|

||||||||

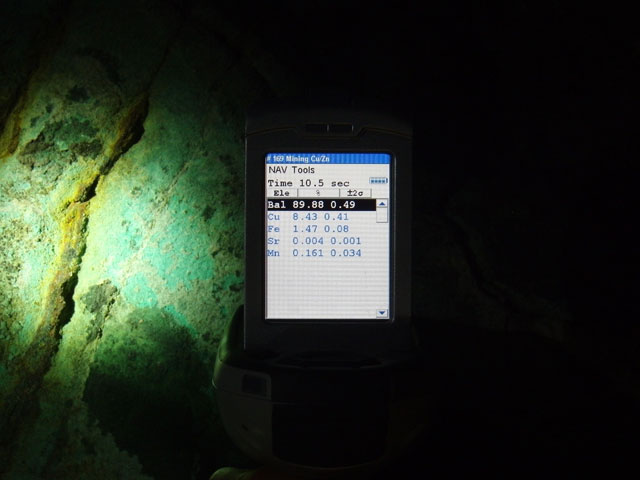

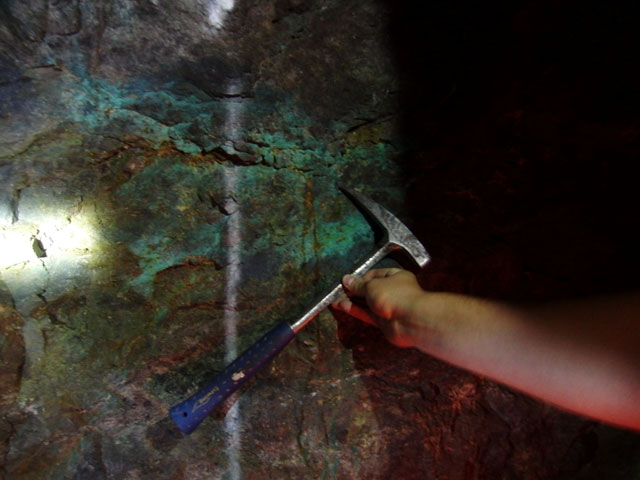

The Creation of WealthBob Moriarty Basic to his overall theme is the idea that wealth is created when a society transitions from an agrarian society to a consumer society. Agrarian societies don’t have much money but they don’t need money to do transactions. Consumer societies on the other hand need currency to complete transactions. China is undergoing the greatest transition in history from an agrarian society to a consumer society. Basically because of the giant sucking sound coming from China, the Chinese determine the price of every commodity. That will continue even when China is not consuming. Prices go up and prices go down. From all appearances China has been building cities and malls just to keep people working. The central government has been quick to try to cool the economy with three interest rate hikes in 2011 alone on top of three in 2010. The economy will slow in China and with it there will be less demand for the basic commodities that make a growing economy larger. Including copper, the only commodity with a Phd. Copper prices have been up and down like a bride’s nightie for the last year, hitting a record high in January at $4.61 and plummeting to a low of about $3.06 in September before recovering to $3.25 now. [corrected] It’s a tough time to be a copper miner. They all are raking in the money at $4.61 copper but many mines start running into problems with a 33% decline in nine months. For marginal producers, a price of $3 might mean shutting down capacity. But for some rare copper producers, there is a giant upside with low commodity prices. Basically, when the price for a commodity is going up, you want leverage. If in 2001 you believed gold was going higher, with the POG at $252, you didn’t want to be looking at someone who could produce gold at $80 an ounce, you wanted to be buying someone who needed $400 an ounce. The $400 an ounce producer doesn’t make any money until prices get above $400 but from there on, his profits rocket higher. Likewise, if you expect the price of copper to go down, you don’t want to own the highest cost producer, you want to own the lowest cost producer. You want to own a mining company in a mining friendly jurisdiction with the highest grade possible. And recently I found one of those. The company is Oracle Mining (OMN-V) and used to be called Golden Hawk. The Oracle Ridge Copper Mine is located some 15 miles northeast of Tucson Arizona. It was a producing mine from 1991 until 1996, mining and milling some 1,000 tons of copper ore per day. With a head grade of 2.33% and recovery of 90%, the mine shipped over 42,500 pounds of copper a day. That would be worth almost $150,000 a day in revenue or just about $50 million a year in income at today’s prices. The management of Oracle has a plan to fast track the mine to production by the end of 2012. The project has an historic but non-43-101 resource of 24 million tonnes at an average grade of 2.33%. They have an ongoing drill program of 5000 meters to upgrade the resource and to bring it into compliance with the requirements of 43-101. The copper ore is contained in a tabular, flat lying body and looking at a plan view, it’s easy to see where the resource is and how a few holes could easily increase the quantity and the quality of the ore body. The high-grade copper ore makes for a high-grade copper concentrate. That is very attractive to commodity trading companies as they can use it to blend in with lower percentage cons. I highly suspect there will be some kind of a financing deal with a commodity trading company in exchange for the right to the cons. The company estimates a Capex of about $80 million to get into production in about 15 months. They have around $14 million in cash on hand now. They will use some sort of debt/equity to raise the money necessary to complete the milling and flotation facility. Oracle plans on building a 2,000 TPD plant and having it in operation by Q1 of 2013. I am very negative on Europe and China but occasionally I come across a company that I think will thrive under what would be adverse conditions for anyone else. If you like mining in the US and you like copper, Oracle is incredibly cheap. I see a lot of good things on the horizon for them. Oracle is an advertiser. The management is very strong and they have a plan that should work. I think they will be producing in 15 months at a nice profit and a much higher share price. As always, readers are reminded they are responsible for their own due diligence. Oracle Mining

### |