Precious Metals Market Timing

The Interest Rate Conundrum

Ron Rosen

Jun 13, 2005

Conundrum

(NOUN) = MYSTERY, PUZZLE SOLUTION

ON LAST TWO PAGES

FRBSF Economic Letter

2005-08; April 29,

2005

The Long-term Interest Rate Conundrum: Not Unraveled Yet

In congressional testimony

on February 16, 2005, Federal Reserve Chairman Greenspan characterized

the recent behavior of long-term interest rates as a "conundrum."

Typically, long-term rates tend to rise as monetary policymakers

raise short-term rates. But not in the current episode. Despite

steady monetary tightening beginning in the middle of 2004, the

yields on long-term U.S. Treasury securities actually have declined

since then by about 50 basis points. As a consequence, the current

level of long-term interest rates seems to be well below what

one would expect on the basis of economic fundamentals.

----------

By DAVID LEONHARDT

Published: June 10, 2005

For the last year, the Federal

Reserve has been conducting a relentless campaign to raise interest

rates. In that same year, the rates that matter the most to many

people - mortgage rates - have drifted back down, returning to

near 30-year lows.

Testifying before Congress

yesterday, Alan Greenspan, the Fed chairman, called the current

situation "clearly without recent precedent." Even

as the Fed has lifted its benchmark short-term rate eight times

since last summer in an effort to choke off inflation, the average

rate on a 30-year mortgage has fallen to 5.61 percent, from 6.3

percent, according to BankRate.com. Mortgage rates are now slightly

higher than they were in 2003, when they were the lowest in at

least three decades.

In effect, the bond market

- where long-term interest rates, including those for mortgages,

are set - is stimulating the economy while the Fed is trying

to stabilize it.

----------

June 9, 2005

NEWS ANALYSIS

by Rich Miller

No matter how meager the

yields, bond buyers are insatiable. But why? Greenspan &

Co. can't say -- but they're sure noticing.

Back in February, when he first

addressed the issue of stubbornly low bond yields, Federal Reserve

Chairman Alan Greenspan called it a "conundrum." The

mystery revolved around a simple question: Why were long-term

interest rates falling even as the central bank was jacking up

short-term rates? Back then, Greenspan ventured that the anomaly

could be a temporary aberration and that in no time, bond yields

might start acting in more traditional ways.

More than three months -- and

two more rate hikes -- later, bond yields have once again been

falling, surprising not only Greenspan but many market pros as

well. Indeed, in early June, yields on 10-year Treasury securities

fell sharply, to below 4%. Greenspan doesn't think the falling

yields are a sign of slower growth ahead, as many in the market

believe. Indeed, he's expected to tell a congressional hearing

on June 9 that the economic expansion remains solidly on track.

HERETICAL THOUGHTS. But even with the economy powering

forward, Greenspan seems increasingly convinced low bond yields

may be an enduring phenomenon, driven by a complex of international

forces the Fed has yet to fully understand.

----------

ANGRY BEAR

Wednesday, June 01, 2005

The Long-term Interest Rate

Mystery

As I start getting reacquainted

with the financial press following my 10-day 'vacation', the

first thing that has caught my attention is the continued fall

in long-term interest rates. The 'conundrum' about which Alan

Greenspan spoke a few months ago has not resolved itself, after

briefly

appearing as though it might back in March. Instead, the

mystery has deepened, in the sense that long-term interest rates

have fallen noticeably over the past month or two even though

the Fed continues to increase short-term interest rates.

Of particular surprise to many

observers, in recent weeks the bond market has completely reversed

the rise in yields that we saw a couple of months ago. This resounding

defeat of the bond market bears has been so striking as to convince

some of them, like Stephen Roach, to give up being a bear altogether.

----------

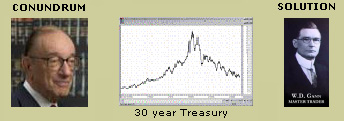

60 YEAR INTEREST RATE CYCLE

Long interest rates bottomed

in 1946. It may be difficult to believe but we are headed for

a bottom 60 years later in 2006. This is happening in spite of

much being written about a coming dollar collapse and sharply

rising interest rates. The economic and financial leaders of

this country are completely perplexed as to why long interest

rates are still going down. The Chairman of The Federal Reserve

Board, Allan Greenspan, says it is a conundrum. He is raising

short term rates but long term rates seem to have a mind of their

own and refuse to follow his lead, thus a conundrum.

However the Maestro of time

and cycles, W.D. Gann, has this to say.

"The future is but a repetition

of the past. "The thing that hath been, it is that which

shall be; and that which is done, is that which shall be done,

and there is no new thing under the sun." -Ecclesiastes

3:1. In order to be accurate in forecasting the future, you must

know the major cycles. I have experimented and compared past

markets in order to locate the major and minor cycles and determine

in what years the cycles repeat in the future." "Time

is the most important factor in determining market movements

because the future is but a repetition of the past and each market

movement is working out time in relation to some previous time

cycle."

The master cycles that most

affect our lives are the 30 and 60 year cycles.

"There have been only

3 historic lows (price) in 140 years. These occurred in 1864,

1920, and 1981. The time periods between these lows were 56 years

and 61 years. It is this 60 year cycle which is especially intriguing."

-James Flanagan of Past, Present, Futures; an excellent

source of Historical market information.

What is currently happening

in the long term Treasury bond market should help us understand

the cyclic nature of the precious metals markets, shares included.

I do not mean this as an insult to anyone or any institution

but it does seem that the more economic degrees one has and the

greater their position of importance in the world of finance

the more they believe that they can control the system and the

system will respond to their actions and maneuvers. It appears

to me that the only time the system responds to their maneuvers

is when unknowingly their maneuvers coincide with the cycles.

They are most likely not aware of this and mistakenly credit

their actions with the result. Those of us who lack the PHD,

MBA and other economic background in some ways are most fortunate.

We are not inclined to think that our education has given us

the tools to control nature. We are more likely to realize that

we best "Go with the flow" for whatever reasons and

don't fight it. The chart below is an excellent demonstration

of the 60 year interest rate cycle.

click image

to enlarge the chart

Subscriptions to the Precious

Metals Timing letter are available thru the Delta Society International

www.trade-Delta.com

- click on Ron Rosen Timing Letter for instructions on how to

subscribe.

In spite of my attending Washington

and Jefferson College and then 4 years later New York University

this is where my education first began. An education like this

helps keep ones feet on the ground, no pun intended. I surely

hate war as much as anybody but service, ex war, would be a great

education for every citizen. Service of some kind where you meet

your fellow citizens is a most beneficial learning experience.

You learn about folks that you might otherwise never come in

contact with. The more you learn about people and yourself the

better your market insights will be. That's me in the middle

facing inboard.

Jun 10, 2005

Ron Rosen

email: rrosen5@tampabay.rr.com

Subscriptions

are available at:

www.wilder-concepts.com/rosenletter.aspx

Disclaimer: The contents of this

letter represent the opinions of Ronald L. Rosen and Alistair

Gilbert. Nothing contained herein is intended as investment

advice or recommendations for specific investment decisions, and

you should not rely on it as such. Ronald L. Rosen and Alistair

Gilbert are not registered investment advisors. Information and

analysis above are derived from sources and using methods believed

to be reliable, but Ronald L. Rosen and Alistair Gilbert cannot

accept responsibility for any trading losses you may incur as

a result of your reliance on this analysis and will not be held

liable for the consequence of reliance upon any opinion or statement

contained herein or any omission. Individuals should consult with

their broker and personal financial advisors before engaging in

any trading activities. Do your own due diligence regarding personal

investment decisions. Disclaimer: The contents of this

letter represent the opinions of Ronald L. Rosen and Alistair

Gilbert. Nothing contained herein is intended as investment

advice or recommendations for specific investment decisions, and

you should not rely on it as such. Ronald L. Rosen and Alistair

Gilbert are not registered investment advisors. Information and

analysis above are derived from sources and using methods believed

to be reliable, but Ronald L. Rosen and Alistair Gilbert cannot

accept responsibility for any trading losses you may incur as

a result of your reliance on this analysis and will not be held

liable for the consequence of reliance upon any opinion or statement

contained herein or any omission. Individuals should consult with

their broker and personal financial advisors before engaging in

any trading activities. Do your own due diligence regarding personal

investment decisions.

The Delta Story

Tee charts reproduced

courtesy of The Delta Society International.

321gold Inc

|