| |||

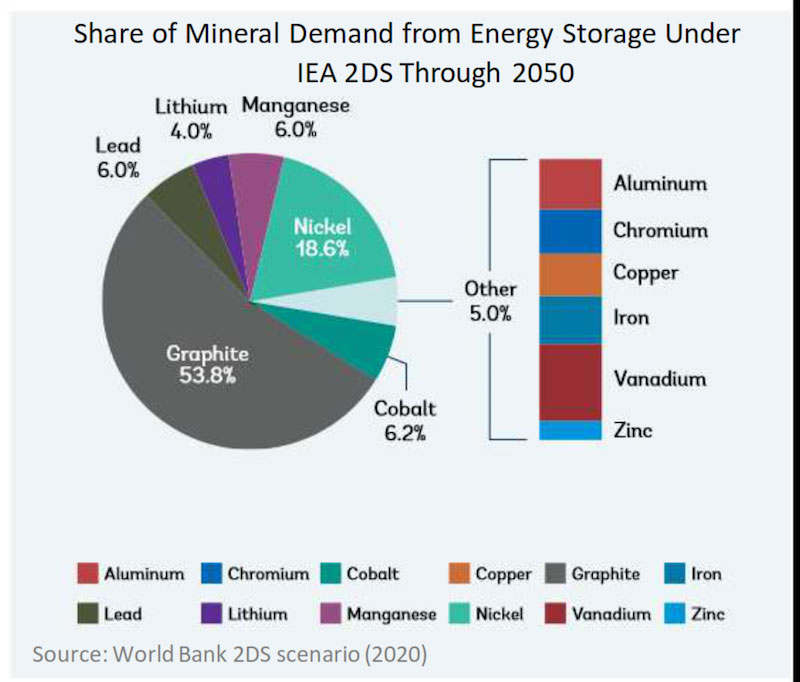

South Star Battery Metals Offers Twenty Fold ReturnBob Moriarty When I talk with management of any company wanting to brief me, I try to stay away from the elevator pitch. Every company president or CEO has given it 3,587 times and has it memorized. All they tell you is what they want you to know. Naturally they tend to ignore all the things you really need to know. So in any meeting when I appear to be chatting in reality I am waiting patiently until I can slip in a bit of a trick question that answers a lot more than the elevator pitch. The first time I tried it I was visiting some copper projects in Chile in the Atacama Desert and talking to the President of the company. Casually I asked him what he wanted to be doing in five years. He was Canadian, about sixty. He came down from Vancouver for the company to develop some projects. He got a stripper pregnant, divorced his wife and ended up with a bouncing baby and a new far more jealous wife who literally followed him everywhere. We were eating lunch at a small café and I saw this woman peering at us all during lunch. I asked the fellow if he had any idea of what she was doing. He told me to ignore it, she was his wife and followed him everywhere to make sure he wasn’t doing to her what he did with his test wife. The trick question was to ask him what he wanted to be doing in five years. What I was hoping for was for him to say that he wanted to be running the biggest and most profitable copper junior in Canada. He answered that he wanted to be retired. Sigh! About ten days ago a good mate of mine wanted me to talk to the President and CEO of a new graphite company planning on going into production of graphite in Brazil shortly. I know a little about graphite, I flew over a great potential graphite project in Ontario. I also visited a tiny but totally AFU graphite deal in Madagascar. And I had a gold project in Sonora Mexico where we drove by a hobby graphite mine operated entirely by hand every time we went to my project. Graphite is interesting. So I thought. I had no idea of just how interesting. In any case, I was Zooming (Is that a verb now like Skyping is?) with Richard Pearce the head of South Star Battery Metals (STS-V). He went through a lot of the reasons graphite is turning into the next big thing when I asked him what he saw the potential was for his company. So he answers without hesitation, “A billion dollars, it’s a big market.” I found myself nonplussed. In all the writing I have ever done and a dozen or so books, I have never found the right time to use that word. In this case it was perfect. When we were speaking the market cap for South Star was about $15 million CAD. Others realized it was a good deal and the stock is fifty percent higher in ten days up to about $22 million CAD. So if he thinks it has a billion dollar potential how is $1 billion divided by $22 million equal to a twenty-fold return? The company is fully permitted to begin immediate construction of a Phase 1 Pilot Plant with an intended production of 5,000 TPA in Brazil, second highest producer of graphite in the world after China. Since the price of graphite varies from about $500 a tonne to as high as $4400 a tonne for large flake Lithium battery grade material. I’ll use a general figure of $1300 a tonne just to give investors some idea of revenue. The $8 million USD pilot plant will begin construction shortly and be in operation in a year. Phase 2 calls for a 25,000 TPA plant at a capital cost of about $27 million USD. That construction decision will be based on how many off-take agreements they can have signed and the cost of capital. Graphite is used for a lot of different applications with a wide variation of technical specifications and prices so a pilot plant really is necessary just to give as many potential buyers samples of what they can expect to get. South Star already has two off-take agreements and I expect more to be signed as construction progresses. As I was talking with Richard Pearce I was struck with his command of the graphite market and his immediate answers to every technical question I asked. Frankly I get a lot of people in management trying to bullshit me so I recognize the difference between BS and someone with a substantial understanding of his market supply and demand. Pearce knows graphite. No one I know has ever done a great job of educating readers about graphite. It’s a market with an enormous variation of pricing and technical specifications for each different application. We probably spent forty-five minutes on the phone and went back and forth from one page to another of the presentation. I found the website frankly to be the best organized of any company I have followed in twenty years. The presentation was the most complete of any I have ever seen. I think that any novice graphite investor will have a good understanding of the market and of South Star when they finish the presentation and then print out and read Appendix 2:Battery Market. Let’s talk lithium batteries and why graphite is so big a deal. (Click on image to enlarge) That chart located on page five of the presentation knocked me for a loop. Graphite is the most important material in a lithium oxide battery. Not just important but the most important making up over 50% of the materials needed for battery storage. I would have said that lithium or cobalt or nickel would be important but they are minor in comparison. That was a real eye opener. But the increasing demand for graphite was enough to blow my socks off. Canaccord did a paper on South Star about three weeks ago that lit a fire under the share price. In the report they estimated that demand for graphite in lithium batteries would increase by 500% between 2020 and 2030. Frankly graphite is going to go into seriously high prices just to meet the increasing demand. While South Star shows a PFS with proven and probable reserves of twelve years production, they are going to have to get real serious about exploring the 95% of the project that remains unexplored. According to the Brazilian Mining Authority, the entire land package belonging 100% to South Star is mineralized and can be mined as an open pit. Earlier I said that Richard Pearce believed he had the reins on a company with a $1 billion market potential and was only worth $22 million today and offers a twenty-fold return. If you can do simple math in your head those figures don’t seem to jibe. The company just finished a private placement for $2.4 million last week. Units were $.11 with a full warrant at $.15 good for three years. That was on top of another private placement back in February for $.105 with a full $.15 warrant. That gives a total of just over 52 million warrants at $.15. When exercised those warrants will bring in over $7.8 million CAD. The latest warrants from a week ago can be accelerated, however, the February warrants cannot be. In any case, when the market fully understands what South Star has and is worth, the price is going to be a large multiple of today’s price. With the $2 million on hand and $7.8 million more coming in from warrants the company is well on the way to having the Phase 1 plant paid for as well as funds for exploration. Naturally they will have to do some additional money raising down the road to finance the $27 million in USD for phase two. So the warrants will increase the outstanding shares to about 150,000 million. I have allocated another 100 million shares for exploration and the Phase 2 project. I don’t have any problem seeing full production with shares at $4 and them touching a $1 billion market cap in 2-3 years. How reasonable would that be as a market cap? Well, let’s look at it from the perspective of how you value real estate. There are three different ways to value a house. Some combination of the three will give you an accurate valuation. The first would be how much it would cost to construct exactly the same house from scratch. That is meaningless with South Star because they picked up their 100% interest in the Santa Cruz Graphite project when no one was interested in an unknown project in a newly discovered district in Brazil. Except for Richard Pearce. The second would be to see what an identical house across the street sells for. Now we are getting into the meat and potatoes of a real value for South Star. There are a number of similar positioned graphite companies that have caught a bid lately. Nouveau Monde Graphite (NOU-V) just put a Phase 1 demonstration plant into production in Quebec in Canada. They plan on producing 2,000 tonnes of battery grade graphite a year in comparison to South Star’s 5,000 tonnes of large flake high value graphite in a year. NOU is valued today at $553 million even with some native issues coming up that don’t exist in Brazil. South Star would have to go up twenty-five times to match NOU. NextSource Materials (NEXT-V) is valued today at $331 million with a 17,000 TPA plant going into Phase 1 production in Q2 of 2022 in Madagascar. Graphite from NEXT is not quite as high a flake size as South Star. Madagascar is the third largest producer of graphite in the world so they are quite experienced with the material. If you valued South Star in comparison it would have to go up fifteen fold to equal the market cap of NEXT. The third and perhaps most significant way to value any real estate project is going to be the cash flow and ROI. That is just as true for any graphite company. And these numbers are going to knock you over. The special high purity spherical graphite for the anodes in electric vehicles is selling today for between $2,200 and $4,500 a tonne. Electric vehicles need an average of between 85 and 115 kilos of graphite each. Call it 100 kilos at say, $30 a kilo. So when you pull out your platinum American Express card for your new Tesla you aren’t just buying the car, you are just paying a fair bit just for the anodes for the battery. The big carmakers are in a race to production in EVs having committed $300 billion in planned funding. Much of that funding is going to go to those who mine and process graphite. South Star is in the right country. South Star is in the right commodity. South Star has experienced mine builders running the company. South Star has brilliant communication. For now South Star is absurdly cheap. Graphite demand and prices are going to go up. The companies prepared to ride the wave are going to make a lot of money. I don’t see saying South Star has billion dollar potential as any leap of faith. This is probably the best company I have written about in twenty years. South Star is an advertiser. I participated in the private placement and have been scooping up shares for the last ten days. I am just as biased as I can be. Go to their presentation. Go to their Appendix for Battery Markets. When I was looking through half a dozen other companies to get information as to where they stood, I was dismayed at the poor job their webmasters did. The sites were filled with meaningless dancing baloney giving bald facts with little communication. If you go to the website for South Star and click on the links I have provided, you will learn everything you need to know about graphite and their plans for production. As always, do your own due diligence. After all, it’s your money. South Star Battery Metals Corp ### Bob Moriarty 321gold Ltd |

Copyright ©2001-2026 321gold Ltd. All Rights Reserved