Yukon

Gold and the Klondike Big Inch Land Co Yukon

Gold and the Klondike Big Inch Land Co

Bob Moriarty

Archives

September 7, 2006

I've been around

the mining business for a long, long time. My speciality is placer

gold, I began my mining career in 1951 or 1952, panning for gold

at the Knott's Berry Farm in Buena Park, California. It's hard

to remember the year with precision, I was but six. But well

I remember the first flash of buttery gold flakes at the bottom

of my pan.

Knott's Berry

Farm was a real farm, out in the country. And for prospective

miners, both boys and girls, they had a gold panning area where

real professionals would show you the ropes as it were. As we

get older, we forget how important the memories of childhood

are, and how they form what we are. But I remember the first

yellow flash of gold I would ever see. And anytime I get a chance

to teach a child to pan, I take it. I suspect and hope they will

remember it as well as I did.

I continued

in my career in 1955 when I staked my first lode gold claim in

the Yukon, I was 9 by then. Actually, I didn't stake the claim

myself, I had someone else do it and they shipped the paperwork

to me in a box of Quaker Oats cereal. I was then an official

owner of one square inch of gold ground from the Klondike Big

Inch Land Company.

The story actually

started in 1947 with a radio show called "The Challenge

of the Yukon" starring Sergeant Preston and his faithful

companion, a Malamute named Yukon King. Malamutes scare hell

out of Ted because they are so big and he is so small. But that's

another story. In any case, by 1955 the radio show had dropped

in popularity to the point it was dropped and Quaker Oats, the

sponsor of the series paid to have the show brought over to the

new medium of television.

I actually

remember when there was no TV in the average household in the

US. 1955 or so was about the time TV became common and affordable.

Quaker Oats moved the series, now known as "Sergeant Preston

of the Yukon" over to TV in 1955 where it would continue

until 1958. But Quaker Oats needed some gimmick to get kids to

watch the show and better yet to convince their parents to purchase

car loads of overpriced cereal. It was a particular moment of

time where some unknown and unheralded advertising wonk came

up with the perfect pitch, one which turned into one of the most

successful promotions of all time. It got me into the hard rock

gold mining business in a small way.

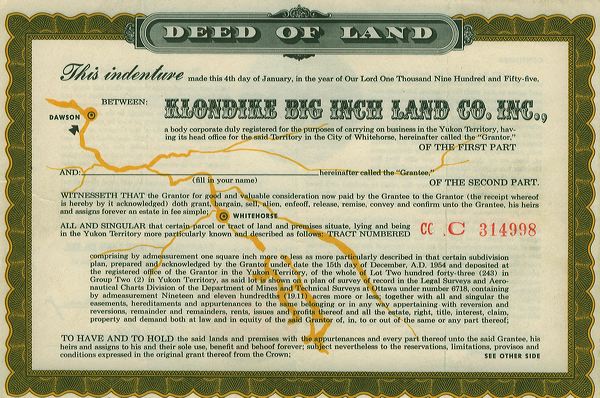

Quaker Oats

set up an Illinois corporation called the Klondike Big Inch Land

Company. The company promptly bought a 19.11 acre parcel of moose

pasture in the Yukon south of Dawson. After carefully measuring

out the land in 1 square inch parcels, Quaker Oats began putting

21 million "Deeds" into carefully marked boxes of cereal.

On each show, Sergeant Preston hawked the "Deeds" to

all the little kiddies. In a few short weeks, the cereal boxes

flew off the shelves and the promotion ended.

I was the proud

owner of one of those "Deeds" to what just had to be

a lode gold claim. I remember well dreaming of just how I would

develop my mine. Alas, the Yukon Lands Branch wasn't so thrilled.

The cost to actually issue a deed for each square inch would

have been prohibitive so claim holders held "Title"

to a square inch but it was a loose title. By 1965 Quaker Oats

tired of being contacted on a regular basis by junior miners

and let the land taxes in the amount of $37.20 lapse. The government

of the Yukon was once again the owner. To this day Quaker Oats,

the Yukon Lands Branch and the Yukon Department of Commerce still

get phone calls from now older but no wiser land "Owners."

I was in the Yukon

about 10 days ago staying in Dawson. I saw a couple of the deeds

framed, front and back and read the story which has been well

researched. I do remember well how rich I felt as a landowner

of a gold property in the Yukon. I was in the Yukon

about 10 days ago staying in Dawson. I saw a couple of the deeds

framed, front and back and read the story which has been well

researched. I do remember well how rich I felt as a landowner

of a gold property in the Yukon.

A few days

later, I saw a real gold mine in the Yukon. It wasn't moose pasture

and wasn't quoted in square inches. But they have boatloads of

gold and are so far under the radar screen of most investors

that I had to keep kicking myself in disbelief. I like buying

and reporting on companies which have a 5 bagger potential but

every once in awhile I come across a 10 bagger which has 20+

bagger potential and I'm going to tell you about one.

YGC Resources

I'm going to

start first by talking about the Ketza River Mine because it

is the heart of the story. I call it a mine whereas YGC Resources

calls it a project and kinda infers there are two different portions.

All of their problem is communication and it was a mine

so it is a mine.

Over the past

20 or so years, different companies have sunk over $50 million

dollars into the Ketza River Mine located about 110 miles NE

of Whitehorse. Between 1987 and 1990, Canamax produced over 100,000

ounces of gold averaging about 10 grams. Canamax put up a $25,000

bond and was given permission to mine an oxide layer of gold

located between both an upper layer of sulfide ore and a lower

layer of sulfide ore. I had never heard of oxide ore being found

between layers of sulfide ores, normally an oxide ore is what

was a sulfide ore body weathered down by water and air. But in

this case, there was an underground river which ran through a

sulfide body and turned it into an oxide. The good news is that

oxide ore causes less problems with the environment and the bad

news is that when you run out of oxide ore, the bond required

to mine sulfide ore tends to be higher because of the increased

costs of mining where acid may be an issue.

In this case,

the Powers That Be demanded a $2 million dollar bond for Canamax

to mine the gold sulfide ore. The company wasn't happy about

having to put up that much money. The company shut down the mine

and mill to show how much power they had (which is almost always

a bad idea when dealing with any government agency.) Before they

could win this test of wills, problems in other areas of the

company caused financial issues and Canamax lost the property.

A fellow named

Graham Dickson had built the 680 TPD plant. After the property

bounced around the industry for a bit, he picked up a 100% interest

in 1994. After sitting patiently for the price of gold to recover,

Graham, now President and CEO of YGC, put the company into high

gear in May of 2005. In all of the literature, the company refers

to two properties, the Ketza River Mine or Ketza Manto Zone and

the Shamrock Zone but to everyone other than a geologist, both

properties will feed the Ketza River Mine. It's a mine, it is

not a couple of exploration targets.

Because of

43-101, management can't say they are going back into production,

only that they are going to make a production decision by March

31, of 2007. But the mine has already produced 100,000 ounces

of gold from 10 gpt ore in the past, they have a 43-101 resource

of over 1.8 million ounces in all categories. A new 43-101 resource

is due out this month and it obviously will be higher. Over on

Stockhouse, someone who at least sounds like he knows what he

is talking about has looked at all the drill core results and

has estimated the new resource will be in the 3.2 million ounce

range. With those kind of numbers, you can guarantee the big

boys will be soon sniffing around.

If I had upwards

of two million ounces of gold and a mill and the gold was either

near or at the surface and it ran 5-10 gpt, it wouldn't take

me until next March to make a decision. It wouldn't take me past

the time it takes you to read this sentence to make a production

decision and regardless of what management puts in writing, I

can assure you they are planning production.

click on images to

enlarge

I met Graham

in Whitehorse in late August. Together with a major German shareholder,

Werner Ulman, we flew out to the Ketza River Mine on a stunning

Yukon autumn day. As we approached the property, I could see

iron stained gossans off in the distance. That's a very good

sign of a giant system.

Since gossans

are such a good indication of iron rich systems, any interested

reader should go to this link to read up on how

valuable the information can be from a gossan. I wasn't aware

of it before reading that piece but the largest open pit mine

in North America, Bingham Canyon, was discovered because of the

iron staining from a gossan. Since gold and silver are often

associated with iron, a gossan is a good sign.

When I visit

a property, I want to get some feel for the size potential. Many

times, in fact, most times, that just isn't possible because

the mineralization may only outcrop at surface. But we were seeing

gossans a long ways away from the Ketza River Mine itself. This

is one giant deposit and they aren't going to run out of gold

any time soon. They pretty much could do drilling just based

on visual indications.

A popular business

model in mining is to maximize the mine. That is, produce all

you can, as fast as you can and leave. I don't find that model

as attractive as that of rationalizing a mine and creating a

cash cow which will produce minerals at a profit for a long long

time. Think of the gold and silver mines in Mexico and South

America which have produced wealth for many generations. Many

of the old family fortunes in the US and Canada came from generational

mines.

Graham Dickson

thinks long term. He is a production guy so he doesn't even think

of a project without planning on how he can go into production.

With the Ketza Mine, he can create the perfect size operation,

to get a reasonable cost of operation but not put the mine out

of production in five years by overproducing. I think that model

makes heap of sense and those are the kinds of operations I want

to see. Once your plant and equipment is paid for, your costs

really drop down. I am baffled as to why mining companies don't

work harder to make mines profitable. Isn't that the whole point?

Here are some

of the goals and time lines.

New 43-101

based on the over $7 million drilling over the last year by September

of 2006.

PRE-feasibility

completed by December 31, 2006.

Production

decision by March 31, 2007.

Mine and Mill

in operation by late 2008.

Begin acquisition

of another late stage property by 2007.

And that's

a big factor in why I like the company so much. Sure, with 1.8

million ounces today, the company could reasonably have a value

up to $180 million based on any comparison with their peers.

More gold will mean higher valuation. The majors and mid-tier

company are going to get real interested at anything north of

3 million ounces. The biggest danger I see is someone coming

in with a low-ball offer before management can get their story

understood by ordinary investors. (Think NovaGold and Barrick)

But Graham

Dickson has designed and put around 20 mills into production.

His team is a production team and that is the expertise in the

shortest supply in the industry. There are a zillion guys around

who can claim to be smart enough to drill holes in the ground.

But there are damned few people who have the experience of actually

putting mines into production and most exploration companies

won't touch production with a ten foot pole.

YGC is well

financed with about $12.5 million in the kitty expected by December

of 2006 based on the current burn rate. The exercise of another

14 million warrants and options would bring in another $12.9

million dollars. I don't see any reason they can't be totally

self financing from here without any more shares being issued.

A minor debt financing would cover any projected shortfall.

I'd guess they

are looking at maybe 150,000 ounce per year production of gold

with a credit of 150,000 ounces of silver as well. Costs will

be below $200 an ounce even though they have to truck in diesel

fuel for their power generation. The rest of the Yukon has a

power surplus for now and there is a good chance the Yukon government

will bring in electricity which will make a major impact on lowering

production costs.

I like YGC

better than any company I've seen since I first wrote up NovaGold

five years ago. Their communication is terrible, going through

the website is like wading through a shoulder high swamp. But

that's why the stock is so cheap. They at least understand they

need a total rework of their website and that they need to improve

communication. But if their website told the real story, the

stock wouldn't be $1.39.

Management

is as solid as a rock across the board from geology to mining

to gluing mills together. The board is a real board, not a bunch

of drinking buddies claiming titles. Management and insiders

control about 24% of the stock and the rest is in strong hands.

When I finally

understood the story, I bought a fair number of shares. I have

an interest in seeing the price go higher and any reader should

understand I am biased. This stock is about as close to a buy

and forget as any stock I've seen since I first told anyone to

buy NovaGold. The biggest danger isn't the stock price going

down, it's getting bought out way too cheap. This is a production

company with production management and a real mine. They will

be leaders, not followers and in the worst case situation, if

someone buys them way too cheap, stick to management, I can assure

you they are going to turn around and do the same thing again.

YGC is an advertiser

and we do own shares.

Written in East End, Grand Cayman on September 6, 2006.

YGC Resources

Ltd.

YGC-T $1.39 Canadian (September 6, 2006)

YGCFF-OTCBB

56.4 million shares outstanding

YGC Resources website

Bob Moriarty

President: 321gold

Archives

321gold Inc

|