| |||

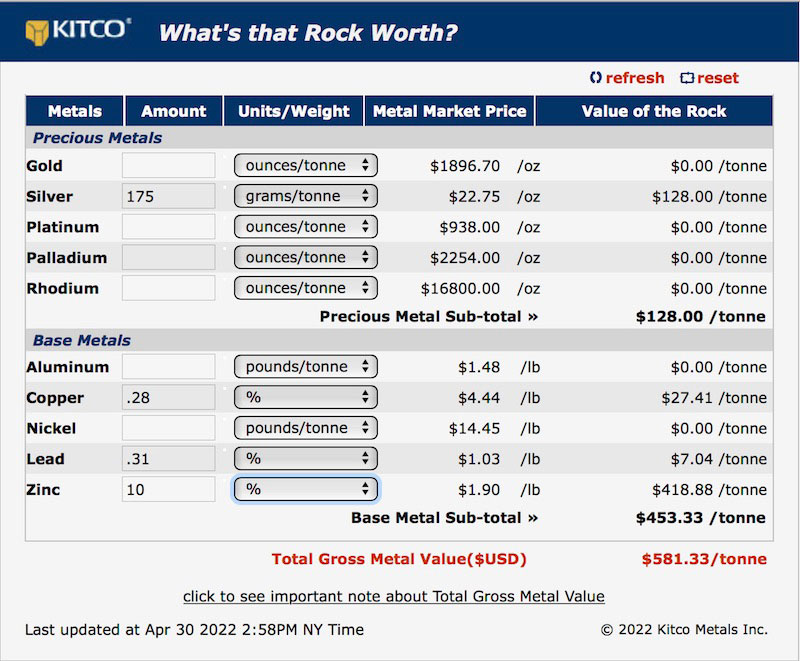

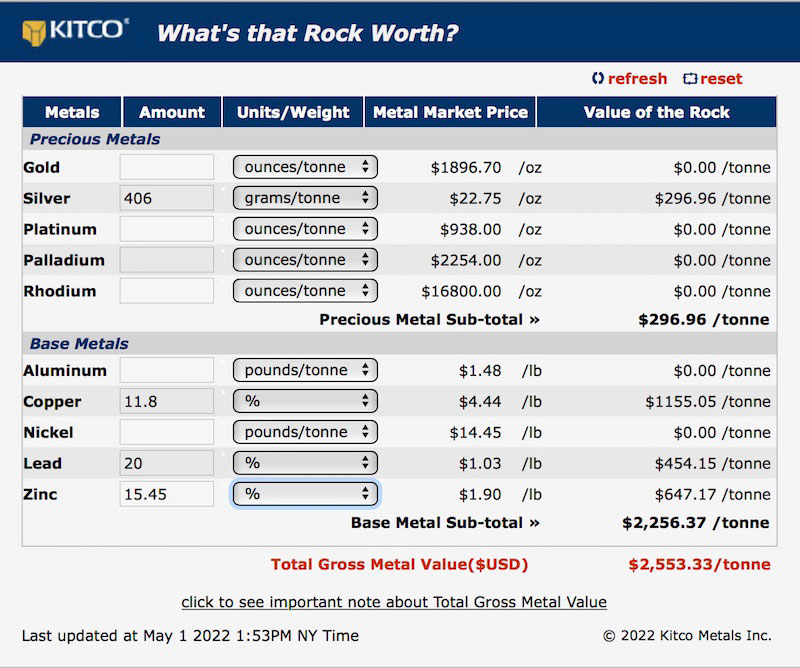

Core Advances Giant Carbonate Replacement Deposit in BCBob Moriarty I suspect that every investor in the junior resource space dreams of the day one of their stocks go up by hundreds or thousands of percent. Novo did it, going from $.25 to just short of $9. Eskay Mining rocketed higher from $.065 in 2019 to a high of $3.55 a short two years later. Eloro climbed from a low of $.30 to $5.89 in just under a year. It happens. Should you be lucky enough or wise enough to pick such a winner, you can make so much money you could retire with the gains on a single stock. I own some of one stock that sold for $.065 in August of 2021 and hit a high of $.88 a couple of weeks ago. That’s a 1250% gain in less than seven months. The stock is Core Assets (CC-C). With the kind of district potential CRD (Carbonate Replacement Deposit) and some already slick moves by management financially it might rise 1250% from today’s price again. Core is a new company that only began trading in late July of 2020. Their core asset is called the Blue deposit located about 48 km south of Atlin, BC. They picked up the project from Zimtu Capital in December of 2018 for $100,000 in cash and 3 million shares. Zimtu retains a 2% NSR that can be bought down to 1% for $1 million within five years of when the deal was done. Core is located in the very northern tip of British Columbia. 2021 was really the first year the company could get traction in exploration and they used the year wisely. A lot of eyes were focused on Core as they did an interesting placement in January of $1.6 million led by Crescat at $.24. Company President Nick Rodway deliberately kept the number of shares issued low and put a restriction on selling the shares. Rodway says he could have raised $10 million there was so much attention being paid towards the project but kept the amount down to the bare minimum necessary to pay for this year’s 5,000 meter drill program at Blue. Nick restricted sales of the shares in the PP to 1/3 of the total every six months. So investors can sell 1/3 in six months from closing, another 1/3 a year after closing and the last 1/3 eighteen months from closing. That way he limited the supply of shares that might hit the market. And there were about 12 million warrants at $.15 that jumped in price for the 2nd year in mid-March and 84% were exercised so as of mid-March the company was fully funded with just short of $4 million to finance this year’s drill program. I fully appreciate what Nick Rodway did with the restriction of the shares and forcing the exercise of the warrants. Traditionally when Vancouver or Toronto brokers hear of a pending finance for a company they short the shit out of the stock wanting to drive the PP price lower. They cover their shorts and put the money into the PP and three months and three weeks (a week short of the four month hold) they dump all their shares. As a result junior resource companies are under constant attack by the brokers who stand to make the most money. All at the expense of ordinary investors. This year the brokers shorted into the PP and were caught out at the airport when their ship arrived at the dock. As soon as the limited PP was filled without the brokers, they were forced to cover their shorts and the stock shot higher. Core began with two different properties in BC, the Blue project and the Silver Lime, both picked up from Zimtu. There had been prior work done in the area by Carmac in the 1990s on the two projects but they viewed the geology as a series of sulfide veins. Nick Rodman and his team thought Carmac lost sight of the forest because of all the trees in the way and concluded that the deposit is a massive District Scale CRD fed by a base metal rich porphyry system. All of the results released to date tend to show Core’s view is the correct one. The company has staked additional ground and now controls just over 108,000 ha. In mid-February Core released channel samples from ten different occurrences at the Sulphide City and Grizzly targets. High-grade mineralization between the two areas measured 600 meters by 350 meters. Grizzly CH21-05 showed assay values of 175 g/t Ag, 0.28% Cu, 0.38% Pb and 7.2% Zn. That is worth over $581 USD per tonne. It’s rich. (Click on images to enlarge) Two weeks later Nick announced grab sample results of 406 g/t Ag with 11.8% Cu greater than 20% lead and 15.45% Zinc. That rock is over $2550 USD per tonne. Of course grab samples and channel samples do not reflect the average grade of the project but you cannot get those kinds of numbers in a vacuum. This is a very rich CRD and big with indications of mineralization just at the Grizzly Manto Zone 6.6 km by 1.8 km and growing. Potential investors need to understand the incredible potential of CRD deposits. The Cinco de Mayo project powered Mag Silver to a 2 billion-market cap. South 32 paid $1.3 billion for the Taylor CRD from Arizona Mining. The Resolution Copper deposit is estimated to produce thirty billion pounds of copper over a forty-year mine life. As of today Core Assets has a market cap of about $74 million with just under $4 million in cash. It has billion dollars potential. You can do the math. Core is an advertiser. I have bought shares in the open market and participated in the last private placement and that makes me biased. Do your own due diligence. Core Assets Corp ### Bob Moriarty 321gold Ltd |

Copyright ©2001-2026 321gold Ltd. All Rights Reserved