million ounces of gold and about $100 million ounces of silver. The company is well cashed up with about $25 million in the bank and just completed a sale of a non-core asset for $7.6 million to Valor Gold on November 5, 2012. Deals done in the last couple of years in the gold space varied from the $390 an ounce Newmont paid for Fronteer in Nevada to $121 paid for Victoria by Premier. With a price of $38 a resource ounce, Paramount has a lot of upside potential. Paramount has one of the most respected management teams in the business led by CEO Chris Crupi. While I don’t own shares and they are not an advertiser, we are always biased, as anyone else would be. I like the projects, I like the people and I like where they are located. With gold and silver going up or staying steady, I see a higher price for the company than today. Paramount Gold & Silver

### Bob Moriarty 321gold Ltd |