Friday the 13th Friday the 13th

David Chapman

It's Friday the 13th and most people will immediately conjure

up images of Jason in his hockey mask slicing and dicing horny

teenagers at Camp Crystal Lake. Of course the myth of Friday

the 13th is steeped in superstition as a day of bad luck. There

are even those who have a fear of Friday the 13th called paraskavedekatriaphobia.

It is itself a form of triskaidekaphobia or a fear of the number

13. There are numerous origins of the superstition from the fact

that there were 13 people at the last supper of Jesus Christ

who was in turn crucified on Good Friday to old Norse myths and

differences in the a lunisolar calendar that has 13 months to

the Gregorian and Islamic calendars that have 12 months.

Oddly the 13th

is more likely to be a Friday than any other day of the week

but that has not stopped Hollywood, those with phobias, strange

evidence that suggests that Friday the 13th is actually unlucky

for some and that businesses particularly airlines lose millions

of dollars in business because people will not travel or go to

work on the day. So in keeping with the spirit of the day we

thought it would be ideal to lay out some of the scary things

that are occurring in both the financial and political world

that could derail investors in the coming months and even now.

Of course if

you listen almost exclusively to Alan Greenspan and Kudlow and

Cramer of CNBC fame you might be excused for thinking that all

was normal and that despite short term problems the market will

right itself and inevitably move higher. Of course what all of

this is premised on is the undying faith many have in Alan Greenspan

that he will consistently and persistently maintain system liquidity

and provide the conditions to allow us to get through these problems.

So far it has

worked, witness the huge stock market rally in the markets in

2003 and the improvement in the economic numbers and despite

some sluggishness even some growth in employment. Despite the

weakness seen in the markets in 2004 and recent sluggishness

in the economy, the byword is to maintain a good mood especially

leading into the November elections and that we are continuing

a robust recovery. Further there is no bubble in the housing

market, the debt is manageable and interest rates will rise but

very slowly. Many others and we of course believe that this is

merely wishful thinking and the economy and the stock market

are so full of cracks and dangers that hiding the truth is just

irresponsible.

Of course for the authorities to tell the truth we would have

a financial panic of unprecedented scope. Wisely, we guess, they

leave the doom saying to pundits such as numerous others and

me to point out the cracks in the system and hope of course that

nothing untoward actually happens leaving our credibility in

shreds. We find that patronizing as it ignores the fact that

numerous analysts actually come from many years of experience

working for the very financial institutions, which we now criticize.

But that being

said one cannot ignore the power of the Fed and its abilities

to provide the liquidity and monetary conditions for the market

to survive. They cannot prevent a market collapse per se nor

can they save everyone from bankruptcy or prevent a sharp drop

in housing prices but they can contain it if it were to happen.

Even if we do not see conditions on the scale of the 1930's happening,

there is always the nagging feeling that it could under the worst

of conditions.

The stock market

rally of 2003 was fuelled primarily by huge monetary growth with

M3 growing almost consistently in the 10% range especially in

the first half of 2003. After a sharp slow down in monetary growth

late last year there was a further burst of monetary growth in

the first half of 2004. Thus far the rapid monetary growth coupled

with the ongoing low interest rate environment and no real shock

to the system has allowed the economy to show signs of growth,

provided a better business environment for profits and has helped

maintain employment levels with some employment growth. But in

terms of past recoveries it has been very anaemic.

But with the

stock markets falling now to new lows for the years and highs

almost consistently being lower than the previous high, as we

move into the traditional seasonal weak period of the year there

is some concern that we may have already seen the highs for the

year. Not only may we have seen the highs for the year but also

we may be headed significantly lower than most pundits are currently

expecting. The following is our economic reasons as to why the

cracks in the system may widen in the coming months. We follow

it with political risk.

Oil prices

have shot to the highest levels ever crossing over $46 per barrel.

While in inflation adjusted terms we are no where near the levels

we experienced at the time of the Iranian Revolution in 1979/1980

rising oil prices act like a tax on the economy. Rising oil prices

are an inflationary shock to the economy and they are an inflationary

shock to financial asset bubbles. Financial asset bubbles are

all built on the premise of ongoing low price inflation and a

low interest rate environment. The US imports over 50% of its

oil. Oil imports have hit record levels.

Interest rates

are starting to rise. While thus far the Fed has only hiked by

50 basis points it may not take a big rise to destabilize the

market. The housing market has been fuelled by low interest rates

and the big financial institutions and hedge funds use the low

cost of short-term money (controlled by the Fed) to speculate

in numerous financial instruments at a spread (carry trade).

Rising short term rates and as well rising long term rates quell

the housing market, make mortgages more expensive and spell the

beginning of the end of the carry trade.

The housing

markets have been in a bubble now for the past two years despite

claims otherwise that the market is not in a bubble. This is

simply nonsense as in some areas of the US and elsewhere housing

and condo prices have shot up 50% or more over the past couple

of years. This is unsustainable and with interest rates rising

the market is vulnerable. Worse, numerous mortgages over the

past few years have been made on some of the worst terms we have

ever heard. Loans up to 125% of value have occurred and 100%

to 110% mortgages are not unusual. When the market crashes, as

it will, people will walk away from these mortgages leaving the

financial institutions with an oversupply. A Morgan Stanley report

has noted that they believe that 25% of the global economy is

infected by speculative exuberance in the housing market including

Australia, Britain, China, South Korea, Spain, the Netherlands,

and South Africa. Another 40% of the world economy there is a

threat of speculative bubbles in Canada, the USA, France, Sweden,

Italy, Hong Kong, Thailand, Russia and Argentina (Executive Intelligence

Review, August 2004).

The US triple

deficits of trade, budget and current account are simply unsustainable.

The trade deficit announced today was a record $55.8 billion

and is currently on target for a yearly trade deficit of about

$575 billion. Exports fell and imports rose primarily due to

increased oil imports and higher oil prices. Predictably the

US$ fell sharply and gold rose. The budget deficit also is on

projection for $400 billion. Taken together the US is adding

upwards of a trillion dollars a year in new debt. Much of this

debt is dependent on foreigners to finance it primarily Japan

and China. China, Japan and Asia in general are the major economic

competitors of the US. With a growing dependence on financing

coming from foreigners there is the risk that foreigners could

pull back or even sell their holdings if they begin losing substantially

on their holdings because of the combined rising interest rates

and a falling US$.

Hedge Funds

and the financial institutions of investment dealers and banks

increasing investments in carry trades and highly leveraged positions

and massive derivative positions leaves them more vulnerable

to shocks including rising interest rates, rising oil prices,

and the threat of terrorist attacks. It has already been determined

that hedge funds in particular were hit hard in the first half

of 2004 with the sharp drop in the bond market. They too have

been guilty of believing that the Fed will ride to the rescue

and maintain an environment of low interest rates and endless

liquidity in order to continue the leverage games they have been

playing. It would be one thing that if it was just the hedge

funds but the banks and the investment dealers are heavily into

the same leveraged positions themselves. Could the Fed handle

a financial meltdown across the entire banking and financial

system?

The consumer

is, as they say, up to his eyeballs in debt. Never in history

has the economy been as leveraged as it is today. It is estimated

that in barely five years the consumer has gone from a 93% debt

to income ratio to one of 115% and climbing. Most of it is mortgage

debt but consumer credit card debt is also at unprecedented levels.

Personal bankruptcies, defaults and mortgage foreclosures continue

at record levels despite the supposed buoyant economy. The consumer

is 75% of the economy and if the consumer is tapped out on debt

and can no longer buy the economy will falter. Retail sales are

showing some signs of faltering as the consumer is forced to

spend more on basics such as food and energy. While oil prices

may not yet have reached that point where it has a serious negative

impact we are rapidly approaching that point. If the cracks in the financial system

are vulnerable it is in the political sphere where the shock

may come that causes a financial panic.

Oil prices

are rising because of vulnerabilities of terrorist and insurgent

attacks on pipelines in Iraq and Saudi Arabia. Two thirds of

the world's oil supply is in the very vulnerable Mid-East and

there have been attacks in Saudi Arabia although not on the oil

facilities, attacks in Iraq and Iran also are potential flash

points. Oil prices are also being impacted by the ongoing bankruptcy

of Yukos in Russia (who supplies 2% of the world's oil) and in

Venezuela where a recall vote this weekend may leave Chavez in

power. There have been two previous attempts at a coup in Venezuela

but Chavez has managed to stay in power. According to polls the

recall vote will fail as Chavez remains very popular with the

electorate. The US has been consistently linked to coup attempts.

Iraq remains

on a knife-edge. The insurgency of the militia Muqtada Sadr has

the potential to turn into a full-scale civil war. No matter

what one thinks of Sadr he is a powerful Iraqi cleric with a

substantial following and they are fighting the US foreign occupiers.

As with all foreign occupiers throughout history they fail to

understand the people and their own history. There is a high

risk of serious damage to the Islamic holy site of the Imam Ali

Mosque as well as to one of the world's largest cemeteries of

Wadi Salam. This would inflame Muslims globally as it would be

seen as holy war. Imagine a comparable attack on the Vatican

or Arlington Cemetery. Turning Sadr into a martyr would accomplish

nothing. It was his father who fought the British during the

British occupation following WW1. Some states are threatening

to secede from Iraq, which in turn would trigger succession of

the Sunni Kurds, which in turn could trigger a war with Turkey.

The hand of Iran is increasingly been seen in Iraq supporting

the 60% Shia population. The government of Ayad Allawi is seen

as strictly an American puppet especially given his ties to the

CIA and eyewitness reports of Allawi personally executing prisoners.

Iraq, compared to the relative stability of Saddam, is in chaos

and threatens to get worse. Even the trial of Saddam is in doubt

as the chief prosecutor is being charged with murder. Mistrial

anyone?

There is a

risk of a clash with Iran. Rhetoric has been rising in the US

over the past several weeks concerning Iran's nuclear program.

That the credibility of the US with regard to WMD is completely

shot especially after Iraq does not seem to faze them as similar

arguments are being made as to why Iran is a threat. As well

there is some evidence that Iran is supplying Iraqi insurgents.

Iran is part of Bush's Axis of Evil along with Iraq and North

Korea. Further Russia is cementing ties with Iran and is providing

them substantial assistance. Russia itself is planning a huge

increase in military expenditures in the coming year. Russia,

unlike Iran and Iraq, does have WMD and can deliver them in 45

minutes. The Russians have become increasingly concerned about

the growing US hegemony in Central Asia and the Middle East in

control of the oil supply and the proximity of US military bases

to Russia.

No matter what

one thinks of the Orange alerts there is a risk of a terrorist

attack. Trouble is being warned of its coming leaves it open

to manipulation and far more questions then there are answers.

The conclusion that it is Al Qaeda almost seems too simplistic

given the ongoing warnings. One feels as if we are being set

up to fail. Amongst the warnings are sources that say it is from

Osama Bin Laden himself. There has been considerable capital

spent on trying to prepare the American public that a terrorist

attack not only could happen but that it will happen. Plans have

been set in place to cancel the elections including what legal

steps are necessary. The thought that the elections could be

cancelled is being met more with a yawn then with outrage as

the major media play their role of asking the question in a matter

of fact manner. A terrorist attack triggering Red Alert could

in effect turn the US into a military dictatorship. This is not

to discount that it can't or won't happen. Indeed we almost seem

to be guaranteed that it will. The bigger question of who could

be behind it will be met with the pat answer of Al Qaeda because

that is the answer we are being prepared with. This isn't to

say it won't be Al Qaeda but that constant warning raises the

question of who benefits and why. But no matter from where the

attack comes from, the stock market would swoon and the financial

system would be destabilized in a manner worse then it was at

the time of 9/11.

An over leveraged

economy, rampant speculation, the threat of terrorist attacks,

sharply rising oil prices suggests one should just hunker down

and stay out of sight. Indeed a pundit even suggested maybe I

should just slit my wrists and go. Of course that would be foolishness

in the extreme. Not that we are immune here in Canada but whatever

the worst case scenario envisaged is undoubtedly no where near

as bad as say those directly impacted in a terrorist attack or

the people of Iraq caught in the crossfire.

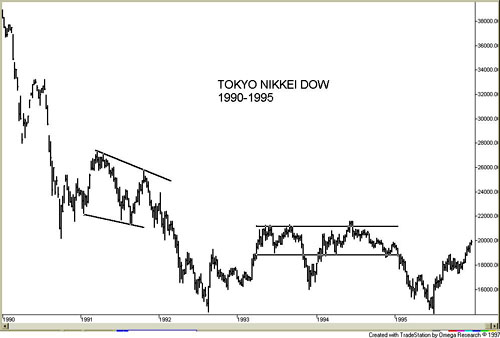

We are showing

two charts [chart

1 - chart 2] both of which we mentioned

on a recent ROBTV appearance. The first is the chart of the Tokyo

Nikkei Dow 1990-1995. We bring your attention to the consolidation

patterns seen in 1991/1992 and again in 1993/1994. These were

drifting patterns after rallies that followed sharp drops in

the market. The rallies that followed the sharp drops looked

impressive but ultimately they failed and the market fell to

new lows.

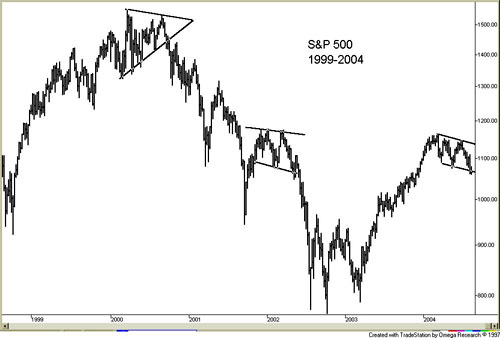

Similarly the

markets of the early millennium demonstrate comparable patterns.

We have always been struck in the similarity between the collapse

of the Tokyo Nikkei Dow of the 1990's and the current market.

The giant topping pattern of the summer of 2000 played out as

a drifting triangle until it collapsed. Similarly the drifting

pattern of late 2001/2002 was a drifting pattern that collapsed

into the financial crash of 2002.

Once again

we are seeing this listless drifting pattern in 2004. Many believe

that the rally of 2003 was a powerful first leg rally of a new

bull market. It is not. It was a corrective rally fuelled by

the easy monetary policies of the Federal Reserve. It saw little

or no corrections. Now we are drifting aimlessly but with a series

of lower highs and lower lows. These patterns that have characteristics

of descending triangles ultimately collapse to test the previous

lows and probably see new lows.

We are now

coming perilously close to breaking the downside of the pattern.

If we do we will collapse first to the S&P 500 960 area then

most likely to the lows of 2002 and possibly even lower. It is

time to batten down the hatches if you have not already done

so. The oils and the golds could or should thrive in this environment.

But others will suffer. It is now Friday the 13th and the real

scary part may be about to begin. Haaa Haaa Haaa Haaa Chhhh Chhhh

Chhhh Chhhh!!! (Theme from Friday the 13th The Movie).

August 13,

2004

David Chapman

Email: david@davidchapman.com

David

Chapman is a director of the Millennium Bullion Fund. David

Chapman is a director of the Millennium Bullion Fund.

The opinions,

estimates and projections stated are those of David Chapman as

of the date hereof and are subject to change without notice.

David Chapman, as a registered representative of Union Securities

Ltd. makes every effort to ensure that the contents have been

compiled or derived from sources believed reliable and contain

information and opinions, which are accurate and complete. Neither

David Chapman nor Union Securities Ltd. take responsibility for

errors or omissions which may be contained therein, nor accept

responsibility for losses arising from any use or reliance on

this report or its contents. Neither the information nor any

opinion expressed constitutes a solicitation for the sale or

purchase of securities. Union Securities Ltd. may act as a financial

advisor and/or underwriter for certain of the corporations mentioned

and may receive remuneration from them. David Chapman and Union

Securities Ltd. and its respective officers or directors may

acquire from time to time the securities mentioned herein as

principal or agent. Union Securities Ltd. is an independent investment

dealer and is a member of the Toronto Stock Exchange, the Canadian

Venture Exchange, the Investment Dealers Association and the

Canadian Investor Protection Fund.

________________

321gold Inc Miami USA

|

{kind=link}

{kind=link}