China at a

Crossroads China at a

Crossroads

David Chapman

November 30, 2004

Over the past twenty five years the Chinese economy has been

nothing short of miraculous averaging roughly 9% per year. In

the process China has become one of the prime economic engines

of the entire world. During this period the Chinese economy went

from a totally command economy to one that maintains many of

the elements of a command economy but through reforms has opened

up more than anyone ever thought it would.

Despite economic reforms China is still ruled by one party and

dissidents are still subject to arrest. But with numerous economic

reforms and freedom has come the demand for more personal reforms,

freedom and democracy. The current system has taken on more the

characteristics of fascism (marriage of state and capitalism)

then it is the old communist model. But growth and those who

benefit from the growth has been very uneven. The main benefactors

have been the coastal provinces and urban populations. China

has seen spectacular urban growth over the past decade but the

population is still largely rural. And it is the rural population

that still makes up about 60% of the population that has not

as yet benefited from the growth. The result has been that unemployment

remains quite high particularly in the rural inland provinces

and there remains from the old days numerous inefficient state

industries.

Still as The Economist points out the growth is starting

to make some inroads into the inland provinces (China's growth

spreads inland - The Economist, November 20-26, 2004).

Growing unrest in a number of the inland provinces keeps pressure

on the central government to ensure that economic growth becomes

more evenly divided. We are reminded that Chinese revolutions

(Communist, Boxer) were largely economic in nature due to huge

inequality.

But one thing that has been amazing with the incredible Chinese

growth of the past quarter century is that no major economic

slowdown has occurred. The longer it goes on of course the higher

the risk. We are all reminded that over that same quarter century

of spectacular Chinese growth we have had the Japanese property

and stock market bust (1990-1995), the Asian financial crisis

(1997-1998), and the Internet/Tech bust (2000-2002). So to say

it can not happen is pure wishful thinking.

Since 2001 the Chinese have embarked on a huge spate of construction

projects (including the 2008 Olympics) many of them quite speculative,

financed by money from the Chinese banks where risk assessment

seems to be merely a word in the dictionary. Chinese banks, according

to The Economist, are just conduits to throw money

into government projects and state-owned companies, with little

regard for risk or profits. According to a recent article in

Asia Times (Crash landing coming for China - Jack Crooks, November

12, 2004) the Chinese banking system is virtually insolvent.

At the end of 2003 outstanding loans to GDP was 145%, the highest

ratio in the world. Bad debts at 40% are also the highest in

the world. Crooks describes Chinese bankers, particularly at

local branches, as being unable to tell a good loan from a bad

loan. Pay is dependent on asset growth not whether you make a

profit or not.

This speculative bubble is an accident waiting to happen and

belatedly the Chinese have begun to realize that something has

to be done about it. Ergo the recent increase in interest rates

for the first time in almost a decade and a tightening of administrative

controls. It may be that all of this is too little too late and

an economy that is becoming an accident in waiting may hasten

its way there. China's economy is very dependent upon increasing

amounts of capital to finance the manufacturing, construction

and infrastructure and without this feed the economy will stall.

The service sector is the smallest of any major economy and consumption

is also the lowest of any major economy. Household debt has grown

very rapidly in the coastal provinces but remains very low in

the inland provinces.

China, like Japan before it, has become a major exporting country.

And its major exporting partner has been the United States. It

is a very circular relationship. Again as Crooks drew so neatly

in his November 12 article China as global manufacturer ships

its low priced goods for the US consumer and the US Dollars that

come back to China makes them then a capital supplier wherein

they help finance the huge and growing US deficits in trade and

budget by buying US Treasuries thus subsidizing the US consumer

by allowing the Fed to maintain low interest rates. Growing consumer

demand then fuels the final bit of the circle by spurring further

investment in China.

On paper it looks great. Trouble is that is has also fueled the

debt bubble in the US and spurred the investment bubble in China.

China is financing the debt bubble (along with Japan who together

make up the primary purchasers of US debt) while the reinvestment

back through the shaky Chinese banking system that knows no bounds

in what constitutes a solid investment is when you look at it

closer two bubbles that are accidents waiting to happen. The

Chinese have fixed the Yuan to the US Dollar. So the Chinese

have not suffered the deterioration in their US$ reserve and

investment portfolios the way the Europeans, Japanese and even

Canada have. But pressure is mounting on the Chinese from the

US to allow their currency to revalue higher against the US$.

The Chinese are resisting and if they do it, and they probably

will, they will do it in their own good time. The hiking of rates

and tightening of administrative controls are probably a first

step. The second step may well be to widen the trading band for

the Yuan from the current miniscule 0.3% to a 3-5% range (Asia

Times - China readies to pull the peg - November 20, 2004).

Everyone is caught in a catch 22 with the falling US$. A falling

US$ makes the exporting countries currencies more expensive thereby

putting pressure on their exports and then they in turn want

to stem that flow by buying more US Treasuries to continue to

finance the US debt bubble. As the US$ goes down the value of

their US debt holdings falls also increasing pressure on them

to dump them but that in turn will just mean that the US$ falls

even faster. Japan, according to recent statistics has slowed

their purchases of US debt but they are still the largest purchaser.

China is trying to diversify away from US debt by converting

into Yuan and or looking for purchases in other currencies or

investments in other countries. China also wants to increase

its official gold holdings which would is as well another way

of diversifying its reserves. In some ways a stronger Chinese

currency would be positive for them as it reduces the cost of

the commodities that they use. Remember with a fixed Yuan to

the US$ the price of oil and an whole host of other commodities

is rising as well. But in the other catch 22 if the Chinese economy

was to slow and the demand for these commodities fell then there

could be a commodity price crash as well. How to lower the US$

and raise the value of the Yuan without causing a global economic

crash? That is the question. And may we add that in the case

of the US, no one ever devalued their way to prosperity.

And as if that isn't enough China with its huge growth has now

become the world's second largest user of oil and the demand

should just keep growing as more and more people buy cars as

a result of growing incomes. That makes oil a strategic commodity

for China and they are making it clear it is. With the US also

long declaring that oil is a strategic commodity and the fact

that two thirds of the world's oil reserves lie in the dangerous

mid-East another economic clash could be lying in the wings.

Recently China secured a huge $70 to $100 billion deal with Iran

for oil. Given all the rhetoric and saber rattling between Iran

and the US over Iran's nuclear weapon ambitions, any solution

to that just got more complicated. The military solution to the

problem may have hit a brick wall. Ditto for a military solution

to the nuclear weapon ambitions of North Korea, where that is

just too close to China for comfort.

China is at a cross roads. And if China is at a cross roads so

to is the rest of the world because if China's attempts to try

and bring itself down with a gentle landing and it fails turning

into a crash landing then it will impact the rest of the world

as well. But the Chinese economy is young and with 1.2 billion

people the growth possibilities are huge. So even if China were

to have a crash landing it would be cleansing and they should

emerge from it stronger. But we are not so sure how a debt laden

country such as the US will emerge from a Chinese crash landing.

That could be a completely different story.

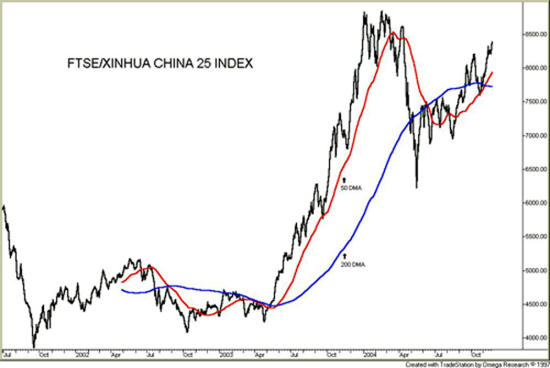

Spectacular rise in 2003

was met with a very sharp correction into mid-2004. The current

up-wave remains short of the highs. A failure to make new highs

would suggest that the collapse in 2004 was corrective in nature

and this is the B wave up. A C wave could take us to new lows

or the correction could be more complex in nature. Given that

China has raised interest rates and that a slowdown in their

economy has not as yet happened despite the enthusiasm for China

we would be cautious on purchases here. Any return back under

the 200-day moving average should put everyone on the sidelines.

Given the speculative investment fervor in China today and the

probability of an upward revaluation of the Yuan the Chinese

stock market could remain weak for some time.

David Chapman

Email: david@davidchapman.com

Note: Charts created using Omega TradeStation or SuperCharts.

Chart data supplied by Dial Data.

David

Chapman is a director of the Millennium Bullion Fund. David

Chapman is a director of the Millennium Bullion Fund.

The opinions,

estimates and projections stated are those of David Chapman as

of the date hereof and are subject to change without notice.

David Chapman, as a registered representative of Union Securities

Ltd. makes every effort to ensure that the contents have been

compiled or derived from sources believed reliable and contain

information and opinions, which are accurate and complete. Neither

David Chapman nor Union Securities Ltd. take responsibility for

errors or omissions which may be contained therein, nor accept

responsibility for losses arising from any use or reliance on

this report or its contents. Neither the information nor any

opinion expressed constitutes a solicitation for the sale or

purchase of securities. Union Securities Ltd. may act as a financial

advisor and/or underwriter for certain of the corporations mentioned

and may receive remuneration from them. David Chapman and Union

Securities Ltd. and its respective officers or directors may

acquire from time to time the securities mentioned herein as

principal or agent. Union Securities Ltd. is an independent investment

dealer and is a member of the Toronto Stock Exchange, the Canadian

Venture Exchange, the Investment Dealers Association and the

Canadian Investor Protection Fund.

________________

321gold Inc Miami USA

|