| |||

Zinc News...And Zinc RealitiesGwen Preston

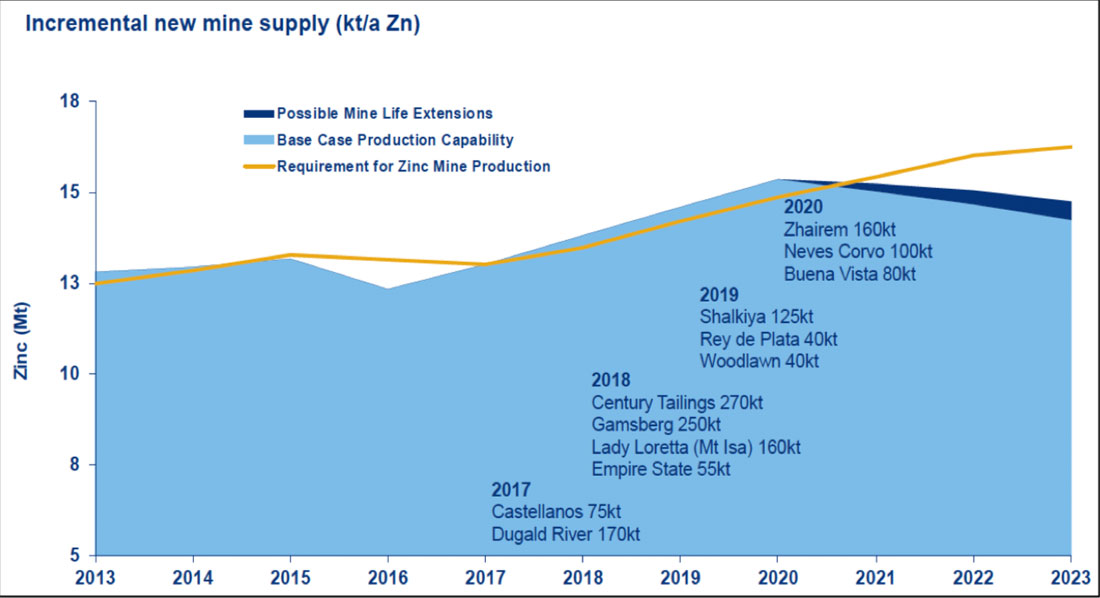

Zinc bucked the downtrend for metals last week by rising to a three-week high. The benchmark price on the London Metal Exchange (LME) was US$2,700 a tonne, rising 18% from a 22-month low in August, but still down significantly from the 52-week high of US$3,610.54 per tonne. (Click on images to enlarge) The driver for the price jump was supply tightness. LME stocks are low at just 99,900 tonnes and it’s the same story in Shanghai where inventories sit at 53,500 tonnes. The price also benefited after the International Lead and Zinc Study Group made revisions to its supply-demand forecasts last week. The group increased its expected 2018 global supply deficit to 322,000 tonnes, from 263,000 tonnes forecast earlier in the year. The revisions were made mostly because mine production growth has been slower than expected, at 2% compared to 5.1% forecast in April. In addition supplies from China, the world’s largest zinc producer, are also expected to contract by 2.5% this year, due to tighter environmental controls from Beijing that continue to force mine shutdowns. The new mines and mine expansions that were supposed to fuel that 5.1% supply growth this year are still underway. The new supplies aren’t missing; they’re just delayed to 2019. The study group now expects global mine production to surge 6.4% next year, with refined output accelerating 3%. Combine rising zinc output with trade wars – which are potentially getting worse, with the White House now threatening to apply tariffs to all the remaining US$200-billion worth of Chinese imports if negotiations don’t go their way in November – and the near-term outlook dims a bit for zinc. Investors are sensibly worried that trade wars will slow global economic growth at the same time as zinc supplies start to ramp up. As a result, in August S&P lowered its zinc forecast for this year and next, from an assumed US$3200 per tonne for the rest of 2018 to US$2800, and from US$3000 a tonne to US$2800 a tonne in 2019. That’s still higher than where it is today, but far from zinc’s high of US$3,610 per tonne at the start of the year. S&P said the revisions reflected its expectation for higher supply amid relatively tepid demand growth. However, zinc at US$2800 per tonne is close to the marginal cost of production for about 75% of the zinc produced globally. Marginal pricing is not sufficient incentive to build new mines. Mines are expensive, in terms of time and money, and so they don’t get built based on marginal economics. And yet new mines are needed. They aren’t needed in 2019, but they are needed within a few years. Zinc prices were boring for many years. A group of massive mines churned out enough supply to meet demand and that stabilized the price. There were occasional spikes, like in 2007 when a few supply issues reared up, but it was mostly a boring arena. Boring meant explorers didn’t bother with zinc. For decades. And that lack of attention means there is a true dearth of advanced projects that stand a chance of being ready to become mines in time to meet that supply gap. We’ve just come through the first phase of the zinc supply shortage. The closures of several huge mines from 2014 to 2016 pushed the price way up. The short list of supplies that were ready to be brought online are now answering that call. But they aren’t enough and now the cupboard is really dry, with nothing available to answer the supply gap that opens up in two years. Will 2019 be a strong zinc year? It’s a good question. I think the zinc price will be boring – it’s gone through enough excitement in the last two years! – with a down trend if trade wars continue to dominate headlines and a sideways-to-slightly-up bent if trade wars ease. As long as the price of zinc doesn’t plummet (which I think unlikely), though, I think that even with a boring zinc price the short list of advanced zinc projects will do well. The market will understand that these assets are rare and needed. And I predict a takeover or two as zinc majors scramble to sort out new mines. Zinc headlines will be what they will. Reports of rising supplies and lower prices next year are something new and easy to write about, more so than the simple, ongoing, unchanged story of insufficient supply in the medium-term to meet demand. Had these reports not come out, I bet the headlines would have focused solely on the incredibly low stockpiles in London and Shanghai, and come to a more bullish conclusion. Short-term moves matter if you are a trader. I don’t trade mining stocks; I buy because I have an evidence-based belief that a sector is set to perform and because, within that, a particular stock makes sense to me. From that vantage point, I am very content to continue owning Fireweed Zinc, Tinka Resources, and Vendetta Mining because they are all on that very short list of advanced zinc assets and therefore I think stand to do fine in the near term – and very well beyond. Oct 31, 2018 EDITORIAL POLICY AND COPYRIGHT: Companies are selected based solely on merit; fees are not paid. This document is protected by copyright laws and may not be reproduced in any form for other than personal use without prior written consent from the publisher. DISCLAIMER: The information in this publication is not intended to be, nor shall constitute, an offer to sell or solicit any offer to buy any security. The information presented on this website is subject to change without notice, and neither Resource Maven (Maven) nor its affiliates assume any responsibility to update this information. Maven is not registered as a securities broker-dealer or an investment adviser in any jurisdiction. Additionally, it is not intended to be a complete description of the securities, markets, or developments referred to in the material. Maven cannot and does not assess, verify or guarantee the adequacy, accuracy or completeness of any information, the suitability or profitability of any particular investment, or the potential value of any investment or informational source. Additionally, Maven in no way warrants the solvency, financial condition, or investment advisability of any of the securities mentioned. Furthermore, Maven accepts no liability whatsoever for any direct or consequential loss arising from any use of our product, website, or other content. The reader bears responsibility for his/her own investment research and decisions and should seek the advice of a qualified investment advisor and investigate and fully understand any and all risks before investing. Information and statistical data contained in this website were obtained or derived from sources believed to be reliable. However, Maven does not represent that any such information, opinion or statistical data is accurate or complete and should not be relied upon as such. This publication may provide addresses of, or contain hyperlinks to, Internet websites. Maven has not reviewed the Internet website of any third party and takes no responsibility for the contents thereof. Each such address or hyperlink is provided solely for the convenience and information of this website's users, and the content of linked third-party websites is not in any way incorporated into this website. Those who choose to access such third- party websites or follow such hyperlinks do so at their own risk. The publisher, owner, writer or their affiliates may own securities of or may have participated in the financings of some or all of the companies mentioned in this publication. 321gold Ltd |