|

||||||||||

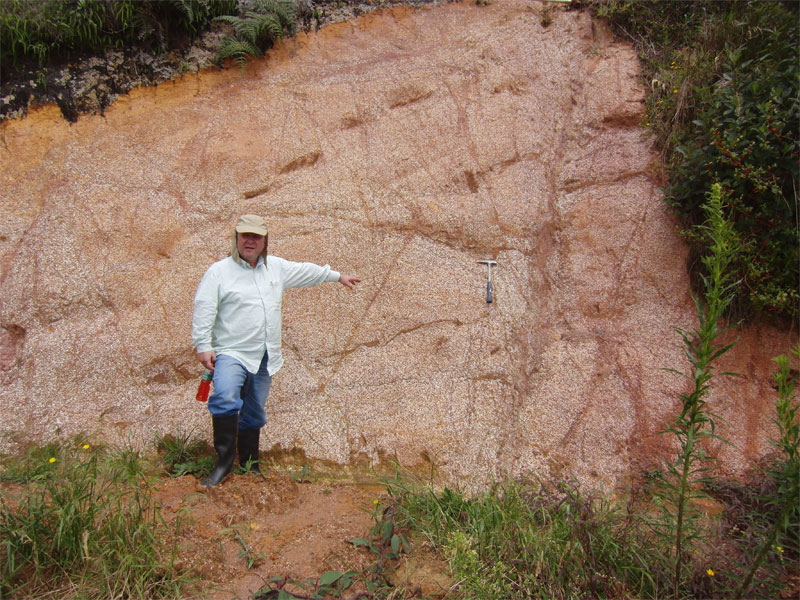

400 Years of Mining GoldBob Moriarty Picking junior mining stocks is getting more and more difficult. There are a bunch of ETFs an investor can buy and that is taking a lot of money off the table. Also there is a proliferation of juniors out there. I have heard estimates of between 1500 and 3000. One thing I would highly recommend to any tentative investor would be to look at a five-year chart. If you are looking at a company that hasn’t moved in the last five years, it probably isn’t going to move in the next five years. We have had ten years of record prices for everything. If management couldn’t come up with something in the last five years, they aren’t ever going to come up with anything. Opportunities still abound. I came back from Colombia recently and I saw a handful of new companies who saw the opportunity in Colombia and are charging ahead. One company, Red Eagle Mining (RD-V), contacted me while I was in Medellin to inquire about me going to see one of their projects. I had the time so I was pleased to say that I could do it. It was a short but very interesting visit. Chairman of the Board and CEO Ian Slater, formerly CEO with the Lundin Group, has put together a world-class team for Colombia. The company VP for Exploration, Alejandro Kakarieka, was good enough to take his time to show me around the Santa Rosa project located some 70 km north of Medellin on paved roads. They have a 2nd project called Pavo Real that is well to the south of Medellin. According to Alejandro, the projects are of equal value. I didn’t have time to visit the Pavo Real project but what I saw of Santa Rosa convinced me that Red Eagle has a tiger by the tail. Red Eagle is trying to define a large-scale bulk tonnage target at Santa Rosa. From what I saw, it is certainly possible. The area has been mined for high-grade narrow veins for 400 years. And that mining has barely scratched the surface. The Red Eagle team has located and mapped some 60 areas where the Spanish used hydraulic sluicing to wash down hills and over 280 adits and shafts. We visited one small scale mine near their land where the miners were mining a half-meter of 5 ounce per ton gold.

The management team is first class and includes Robert Bell, a highly experienced mine builder, Robert Pease, former CEO and founder of Terrane Metals, Tim Petterson VP for Corporate Development is a mining engineer and was head of mining research for both ABN AMRO and HSBC. Alejandro Kakarieka was Exploration Manager and Country Manager for Imgold in Colombia. Ken Cunningham, CEO of Miranda Gold, is a director as well as Jeffrey Mason, former CFO of Hunter Dickinson. The company only went public on June 28, 2011. That’s good because they carry no baggage and it gives potential investors a chance to get in at the same price as when the company did their IPO. Alejandro and his team have been busy mapping the land package in preparation for a major 10,000-meter drill program. They have completed an aerial magnetic and radiometric survey which shows two major crosscutting faults, one running NE/SW and another running EW. The company is well cashed up with a float of 36 million shares total and $17.5 million in cash. On July 11th, the company announced the commencement of the drill program at Santa Rosa. Alejandro has budgeted $4.5 million for this year’s exploration. They will have two core rigs drilling shortly. No one has ever done any modern exploration on the Santa Rosa project even though over 1700 surface rock samples show an oxide cap of 1.2 g/t gold and reports from the artisan miners show up to 98-g/t high-grade material. Any time you invest in a junior you are gambling. At best, you are buying a lottery ticket and at worst you are rolling dice. The key to successful investing is to buy only shares where the odds are in your favor. I saw only a small portion of the ground Red Eagle controls on their 100% owned Santa Rosa property. But I took samples, I panned gold and I was knocked out that this brand new company has been able to pick up such a commanding land position with so much potential. Another aspect and investors will like this, is they are drilling now and will have results in 8-12 weeks. This isn’t going to be your typical “Waiting for Godot” mining company. There will be results and I think they will be barn burning. I am highly biased toward Colombia in general and Antioquia in particular. Colombia was once the biggest gold producer in the world and I believe it will be again. Antioquia is the province where Medellin is located. While I was there I met with Nicolas Lopez, the Secretary of Mines for Antioquia. He’s a young, dynamic and very intelligent lawyer. He sees the potential in Colombia and Antioquia and is doing everything in his power to create a positive environment for junior mining companies in the province. Colombia is going to be a gold mining powerhouse. Dozens of companies will be in production. The business climate is right, the geological environment is right and the government is mining friendly. Colombia has been under the radar scope for 60 years but companies run by guys like Ian Slater who understand what is there are going to become major mining companies. You can invest in his vision today at the same price the company went public. The management team is super strong, the land position is sweet, Alejandro Kakarieka knows exactly what he needs to do and the drills are turning. It doesn’t get any better than that. It’s possible to invest now when there is perceived risk. I’ll suggest the risk is a lot lower than you might think and the potential higher. You have until the drill results start coming out to invest cheap. I don’t think it will be cheap after the results come out. I was panning gold at the surface right where they are going to drill. The issue isn’t, is there gold there? The issue is, how much gold is there? I love getting involved with companies at this stage. Ian has put together a team with a long history of success. It’s about to get longer. Red Eagle is soon to be an advertiser and we are biased. I don’t own any shares now because I didn’t know about the PP but on any decline I would be a buyer. As always, it’s your money to invest, we don’t share in your profits or your losses so take some responsibility for doing your own due diligence.

Red Eagle Mining

### Bob Moriarty |