Treasures of the Sierra Madre

Palladon, Mag Silver, Sydney, Excellon

Bob Moriarty

Sep 8, 2004

I recently made a trip to Mexico to visit the Santa Cruz property

of Endeavour Silver. I also

made plans to visit a copper property in Utah on behalf of Palladon

Ventures. When I was setting up the trip with CEO George

Young of Palladon, he suggested I extend my trip to Mexico and

see more of the properties in his stable. I did... and other

than a bad case of the Quang Tri Quickstep, the trip was nothing

short of remarkable.

Most gold/silver sites, including ours, tend to expand on the

potential for the precious metals. In a way we do a disservice

to our readers and for that I apologize. My main fixation is

the precarious state of the US and World financial system and

that results in my fixation on silver and gold as solutions to

our monetary problems. But there is a world of commodities out there

which offer just as much, if not more, financial reward than

do gold and silver. If you disagree, just look at a charts of

moly or uranium for the last year or so.

We are in a bull market for real goods. We are in the midst of

a transition from financial instruments of mass destruction,

as Warren Buffett likes to call derivatives, and going into a

massive bull market for real goods of all kinds. And for those

who want to believe a cartel of some kind controls the price

of silver and gold, I hold that Chinese demand for commodities

of all sorts has far more effect on gold and silver than any

mysterious cartel.

This bull market began in 2001 after gold hit a low in 1999.

For the metals stocks a strong correction began last December.

I think we had a bottom in May but we may well test the lows

again. All bull markets go through corrections and this is no

different. It has lasted nine months. It may last another nine

months and it won't make any difference in the end. If you are

swift on your feet, you can trade in and out as Harry Schultz

suggests or simply buy and hold as Richard Russell says.

Across the board you can see many many stocks selling at what

appear to be absurdly low prices. The primary reason they appear

to be selling at absurdly low prices is that they are selling

at absurdly low prices. If you are a contrarian - and that's

the only tried and proven way to make money that I am aware of

- low prices are an opportunity, not a problem. When I write

about a stock or a group of stocks, I am not trying to suggest

these are the best or the only stocks you should consider. We

are in a gold/silver bull market and hundreds of stocks are selling

at giveaway prices. That's a good time to buy, when no one wants

them. When everyone wants them, sell.

Before I expound on Mag Silver - the first of George Young's

companies in North America - I need to give you a little information

on silver in general and Mexico in particular.

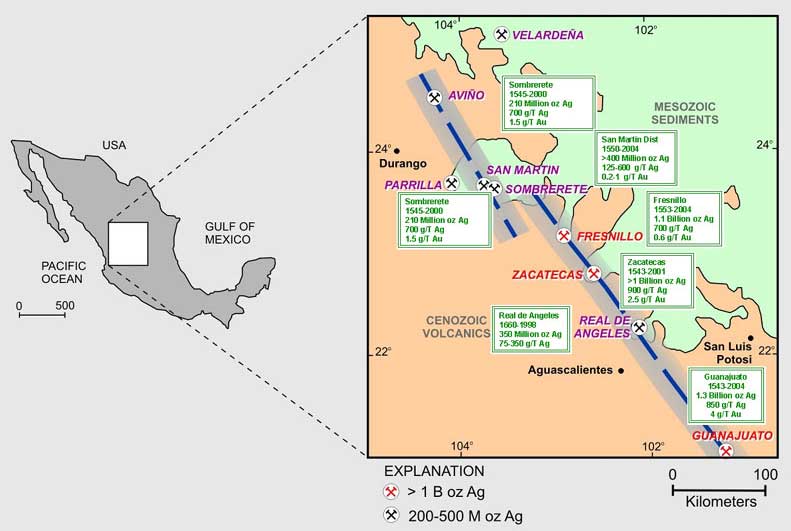

Mexico produces more silver than any country in the world. Mexico's

largest producer is Penoles with production of 48.4 million ounces

last year. And Penoles' largest mine is the Fresnillo mine in

the state of Zacatecas with production of about 31 million ounces

yearly. So the Fresnillo mine produces about 2/3s of all the

silver produced by the largest silver producer in Mexico. Silver

at Fresnillo was discovered in 1566 in a surface outcrop.

From 1566 until 1976, the production

of silver continued at the mine based primarily on drifting on

the surface outcroppings. Eventually these ore veins, averaging

700 grams of silver to the ton as well as high grade zinc and

lead, began to run out. Plans were made after 410 years of production

to close the mine in 1976 after total silver production of 500

million ounces. From 1566 until 1976, the production

of silver continued at the mine based primarily on drifting on

the surface outcroppings. Eventually these ore veins, averaging

700 grams of silver to the ton as well as high grade zinc and

lead, began to run out. Plans were made after 410 years of production

to close the mine in 1976 after total silver production of 500

million ounces.

The veins at Fresnillo are pretty unusual.

While there was minor outcropping, that's how the Indians found

silver in the first place, most of the veins lie deep. As much

as 500 meters below the surface. In the over 400 years of production,

little exploration had been done. So Penoles tried drilling to

see if there were any silver veins in the neighborhood they had

overlooked. And indeed they had. They drilled deep and found

half a dozen more veins. In the first 410 years they produced

500 million ounces and since 1976 have produced another 500 million

ounces. The veins at Fresnillo are pretty unusual.

While there was minor outcropping, that's how the Indians found

silver in the first place, most of the veins lie deep. As much

as 500 meters below the surface. In the over 400 years of production,

little exploration had been done. So Penoles tried drilling to

see if there were any silver veins in the neighborhood they had

overlooked. And indeed they had. They drilled deep and found

half a dozen more veins. In the first 410 years they produced

500 million ounces and since 1976 have produced another 500 million

ounces.

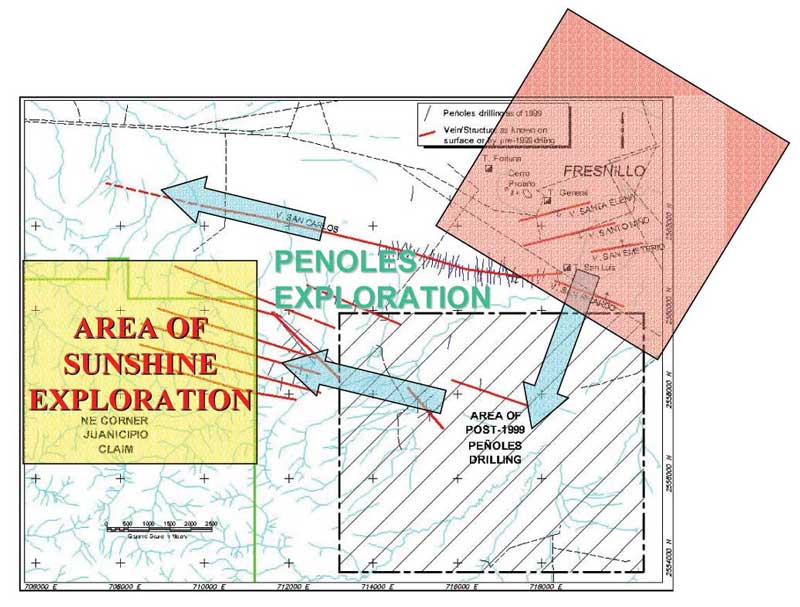

A commonly held truism in the mining business is that the best

place to explore is within the shadow of the headframe of an

old mine. With that in mind, Peter Megaw brought the Juanicipio

property to the Sunshine Mining Company years back.

When the Sunshine went belly up two years ago

as a result of $4 silver, Peter snapped up the property and vended

it into Mag Silver. When the Sunshine went belly up two years ago

as a result of $4 silver, Peter snapped up the property and vended

it into Mag Silver.

In April of 2003 Mag Silver went public at $.50. (Mag Silver

Corporation MAG-V $.91 Canadian 25.5 million shares 29 million

fully diluted Market cap of about $27 million Canadian MSLRF-OTCBB

- website).

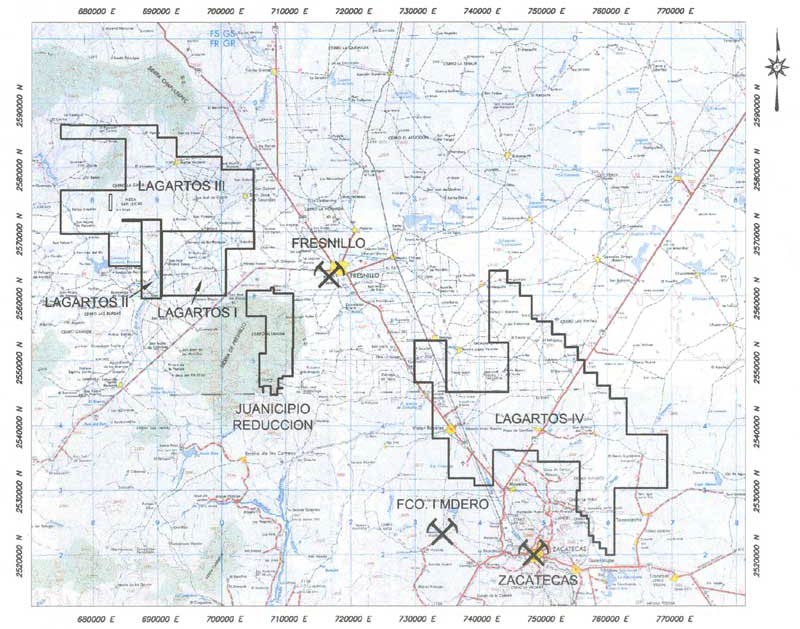

Mag Silver has acquired six major silver properties including

the Juanicipio/Lagartos properties surrounding the Fresnillo

mine.

I saw but two out of the six Mag Silver

properties. Mag Silver is hunting elephants and when hunting

elephants, looking in elephant county is always a good idea. I saw but two out of the six Mag Silver

properties. Mag Silver is hunting elephants and when hunting

elephants, looking in elephant county is always a good idea.

Drilling during 2003 and earlier this year on the Juanicipio

property just 5 km from the Fresnillo Mine proves Peter's thesis.

The property lies right on the NW trending structure. As Peter

explained patiently to me, Mexico has been compacted like an

accordion and then expanded just like an accordion expanding.

I took a picture out of the aircraft when I was

flying from Mexico to Dallas and it shows the nature of the silver

structures perfectly. I took a picture out of the aircraft when I was

flying from Mexico to Dallas and it shows the nature of the silver

structures perfectly.

If all that Mag Silver wanted to accomplish is hunting elephants,

they have already demonstrated that not only are they hunting

elephants, they have nailed an elephant. Penoles is currently

using two drill rigs to drill right up to Mag's Juanicipio property

where Mag has found Fresnillo grade silver/lead/zinc mineralization

with with a high grade gold kicker (10 grams to the ton).

But what I saw that interested me wasn't the Juanicipio property.

It is identical to Fresnillo with a gold kicker and no doubt

Penoles will be tapping on the door of Mag soon wanting to talk

JV. But Peter Megaw isn't just hunting elephants in the very

heart of elephant country, he's using nuclear weapons to hunt

them. While I was at the property, they were in the midst of

moving the drill rig 25 km to the NW of Fresnillo.

Mag Silver did a magnetic IP study on the entire district and

the results showed it's possible the district extends not just

5 km from Fresnillo to the Juanicipio property to possibly 25

km to the NW where the ground is identical to that of Fresnillo.

By now the 800 meter hole has been completed at Lagartos which

targeted two distinct IP anomalies. If the assay results show

Fresnillo grade structures, Peter Megaw and Mag Silver may well

have bagged their elephant. Expect results to be released in

4-6 weeks.

If it was all that simple to discover millions of ounces of silver

or gold, it's pretty logical to wonder just why it hasn't been

done before in the same area. And the answer is fairly simple.

All in costs to drill in the area run about $200 US per meter.

So an 800 meter hole which will only test two structures about

500 meters below the surface costs about $160,000. Those sort

of holes blow big holes in budgets rather quickly.

All investing in penny juniors is crap shooting and don't let

anyone kid you elsewise.

[Barb swears I just made up this word]. What you are looking for is good management who

have come up with some good projects with 10-bagger or higher

potential. Earlier this year Mag was selling in the $2.50 range.

Three weeks ago it was selling barely above the IPO price. That

doesn't make a lot of sense. They have made a lot of progress,

are on the verge of potential stardom and have six good properties

in their stable. At $2.50 I wouldn't be waving my arms and legs

but at below $1 making money on Mag is about as difficult as

falling off a bike.

Peter Megaw is one

of the genuinely nice people in the industry. While he is a PhD,

he does speak English and does a great job of communicating complex

geological theory to boneheads such as me. And he speaks fluent

Spanish and Swedish and can get by in French. Figure that one

out. And the four days we spent together driving across Mexico

were a delight (with the exception of this click

| click

| click

| click).

Our next stop after the Fresnillo district was to see the gold

property of Sydney Resources at Inde in the state of Durango.

(Sydney Resource Corporation

SYR-V $.41 Canadian 16.5 million shares outstanding 22.5 million

total including options and warrants at higher prices $6.7 million

market cap SYROF-OTCBB - website).

Sydney has entirely different management from

Mag Silver, the common denominator is Peter Megaw as geological

consultant. Sydney optioned the Inde property earlier this year

and stands to earn up to a 70% interest over time. Full details

can be found on their website. Sydney has entirely different management from

Mag Silver, the common denominator is Peter Megaw as geological

consultant. Sydney optioned the Inde property earlier this year

and stands to earn up to a 70% interest over time. Full details

can be found on their website.

Inde shows production of gold going back as far at 1532 and has

produced between 1-2 million ounces of gold. Miners sought high

grade structures consisting of oxide ore in both vein and carbonate

hosted mineralization. While sulfides are known, no mining has

been done below the water table.

Sydney has been working on a surface mapping and trenching program

to define potential drill targets. Trenching results already

received indicates the potential for a low grade surface bulk

operation previously not envisioned.

Inde wasn't the sort of project that grabs you by the throat

and screams "Buy me, Buy me" at you but if you subtract

the cash on hand from the market cap, you come up with a net

market cap of about $4.7 million. Having an office and a two

line phone in Vancouver makes any company worth $5-$6 million

so it's not much of a stretch to see the company is pretty cheap.

Good results on the search for low grade, bulk tonnage would

hit the stock like a shot of Cuban coffee so it's worth keeping

Sydney on the radar screen. Unlike the other projects I saw on

the trip, I didn't demand Peter stop the truck so I could call

my broker and buy some shares but at any lower price, I personally

would be a buyer.

The next project we visited was enough to stop the truck

and make a phone call to my broker. From the minute Peter started

talking about it, it sat up like a tiny puppy in a pet shop window

on its back legs and barked, "Buy me, Buy me." So I

did.

The Platosa Project is a very high grade silver property(11900

grams to the ton over 5.6 meters for one intercept) in the State

of Durango. Excellon Resources - (EXN-V $.18 Canadian,

110 million

shares outstanding, 147 million shares fully diluted, market

cap $19.8 million Canadian (corrected) - website)

- is in the process of driving a ramp with the intent of going

into a large scale bulk test mining with December as a production

date.

According to Excellon, "Platosa

strongly resembles several of the world-class Carbonate Replacement

Deposits (CRDs) of Mexico such as the Santa Eulalia, Naica and

Ojuela deposits, all of which have produced millions of tons

of high-grade mineralization. Like Platosa, these deposits had

minor surface expressions that were followed to the bulk of the

deposits." According to Excellon, "Platosa

strongly resembles several of the world-class Carbonate Replacement

Deposits (CRDs) of Mexico such as the Santa Eulalia, Naica and

Ojuela deposits, all of which have produced millions of tons

of high-grade mineralization. Like Platosa, these deposits had

minor surface expressions that were followed to the bulk of the

deposits."

It's a complicated project. Part of it is a JV with Apex silver

with Excellon holding a 51% interest and Apex holding the remaining

49% and part of it (the most interesting part) being 100% owned

by Excellon.

Excellon is going into production. Over the next 14 months they

expect to produce about $15 million US in free cash flow after

expenses. It will cost them $10 million US to open a ramp and

do the mining. But they have the cash in hand. The website has

barely been updated in two years and it's largely responsible

for the dismal state of the stock. I have talked to Peter Megaw

at some length about it. And I have seen a Power Point Presentation

which is brilliant, but it isn't available through their website.

Basically, Excellon and Apex have gone to an area of old production

in NE Durango State. Peter and his people have found a Carbonate

Replacement system which seems pretty large. Certainly it is

high grade. On what they refer to as the Core property, a property

not part of the Apex JV, they have drilled an indicated 65,000

tons of high grade silver/lead/zinc. It averages 75 ounces of

silver to the ton, 12% zinc and 15% lead.

Generally it is considered heresy in the mining industry for

junior mining companies to be considered exploration companies

yet to go into production. It's perfectly OK for 99 out of 100

to waste every dime of their shareholders' money drilling holes

until states like Nevada look like Swiss cheese but the very

suggestion of going into production brings out the garlic and

silver crosses.

Basically Excellon is going to produce between $20 and $30 million

dollars in the next 14 months. Depending on the prices received,

they should net between $10 and $20 million dollars. I consider

that a smart move. $15 million in cash buys a lot of professional

exploration.

Their $10 million dollar website fails to mention anything about

going into production on what is a tiny scale. I call it a $10

million dollar website because they have a brilliant story and

the website utterly fails to tell the story. So the website,

the $10 million dollar website, is costing shareholders $10 million

in market cap. If they earn $10 million, which is on the low

side for the metals, ($.25 Lead, $.35 zinc and $4.80 silver)

in the next year or so, the stock ought to be much higher than

a $9 million dollar market cap.

Peter Megaw believes the known 65,000 ton resource is merely

the end cap of a far bigger system. Post mineralization faulting

has broken the deposit into 6 distinct zones but by working backwards

in exploration, Peter believes he can chase down a lower grade

but far bigger bulk target.

Since Excellon plans on using contract labor as much as possible

and direct shipping the ore to a refinery nearby, their costs

will be relatively high on a per ton basis but with $650 per

ton ore, a few bucks higher cost is relatively meaningless. Excellon

is adding only three people to their staff to run the operation

and that doesn't take a brain surgeon or rocket scientist to

manage.

I like the concept and the stock. We were buyers at $.20 a share.

Making money on Excellon is going to be about as difficult as

falling off a bike. Be careful should you decide to buy. The

liquidity just isn't there. It would be there if they ever got

around to telling their story but right now it's not. If you

put in a market order to buy shares, you will get scalped. Naturally

you are responsible for your own due diligence.

A week in Mexico was all that my system could handle, I flew

out of Torreon after my visit to Platosa to my next stop in Salt

Lake City to meet with George Young, CEO of Palladon.

Palladon Ventures - (PLL-V $.41 Canadian 20.6 million

shares, $8 Million dollar market cap, $4 million in cash on hand,

PLLVF-OTCBB - website)

- has put together a commanding land position by consolidating

a number of claims in the Milford area 200 miles SW of Salt Lake

City. The area is probably the last and best chance for a major

copper property in the United States.

George picked me up at the airport

and we went over to Bingham Canyon to see what he would like

to find for Palladon. Bingham Canyon is the first and largest

open pit copper mine in the world. Since opening in 1906 they

have mined over 6 billion tons of rock. Bingham Canyon has produced

enough copper to wire every house and factory in Mexico, the

United States and Canada. But they are soon to run out of ore. George picked me up at the airport

and we went over to Bingham Canyon to see what he would like

to find for Palladon. Bingham Canyon is the first and largest

open pit copper mine in the world. Since opening in 1906 they

have mined over 6 billion tons of rock. Bingham Canyon has produced

enough copper to wire every house and factory in Mexico, the

United States and Canada. But they are soon to run out of ore.

Palladon Ventures is a work in progress. Right

now George and his crack management team are trying to define

their business model. There were a dozen or more mines operating

in the Milford district in the past and there is already milled

ore waiting to be processed. They have an option to earn into

65% of the 70,000 acre district. They are considering going into

production ala Excellon albeit on a far smaller scale. Palladon Ventures is a work in progress. Right

now George and his crack management team are trying to define

their business model. There were a dozen or more mines operating

in the Milford district in the past and there is already milled

ore waiting to be processed. They have an option to earn into

65% of the 70,000 acre district. They are considering going into

production ala Excellon albeit on a far smaller scale.

What they have accomplished is to consolidate the district. All

by itself, that is a major victory. The project will look far

more attractive to a tentative JV partner the larger it is.

I've owned the stock for months, bought at a

higher price on the recommendation of a good friend. With a net

market cap of $4 million, it wouldn't take much in the way of

news to bump up the stock. Probably the ideal situation would

be to get into a JV with one of the copper majors but management

is looking quite seriously into bootstrapping themselves into

cash flow by processing the already-stockpiled ore. I've owned the stock for months, bought at a

higher price on the recommendation of a good friend. With a net

market cap of $4 million, it wouldn't take much in the way of

news to bump up the stock. Probably the ideal situation would

be to get into a JV with one of the copper majors but management

is looking quite seriously into bootstrapping themselves into

cash flow by processing the already-stockpiled ore.

In addition to the Western Utah Copper Project, Palladon has

a slew of mostly gold properties in Patagonia, Argentina. With

management as experienced as George Young, I look forward to

more and better news.

Our opinions are our own, we are not paid in any way to write

about companies. Most of them are companies we have invested

in so read anything we write with an eye to our potential bias.

And please take some responsibility for doing your own due diligence.

By the time you read this (Tuesday

7th) I will be winging my way to Las Vegas to the gold show,

I'll be back on Friday, so please don't send me email until Friday.

September 7, 2004

Bob Moriarty

President:

321gold Inc

Archives

321gold Inc

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}