| |||

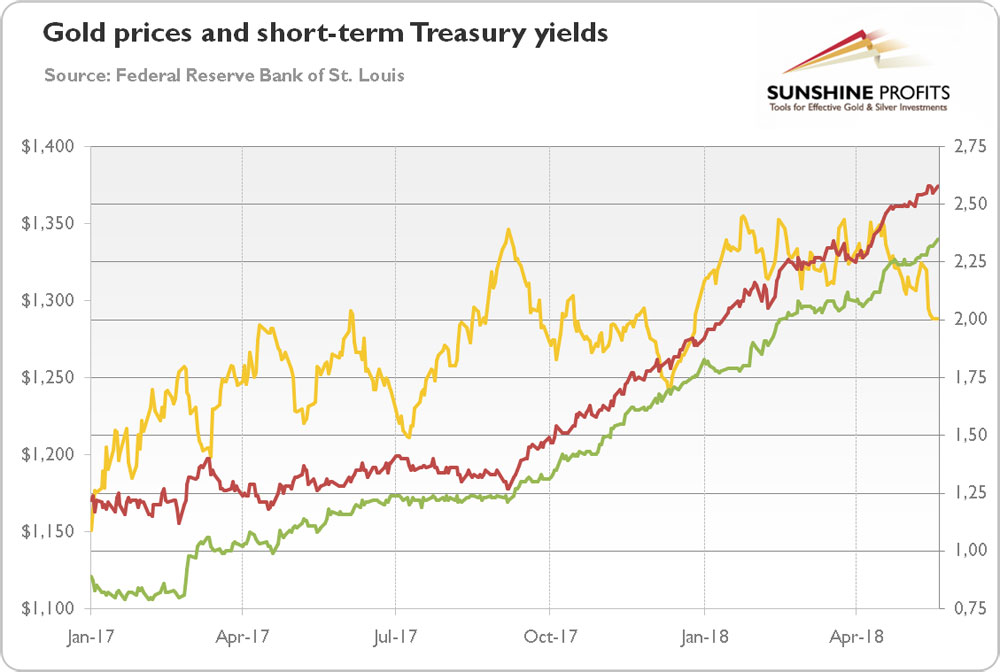

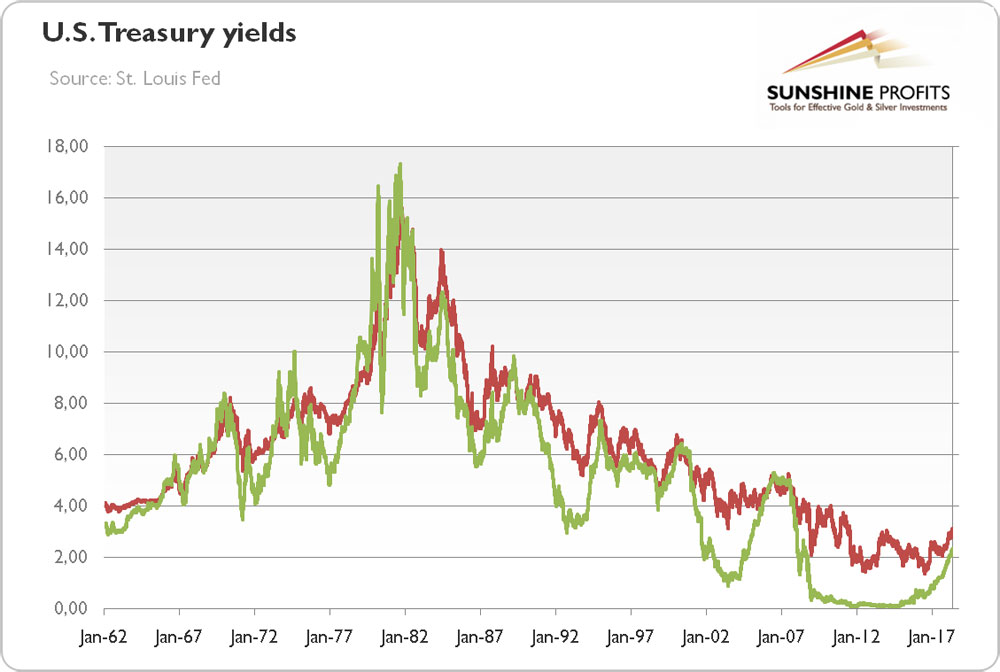

How Long Can This Last?Arkadiusz Sieron Yields are rising. The global economy has adapted so far without any major problems. So far. But how long can this last? And what does it ultimately mean for the gold market? Let’s look at the chart below. As one can see, the U.S. long-term interest rates have been rising since September 2017. And they breached 3 percent in the second quarter of 2018, attracting investors’ attention all over the world. Chart 1: Gold prices (yellow line, left axis, London P.M. Fix, in $) and the 10-year U.S. Treasury yields (red line, right axis, in %) from January 2017 to May 2018. (Click on images to enlarge) However, although the recent moves in the 10-year yields are of great importance, higher short-term yields might also be problematic. Please take a look at the next chart, which paints 1-year and 2-year Treasury yields. They have also been surging recently: the 2-year yields have jumped above 2.5 percent, the highest level since 2008. For some analysts, the rally in short-term yields is even scarier, as they are more relevant in daily life of many consumers and investors. Chart 2: Gold prices (yellow line, left axis, London P.M. Fix, in $), the 2-year U.S. Treasury yields (red line, right axis, in %), and 1-year U.S. Treasury yields (green line, right axis, in %) from January 2017 to May 2018. Anyway, all interest rates have been rising, making many people nervous. Why are they worried? Well, higher interest rates mean greater costs for debtors. Consumers and investors have to pay more for their loans. The debt-service costs increase for companies, putting them in troubles. It’s no coincidence that practically all the Fed’s tightening cycles preceded the recessions. Moreover, the Fed’s actions have important consequences not only for America, but for the whole globe. When the U.S. interest rates rise and the greenback appreciates, it implies problems for many emerging countries which are heavily indebted in U.S. dollar. Analysts estimate that households, companies and governments loaded up on $40 trillion of debt taking advantage of ultra low interest rates after the Great Recession. The recent crisis in Argentina (who can count them?) may be the canary in a coal mine, warning of the lethal effects of rising interest rates and a strengthening dollar on countries that depend heavily on foreign debt (remember taper tantrum in 2013?). But should investors panic? No. We argue that rising yields indicate changing macroeconomic condition, not a doomsday scenario. Why? Firstly, the yields rose because the economy improved. The U.S. central bank has finally started to unwind its massive balance sheet and to hike the federal funds rate in response to healthier labor market and stronger overall economy. Second, the interest rates have gradually marched higher – it was not a sudden jump. Just look at the chart below, which shows the 10-year Treasury yields since 1962. If you examine it closely, you will see that the recent rise in yields has been rather benign. Actually, you can barely notice that “deathly move” on a long-term chart. Instead, you can see that the 10-year yields jumped above 3 percent both in 2011 and 2014 – and the sky did not fall. Chart 3: U.S. 10-year Treasury yields (red line) and U.S. 1-year Treasury yields (green line) from 1962 to 2018. What does that discussion mean for the gold market? Well, we don’t have good news. Higher interest rates may be harmful for debtors (but creditors benefit), including emerging markets. However, what is really scary are the short and rapid changes, not long and slow interest rate increases. It means that – contrary to what the sellers of scary narrative try to peddle – the doomsday scenario is not likely in the near future. Hence, gold will not shine as a safe-haven asset during the allegedly upcoming bond market crash. And investors should remember that during emerging market crises, the U.S. dollar usually appreciates – which is clearly bad for bullion – as investors shift their funds into America. But, hey, gold bulls, the case is not lost! The yellow metal also does not like high interest rates. During rapid moves, gold could plunge easily. But when interest rates climb steadily (as inflation remains limited), the shiny metal may stay afloat. It is similar to inflation: gold shines only during high and accelerating inflation, not during mild inflationary periods. The world is non-linear. Investors’ sentiment is non-linear. We don’t notice small price increases (or modest upward moves in yields), only huge and persistent inflation is able to pull us out of the comfortable numbness. However, rapidly appreciating dollar is a different kettle of fish… Stay tuned! If you enjoyed the above analysis and would you like to know more about the link between rising yields and the gold market, we invite you to read the June Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign me up! Thank you. ### Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts. 321gold Ltd |