Global Watch

- The Gold Forecaster

The Central Bank Gold Agreement

of 2004 - Year 2

Julian D.W. Phillips

Oct 4, 2005

Excerpts from the "Global

Watch - The Gold Forecaster."

The Central Bank

Gold Agreement of 2004. - Year 2

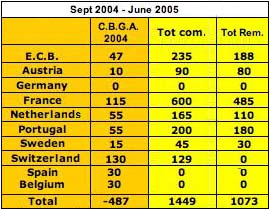

- Here is the table of sales

from last year [below]. Some have speculated that there is a

pattern, but we do not see any particular pattern, except that

it appears that the principle of disclosure of intention became

the disclosure of what has just happened. Indeed this covered

sales from bodies that had not disclosed any intention of selling

until it was subsequently disclosed. An educated guess would

favour changes of opinion on the part of some sellers, which

maintained the agreement's credibility. Indeed there does not

appear to be a programme of sales 'set in stone'. This could,

of course, be because they don't want one disclosed so as not

to unduly influence the gold price. But the pattern of behaviour

is not consistent with that. It appears more likely that some,

like Germany, have had second thoughts on their sales.

Source: World Gold Council

Notes:1) Germany has

only sold amounts minted into Coins -Not included in the Agreement.

2) The E.U. sold 53.8 tonnes unexpectedly, without naming the

source, so we cannot give

a future sales figure nor a residual amount to be sold.

Some have come along to sell

when perhaps this decision was not made prior to the agreement

being signed and some changed their mind after the event.

- The E.C.B. was a case in point.

They did not announce beforehand that they would sell. We now

believe they will sell 47 tonnes in each of the next four years.

To say that their intention is to maintain a 15% level in gold

of their reserves does not make sense as the gold price has risen

persistently and should continue to do so. Does this mean that

the measuring line is in Euros or in the U.S. $? Should their

gold sales be linked to the value of gold against the U.S. $,

a currency most appear to believe will fall? It is such a moving

target that one would have to conclude that the E.C.B. was favouring

the weak component of their reserves over the strong? Such a

bureaucratic reasoning defies good investment sense in that gold

is acting as a good counter to the weaknesses of both the ¤

and the $? To limit these sales to 227 tonnes would also defeat

the objective of a 15% level in reserves, because of the upward

mobility of gold. Hence our figure below must be a guess based

on the last sale.

- Germany is expected, by many,

to sell up to 600 tonnes, but dropped its option to sell last

year. Nothing has been heard from them since, so will they or

won't they? The reason given by them was that gold was a 'good

counter to the swings in the $' a feature it has demonstrated

to good effect of late! So why should they change this reasoning?

It is unlikely we will see any sales from them.

- France's sales tapered off,

surprisingly to us, with 17 tonnes of their not being seen as

part of the Agreement, it being a transaction with the B.I.S.,

but they did sell 115 tonnes it was reported, in all. It seems

likely they will continue to sell. We could see sales of 100

tonnes from Spain, but no announcement to that effect has been

made. Likewise Belgium is thought to be a possible seller of

another 100 tonnes, but no announcement has been made on this.All

in all, there is no certainty that the full amount of the 2500

tonnes will, or will not be sold. It appears this will only be

certain at the end of the fifth year. The protective wall of

silence and the uncertainty of the 'ceiling' being reached is

as clear as mud.

But what we do know from the above is that, as far as we

know for certain, a total of 1073 tonnes remains to be sold

over the next 4 years, an average of only 268.25 tonnes a year,

a far cry from the 'ceiling' of 500 tonnes a year!

- However, even this amount

could be sold up to the ceiling in the next two years, with no

more thereafter?

- Even 500 tonnes a year appears

at the moment not to be enough to cap the demand present in the

market.

Portfolio Progress

in South Africans

In the 13th June 2005 Issue

we recommended you buy four South African Gold Mines and hold

them for a year.

Here are the prices at which we recommended them and the prices

today:

| . |

Entry Prices |

Current Price |

% Increase |

| AngloGold

Ashanti |

$34.20 |

$43.20 |

+26.32% |

| Goldfields |

$10.50 |

$14.88 |

+41.71% |

| Harmony |

$7.50 |

$11.19 |

+49.2% |

| DRD

Gold |

$0.75 |

$1.39 |

+85.33% |

| Sasol |

$25.00 |

$38.70 |

+54.80% |

We believe there is much

more to come as the gold price rises and the average price of

gold the mines receive rises. These are not the only gold share

we like, just the South African ones we recommended.

You may well ask why we recommended

South African gold shares at all in view of the predatory

attitude towards South African mining on the part of the South

African government and its taxation policies. Primarily it is

because South African miners are amongst the best in the world

and they on a broad front are moving out of South Africa slowly

but surely and diversifying into more lucrative and more mining

friendly parts of the world. Already the cash flow from offshore

is substantial. Already it is clear they will be successful outside

the country and already they have made it clear they are taking

the companies offshore with them. Here are the comments of the

main-man-what-counts at Goldfields, Chris Thompson.

He said South African gold

mining companies would have to continue their move offshore if

their companies were to survive. "Unfortunately, the move

to offshore business has become politicised in South Africa,

even though geology has no politics," he said. "A company

with its foundations in South Africa is ending. The base is gone

and there's nowhere to go." South African gold mines were

getting deeper and the distance between the shafts and the mining

activities was also increasing. The inevitable outcome was an

increase in costs, Thompson said. "The industry is dying

and dropping fast."

In 1998 the South African gold

mining industry produced about 450 tonnes per year. It is looking

as though it will struggle to produce even 300 tonnes this year.

Gold Fields would continue to expand its offshore portfolio,

but as yet, there is no further clarity on whether corporate

activity with Polyus, the gold unit of Norilsk Nickel, which

owns about 20% of Gold Fields, would resume, but clearly there

is a synergy between the two with similar objectives.

- Harmony Gold has more than

90% of its output coming from South Africa.

- DRD GOLD has less than 40%

of its production in South Africa.

- AngloGold Ashanti produced

40-45% of its production in South Africa.

Oct 3, 2005

Julian D.W. Phillips

Disclaimer | Subscribe

email: gold-authenticmoney@iafrica.com

website: Gold-Authentic

Money

Recent Gold/Silver/$$$ essays at 321gold:

Jul 22 Is Wall Street Looking at the Wrong Chart? Carlton Preston 321gold

Jul 21 A Government Disease & A Golden Cure Stewart Thomson 321gold

Jul 19 Oil, Stk Mkt & Silver: Key Wave Counts captainewave 321gold

Jul 17 "Gold, Food, & Energy" - Key Sectors In Play Morris Hubbartt 321gold

Jul 17 Gold Stocks' Autumn Rally '26 Adam Hamilton 321gold

Jul 14 Gold Bugs Versus Mainstream Narrators Stewart Thomson 321gold

|

321gold Inc

|