Think ZINC: Or the Next Big Thing Think ZINC: Or the Next Big Thing

Bob Moriarty

Archives

Feb 18, 2008

I spent an exciting two weeks

in South America recently where I saw some of the best projects

I have seen in a long time. First I visited Lima where I toured

a silver-zinc-lead project that blew my socks off and I think

it will interest you.

Astute readers (are there any

others visiting 321gold?) may well remember that I have been

warning of a slowdown in base metals for almost a year. But

if that's what I believe, why am I in love with a silver-zinc-lead

project?

I'm a contrarian. It's my job

to measure the temperature of the herd as best I can and figure

out where the next stampede is headed. Too many people were in

love with zinc, the price rocketed to $2.10 in December of 2006.

Soon thereafter, lead shot up to $1.80 by October of 2007. I've

been to China several times in the last couple of years. I know

what importance they are putting into their Coming of Age Party,

the Olympics. You can backtrack and figure that they pretty much

bought every ounce of lead and zinc a year in advance. So a slowdown

in Chinese production wasn't brain surgery.

We've had our slowdown; zinc

dropped to $.98 a couple of weeks ago and lead dropped to $1.10

in December. I was uncomfortable with zinc above $2 and with

lead nearby but I'm comfortable at these prices with both. Now

is a wonderful time to be buying a near-term producer.

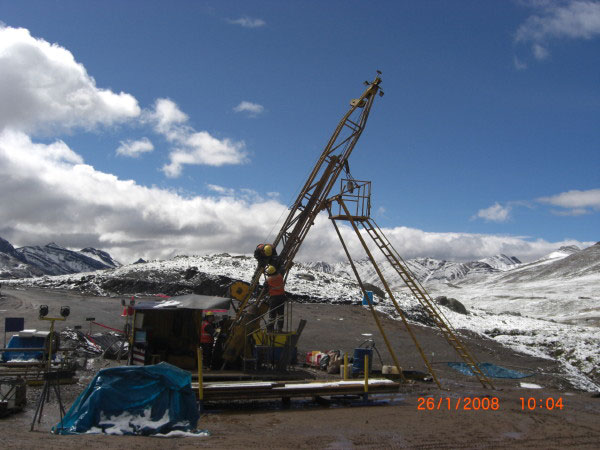

The Santander silver-lead-zinc

mine began production some 50 years ago under St Joseph Minerals.

The company started production on a silver-lead-zinc carbonate

hosted replacement system about 200 kilometers Northeast of Lima,

Peru in the high Andes. The project is located at 4600 meters

or 15,200 feet.

Peru used to have some silly

assed rules about business. St Jo mined the property for a few

years then sold it to the contractors. In 50 years, some 8 million

tons of about 10% combined lead-zinc with 2 ounce silver ore

was mined. But the country required the company to sell the product

internationally and to remit the funds to the government. If

the product sold for 3 soles, the government would credit them

1.5 soles or a NSR of 50%. It doesn't matter how rich a mine

is, you can't make money when the government is literally stealing

50% of what you sell for. And their expenses were all in the

higher 3 soles exchange rate. The mine was never profitable.

As a result, short cuts were taken on maintenance and it shows.

15 years ago, the project,

now under local ownership, went into bankruptcy. There is an

existing 1000 TPD mill and facilities for 1000 workers. A stupid-wild-assed-guess

would put the value of the plant and equipment at maybe $100

million. Best of all, the project comes with it's own hydroelectric

power plant located some 17 KM away. I figure that's easily worth

$20 million. It produces 2 MW now but management has plans to

upgrade the facility to 8 MW in order to sell 3 MW and use 5

MW in an upgraded 4000 TPD mill planned down the road.

Trevali Resources (CNQ:ZINC) announced

the assumption of the project [pdf] a couple of months

ago. Terms are fairly simple. They issued 2 million shares

and agreed to pay the debts of the bankrupt company and are paying

$100,000 in a lease payment monthly for a 50 year lease with

an automatic 50 year extension and payment of a 3.5% NSR. So

far they have spent about $5 million buying down 91% of the debt.

It's a great deal for both companies, the bankrupt company and

for ZINC.

Carlos Ballon, also director and VP of Cardero Resources,

is Chairman and CEO of Trevali. Mark Cruise, Cardero Resources

VP of Exploration, is the President. For now, each is actually

operating one level lower than his pay grade. I drove to the

power plant with Carlos at 2600 meters elevation where we spent

the night. The next day we continued to 4600 meters to the plant

and mine.

The nicest thing I can say

about Carlos is that he is a slave driver cracking the whip over

his entire crew. Everyone involved is 1st class and is hustling.

Mark Cruise is supervising a massive drill program to define

a major ore body. As the project comes on stream, they will revert

to a more managerial role but for now I fully approve. Crack

the whip.

The plan is for Mark to outline

5-6 million tons of maybe 13% combined lead-zinc, with maybe

4 ounce silver ready for immediate production. The goal is maybe

10 million tons in total in a year. The system is a carbonate

replacement system. These systems typically occur in clusters.

Carlos wants the plant in production

in June. The refurb cost to bring the mill to professional standards

at 1000 TPD is $3 million. It's very ambitious but all of the

people I saw at Santander were motivated. Carlos is setting a

very high bar right from the gitgo. Everyone wears and uses safety

equipment and undergoes a physical examination to make sure they

can take the 15,000-foot elevation before they are allowed on

site. He makes it clear that safety is paramount. I was impressed.

The immediate plan is to begin

processing the tailings that grade about 3% lead-zinc and 15-gram

silver. I've put a chart below to give readers an idea of the

gross metal value of such rock. Remember, this stuff has already

been crushed and ground so he can be processing and still upgrading

his crushing circuit. The rock is worth about $87 per ton today.

That doesn't mean they will recover $87, the real figure will

be much less. But they are expecting $8 to $10 cost of production

per ton so even from the first; cash flow is going to be nice.

As Carlos is getting the plant

ready, Mark is working on the mining side with Les Oldham. They

have an aggressive drill program in progress. I saw core from

the Magistral Norte area, one of four already identified drill

targets. The intercepts are very high grade and quite wide. Trevali

has finished 18 holes; mineralization appears to be increasing

with depth. A back of the envelope calculation showed me they

have already identified over 3 million tons of high-grade ore.

As the crushing circuit is brought to speed, ZINC will begin

to add high-grade ore to the tailings ore. A glance at the chart

below shows what's going to happen to cash flow as the plant

comes up to full speed.

We can only guess where prices

will be for metals a year from now when Carlos and Mark believe

they will be in full production at 1000 TPD but my rough figures

show $60 million a year in cash flow. If I am right on my prediction

of where metals prices are headed and what Bernanke is going

to do to the dollar, at 4000 TPD, the figures go off the charts.

This is going to be a big deal and a profitable deal.

Carlos doesn't have a firm

date on the 4000 TPD production target. Much of it depends on

how fast Mark and Les can define ore. They are presently drilling

only the first of four very significant high-grade bodies that

come right to the surface. Given that the old Santander pipe

was mined to 500 meters depth and remains open to depth, it's

clear that the project has tremendous upside exploration potential.

Two diamond core drill rigs are on site turning and a third will

be added by the time you read this. They have also completed

a detailed geophysical survey of the 4455-hectare property and

have identified 6 additional look-alike anomalies. Odds are that

some will turn into ore bodies, remember, carbonate replacement

systems come in clusters. The total cost to get it up to 4000

TPD looks to be in the $4.5 to $5.5 million-dollar area. That's

not a problem; the company has over $8 million in the bank today.

In any business, managers always

seek to create some kind of competitive advantage. You have to

be better than the competition at something or they will control

your business. Part of this project that I think is ultra-important

is the power station. It's located at an elevation of 8500 feet

or 2600 meters. The river there runs 12 months a year. The drop

is steep so the water is fast. Previous operators put in a Pelton

Wheel driven power station now capable of delivering 2MW. The

plant is located some 17km from the mine. Trevali will have to

increase the flow of water to the station, install more Pelton

Wheels and generators and upgrade the line going to the mine.

When that is complete, they will not just have free power, it

will have a negative cost as they will be selling about 40% of

what they generate and the income will pay all of the expense

of power generation.

I don't want anyone believing

this is going to simply be another Silvercorp [TSX-SVM],

rocketing from $.30 to $10 in three years. No, not at all. Silvercorp

has about 1.25 million tons of high-grade ore averaging 45-ounce

silver and 35% combined lead-zinc. Silvercorp has 7 times the

silver grade and almost three times the lead-zinc grade. No,

Silvercorp has far better ore. Of course it looks as if ZINC

has 8 times the total amount of rock and that number could easily

grow. This is going to be a lot better than Silvercorp.

Silvercorp wants to quadruple

output to 3000 tons per day in a year when Trevali could be producing

4000 tpd soon thereafter. There may well be a period where Trevali

produces more metal than Silvercorp. Today SVM has a $1.4 billion

dollar market cap and ZINC has about a $50 million dollar market

cap.

Carlos had a consultant do

a research study on the value of similar Peruvian mining companies.

I think the numbers were a little biased against the local companies

because a Canadian listed company is going to get a higher capitalization

than a Lima listed company. The results showed that companies

got between $800 and $900 per ton of zinc equalivant. If Mark

Cruise and Les Oldham can scratch up 10 million tons of ore grading

13% zinc and 6 ounce silver, that would be similar to 17% zinc.

10 million metric tons at $900 a ton of zinc at 17% would be

a market cap of $1.5 billion. It's perfectly reasonable.

There are a number of companies

loosely associated in the Cardero-Henk Van Alphen fold. Athlone

Energy (ATH-V), Wealth Minerals (WML-V), International Tower

Hill (ITH-V) and of course Cardero Resources (CDU-V). Each of

these companies have great projects and just can't seem to raise

traction. A good part of the problem is communication and I have

spent a lot of time beating their IR people over the head in

an effort to get them to do a better job of communication.

I suspect that with all the

activity at Santander, Carlos Ballon and Mark Cruise are going

to force the rest of the crew into increasing their speed of

action. It takes a high energy level to put a mine and mill back

into production and you not only need to act now, you need to

communicate now. For example, ATH is producing 630 barrels of

oil a day. That should be worth $50,000 in market cap per barrel.

The price of oil says ATH should be worth $31.5 million. But

the market only values ATH at $15 million. A large part of the

reason is because they refuse to communicate. Basically if you

don't communicate your story, you don't have a story.

Cardero is doing a long overdue

scoping study on their Pampa de Pongo Iron Deposit in Peru. Iron

ore should be worth about $2 a ton in market cap. PDP has a 953

million ton resource. That implies a $1.8 billion dollar cap

for Cardero if the market understood what they have. The market

does not and the current market cap is about $55 million.

By getting Santander into production

in record time, the management team of Trevali is not only going

to lift their market value, they are going to focus very positive

attention on the rest of the stable. And I suspect this is going

to be one of the big market hits where a lot of people make a

lot of money.

If Carlos needs someone to

polish his bull whip or iron it or do whatever you do with a

bull whip in between beatings, I'll be happy to do it. I want

to see the entire group do what I have believed all along they

could do.

As you can reasonably surmise,

I am a shareholder in ZINC. They are soon to be an advertiser

and I am as biased as I can be. They have a lot of work ahead

of them to accomplish their goals but it's all reasonable and

possible. As negative as I am on the future of the economy in

the US, I am positive for the rest of the world. There will be

demand for silver as money and for lead-zinc as commodities.

If the American consumer is tapped out, I'm sure some of those

wonderful 1.3 billion Chinese who save almost 50% of their incomes

will step in and do some consumption of their own.

Trevali Resources Corp

CNQ:ZINC $2.40 Canadian (Feb 15, 2008)

OTCBB:TREVF

28.8 million shares

Trevali Resources Corp website

###

Feb 18, 2008

Bob Moriarty

President: 321gold

Archives

321gold Ltd

|