|

|||||||||||||

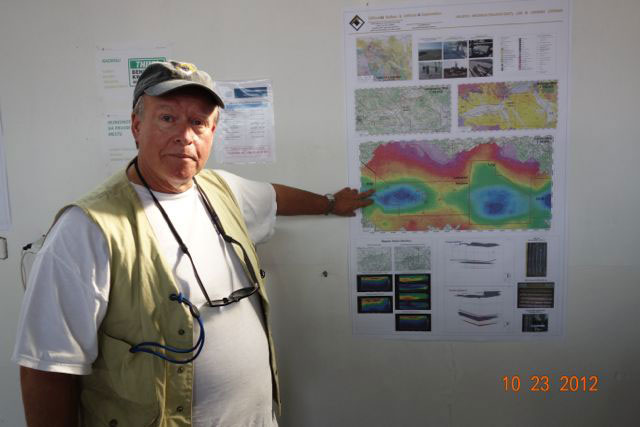

Lithium is SexyBob Moriarty Lithium is sexy. There was a lithium boom a few years back and overnight hundreds of companies claimed they were in the lithium business. Lithium is sexy. That’s a great reason to avoid lithium. That’s a great reason to avoid anything sexy. Uranium had its boom before crashing, nickel had its boom before crashing, lead and zinc boomed before crashing, the REE had their boom before crashing, graphite had its boom. If you are to invest successfully, you must invest in what the crowd doesn’t want. It’s simply not possible for 500 mining companies to succeed mining anything. Go where the crowd isn’t. Boron isn’t sexy. Boron is pretty boring. Two companies control over 75% of the market. They are making money on boron hand over fist. That would be Rio Tinto with operations in California and Argentina and a state controlled company in Turkey. And as sexy as lithium may have been for a short time, the entire world market was only $508 million in 2011 while borates sold $2 billion in the same year. The last month has been a whirlwind. I spent six days flying back and forth to Perth Australia and got to spend one whole day with wifie before heading out on another trip to Serbia, Bosnia and Albania. So far the trip has been well worth it. I got an interesting few days in Serbia and Bosnia with the most technically qualified team I have ever visited, the Dream Team at Pan Global Resources. Rio Tinto created the borates Dream Team. In 2004 the Dream Team, led by geologist Bob Kellie, discovered the Jadar deposit in Serbia. Jadar has an inferred resource of 125 million tonnes at 1.8% lithium (Li2O), and 12.9% boron (B2O3). Using fairly conservative numbers for recovery, that’s $80 billion dollars insitu value. Prior to the iron and coal boom created by China making the transition from an agrarian society to a consumer society, borates were one of the most profitable sectors for Rio Tinto. But in 2008, markets around the world crashed and Rio went from making a billion dollars a month to losing a billion dollars a month. Since borates were now a fraction of the revenue of Rio, the company decided to bail on borates. Sort of. Someone with a more of a fix on sense rather than cents pointed out that if Rio sold the Jadar deposit, they would be creating their own competition. So Rio put the Jadar deposit on a back burner and walked away from a number of already identified but untested basins in the Balkans. A Canadian entrepreneur named Petr Palkovsky was neighbor to the Rio Tinto executive tasked with selling the Jadar deposit. Petr learned of the planned sale and attempted to put together a company to buy Jadar. Rio canceled the planned sale before Mr Palkovsky could put together his group. Palkovsky went to plan B. If Rio didn’t want to sell the $80 billion insitu value Jadar, perhaps he could reassemble the Rio borates team and cookie cutter the Jadar deposit. To give you an idea of how valuable borates were and are to Rio Tinto, they had people working for them who had to sign a document saying they would never work for anyone ever in the borates field. You may safely assume Rio had to pay through the nose to get people to sign away their future. So when the Global Financial Crisis (GFC) struck in 2008, Rio fired them, tore up the contracts forbidding them to work in borates for anyone else and walked away from a dozen potential deposits in Serbia and Bosnia. Petr Palkovsky smiled, convinced Bob Kellie team leader for Rio Tinto discovering Jadar to become partners with him in Lithium Li and promptly picked up every prospective basin in Serbia and Bosnia. The Dream Team, formerly of Rio Tinto, consisted of William Pennell former head of Rio’s Global Industrial Metals exploration group, now a director of Pan Global Resources and others. While at Rio, Pennell worked with world expert, Bob Kistler who literally “wrote the book” on borates and John Reynolds, who is one of the top experts in the world on basins and evaporate deposits. All these guys either work for Lithium Li or consult for them. When Rio Tinto went into Serbia they didn’t know the area the way Lithium Li now does. Discovery of the Jadar deposit was early and exceptional. Rio didn’t test every basin, they just drilled and came up with Jadar at 125 mt of 12.9% B2O3 and 1.8% Li2O. In ground value it's about $80 billion, obviously that isn’t a figure reflecting what can be mined economically. Basically, it’s about $400 a ton rock and is an easy to understand target for Pan Global. All the knowledge Rio assembled came unglued in 2008 in the GFC and was carefully put back together by Lithium Li and Petr Palkovsky. In 2010 Lithium Li entered into a JV with Pan Global Resources headed by a former exploration director of Rio Tinto. The jv calls for Pan Global to spend up to $20 million over 10 years to earn 80% in any 3 of the 15 applications owned by Lithium Li. So far Pan Global has spent over $4 million drilling seven of the applications. Economic mineralization was found in three of the projects, four more were dropped as uneconomical. As company president Julian Bavin said to me, if this was a Chinese company, they would be making production plans now. Hole VBN-003 assayed 18.8 meters of .26 Li2O and 1.3 meters of 16% B203. But Pan Global is looking to duplicate 3 meters mining width of 12.9% B2O3 and 1.8% Li2O or better. Rio’s results had about the same value for borates and lithium. Pan Global would be happy with 25% borates if they came without lithium. Here is how Pan Global compares to Rio’s results.

One very vital bit of information learned since Rio Tinto first came to Serbia is that the basins are best located using gravity sensing. Several of the basins are invisible from the surface and can only be located by gravity testing. Boron forms chemical combinations with literally hundreds of combinations. The primary mineral at Jadar is Jadarite and was named for the Jadar deposit. To date that combination of boron and lithium has only been found at Jadar. Both boron and lithium are found in sediment basins that used to be salt lakes. Pan Global and Lithium Li geos are uncertain if the boron and lithium came from hydrothermal activity or volcanic tuffs but in any case, once the lithium and boron gets into a basin, it stays there. Both metals are highly mobile and while finding basins is easy through gravity, finding just where the borates and lithium are can be more difficult. Buying junior mining stocks is always a gamble. You are purchasing lottery tickets and it’s vital for an investor to understand just what the real odds of a payoff are. Buying Pan Global is like picking up the dice at a crap table where you bet $100 and the payoff is $1000. When you run into those kind of odds, put your money down and roll the dice. You may lose money if things don’t go your way but if you win, you win big. With all commodities, takeovers take place at between 1% and 10% of in situ value. Rio invested about $50 million to find Jadar and now sits on $80 billion worth of in ground value. When in 2008 they were considering “giving” it away, they still valued it at $150 million. The Lithium Li/Pan Global JV is well ahead of where Rio Tinto was given how much money they have spent so far. They literally have the “Dream Team” of borates experts in the world. They are drilling in a known area of economic mineralization where they know the country and area better than anyone in the world. The odds of their success is probably well above 80%. At Friday’s price, the company had an $11 million market cap. I believe they have an 80% chance of hitting a deposit similar in tonnage and value to what Rio did at Jadar. You don’t get much better odds than that. Management is brilliant. These companies are run the way mining companies should be run. They operate lean and mean and aren’t handing out options every time they smash down the shares as most juniors do. The share structure is tight and they are showing a lot of success. Borates may not be sexy but they are profitable and isn’t that what it’s all supposed to be about. Pan Global is an advertiser and we are biased. Do your own due diligence. Pan Global Resources

### Bob Moriarty 321gold Ltd |