| |||

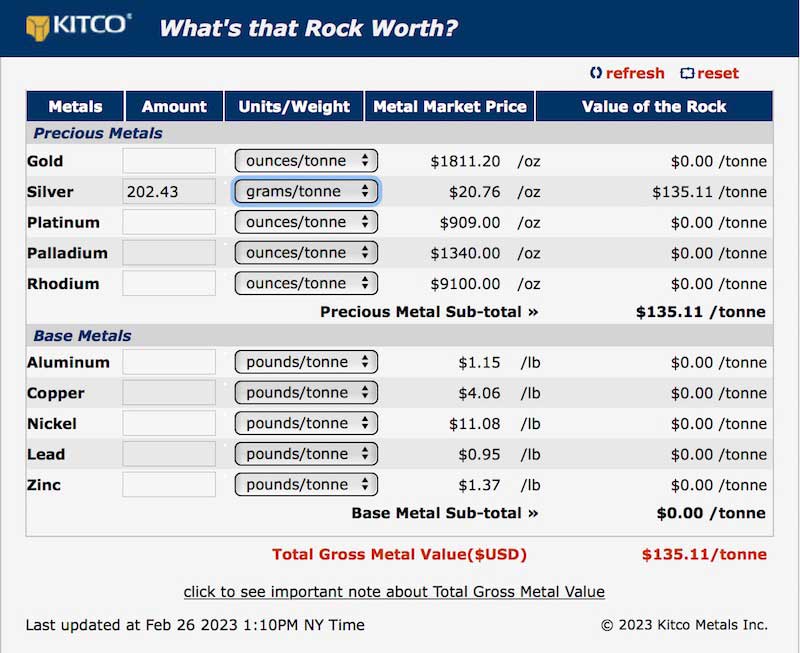

Eloro Drills a Cornucopia of RichesBob Moriarty I’ve heard it said that you could never be too rich or too beautiful. I’m not sure if it is true or not, since I have no experience with either. But as a junior resource company for certain you can have too successful a drill program. It’s true of New Found Gold. It’s true of Lion One and it’s really true of Eloro (ELO-V). Each of those companies has hit so many home run holes that frankly investors don’t know what the companies are worth since it is outside their frame of reference. The drill holes are just too good to understand. On January 31st Eloro announced hole DHK-27 showing 325.48 meters of 202.43 g/t Ag worth $135 a tonne in USD or $184 a tonne in CAD. That is a giant and world-class hole. But when you have hundreds of world-class holes in one deposit such as Iska Iska in Bolivia, what have you got in total? (Click on image to enlarge) That’s where it really gets interesting. We are not going to know just how big Iska Iska is as a mine for probably fifty years or more. So far the ELO technical team have drilled 84,495 meters in 122 holes. In a press release from last year, Dr. Bill Pearson showed the potential for a strike length of 2,000 meters with a width of 1,000 meters and a depth of at least 800 meters. If you throw those numbers in your Bomar Brain and use a typical specific gravity of 2.65 tonnes per cubic meter you get 1.6 billion cubic meters with 4.24 billion tonnes of rock. It’s not going to all be mineralized but saying a potential of 1.5 billion tonnes of ore is possible. The simple reason I said that we wouldn’t know how much ore the mine contains for probably fifty years or more is because of the law of big numbers. It doesn’t make sense at all to drill what you can’t mine for a long time. If the company mined 120,000 tonnes per day it would be about 43 million tonnes per year in total. With a potential total of 1.5 billion tonnes you have a potentially large mine for 35 years. Why drill off what you don’t need to count for a long time? 43-101 has forced a focus on defining a resource. In some ways, that is a noose around the neck of the mining or exploration company with a lot of companies thinking of nothing but generating a giant resource. What investors do need and will have in the next month or so should the company make their planned time line is a 43-101 resource showing just what they have in minerals already defined. If you pointed a gun at my head, I would guess it would be in the 400 million to 700 million tonnes of $100 to $125 CAD a tonne rocks at today’s prices. That’s ten to fifteen years production of rock worth maybe $115 a tonne or production of about $5 billion a year in total revenue. When you have a mine with the potential of Iska Iska there are other factors that determine how big you go. There will need to be a rail line. It’s very high elevation at 4,000 meters and that will be a challenge for finding and training people. That is about 13,100 feet. Power will be an issue. It’s way early to speculate too much about how they would put it into production but we can come up with some solid numbers in the next month when the 43-101 comes out. A mine and mill that size will cost in the $1.5 to $2 billion area. Eloro will not mine Iska Iska. It is not in their skill set. They don’t want to be miners but Chinese and Korean and Japanese smelters need feed and having a dependable source of supply for many years will be very attractive. There are probably half a dozen big mining companies who will be interested in Iska Iska at a price. It will not sell for ore in the ground. The majors can look at the grade and resource and do an easy back of the envelope calculation as to how many years production there will be. I’m going to guess a margin pre-tax of 20-30% and that would put Iska Iska near the top of attractiveness. In addition there appears to be a tin component where there appears to be two different porphyries, a silver rich, lead and zinc porphyry and a tin rich buried porphyry that would give a mining company some flexibility in what they mine and process at any given time. You are not going to come across very many projects that are world class and still have a high Return On Investment. Eloro has both. And the stock is cheap right now because frankly until the 43-101 comes out this month you can just make up any number you want. Eloro is an advertiser. I have bought a lot of shares in the open market and in private placements. It is one of my larger positions. I am biased, so do your own due diligence, please. Eloro Resources Ltd ### Bob Moriarty 321gold Ltd |

Copyright ©2001-2026 321gold Ltd. All Rights Reserved