|

|||

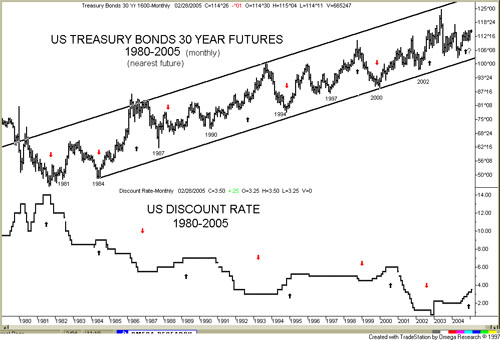

Bond debacle coming?David Chapman Our monthly chart of long term US Treasuries and the Fed Discount Rate show this relationship. While there have been periods of where US bond prices fell sharply on only a small hike in rates and there have been periods of some ambiguity we can not recall a period such as this one where we have seen both long bond prices rise along with a hike in the discount rate. So what's wrong?

One argument being put forward is that since the US is no longer issuing long-term bonds that there is a scarcity of product. But this doesn't wash as the active 10-year bond has gone up in price as well. Today 10-year bond yields have fallen to 4.16% and the spread between short rates has narrowed considerably. With a year over year rate of inflation of 3.3% the spread between the inflation rate and 10 year yields is less than 1% while the spread to short rates is still negative although considerably less negative then it has been. For long bonds though the narrow spread is puzzling as historically there is at least a 2% or more spread between long rates and the rate of inflation. The Economist recently offered some reasons as to why bond prices may be rising. First it may be that Pension and other large funds are shifting more cash into bonds expecting some regulatory changes that might favour the strategy. Second foreigners continue to buy US long bonds thus artificially keeping interest rates lower than they might otherwise be. This is being done to prevent their own currencies from rising too fast against the US Dollar. A third reasoning is that bond investors have a high faith in the ability of the Fed to fight inflation. Odd considering that inflation has been rising of late not falling and it assumes that no one is overly concerned about the huge deficits of budget and trade. A fourth reasoning (and the gloomiest) is that despite the upbeat economy, bond investors see nothing but storm clouds on the horizon and that the debt-laden US consumer is an accident waiting to happen. This is odd as well because if a credit crunch is expected usually bond prices rise in anticipation. Finally investors may have just mis-priced bonds and are too complacent about the possibilities of the budget and trade deficits lessening and about inflation. Bill Gross of PIMCO, the world's largest bond fund, has lessened his investments in US bonds for some time and has sought what he believes the relative safety of foreign bonds particularly in Europe on a fully hedged basis. Mr. Gross believes that as we noted above that foreigners have kept US bonds artificially low buying to protect their currencies and 10 year yields should be at minimum 5% or higher. Of course that would have negative ramifications for the US economy as even a small increase in bond yields could choke off the mortgage market and leave many consumers in dire consequences. Clearly that is not something that is desired by the monetary authorities as that would also choke off the consumer economy forcing the US (and others) into a recession. The US remains the driver of the world economy even as the US consumer continues to spend in excess of his income. Irrespective that is something that cannot go on forever even as some analysts continue to be dazzled by the ability of the US consumer. The other mystery with US bond yields is the fact that the yields have stayed down in the face of the weak US Dollar. We believe that a lot of that can be explained by the huge presence of foreign buying of US bonds even as the US Dollar declined. Certainly the experience in the 1970's when the US Dollar was in major decline the US bond market saw constantly rising yields. Today even as the US Dollar has been falling since 2001 the US bond market has been generally rising in price (falling in yield). There are hints, however, that those days may soon be over and here is the risk for the US bond market. As the US Dollar falls assets denominated in US Dollars also fall in value for foreigners. Despite the fact that foreigners have poured billions into the US bond market in the past few years especially from Japan and China and to a lesser extent Europe some such as the Europeans are becoming less concerned about their rising currency and that it would cause them economic problems. As well China (and other Asian countries but not yet Japan) are seeking ways to lessen their dependency on the US Dollar for trade. This suggests a further shift away from US Dollars (and US Dollar denominated securities) into other currencies. Trade in between Asian economies and Europe has been rising faster than trade with the US so there is incentive to lessen dependency on the US Dollar. Recently some Chinese officials have been making statements that "the US Dollar is no longer, in (their) opinion is no longer, (seen) as a stable currency and devaluating all the time, and that's putting troubles all the time" (Chinese Economist Fan Gang). The US has wanted the Chinese to increase the value of the Yuan for some time. If the Chinese were to grant the US its wish then they would not need the huge hoard of US Treasuries they presently hold. Massive treasury selling could follow. As well just even a perceptible shift out of US Dollars denominated assets and into other currencies would have a negative impact on the US bond market. Our understanding though is that the Japanese continue to pour funds into the US market. In the past year alone, while we have no breakdown of who is buying, marketable securities held in custody by the Fed by foreigners have increased by some $229 billion to over $1.3 trillion. And the rise to $1.3 trillion has taken place largely in the past two years as the US Dollar fell. This has clearly gone a long way to help the US Treasury market even as the US Dollar has declined. This has also occurred even as the Japanese bond market itself is a bubble accident waiting to happen as the Bank of Japan has kept rates artificially low to help the Japanese economy. Meanwhile debt to GDP has soared to 150% and while the Japanese banking system is cleaning up their balance sheets there is more to be done. We are also reminded that both the Japanese and Chinese banking systems remain very fragile and many of their financial institutions are technically bankrupt. Chinese financial institutions in particular have created an investment bubble lending with little regard to credit quality. Indeed for the most part they are guilty of over lending and a lot of these funds have gone into speculative activity. These are bubble accidents waiting to happen. So with a bubble in both China and Japan and a bubble in bond assets in the US as well the only question is what will be the trigger for an accident. We don't have the answer for that. All we know is that the risks are very high and we suspect it will be triggered by some sort of credit crunch and a major default. Recall that the crisis of 1998 got underway with a Russian default and that almost collapsed the financial system. Today the Fed has considerable less room to manoeuvre as they have kept short rates so low for so long that even dropping rates to zero may not have the desired effect of saving the system. If fundamentals are lining up against bonds then cycles are also possible falling into place as well. Bonds demonstrate a number of longer-term cycles. Generally bonds have followed cycles of roughly three years with distinct lows seen in 1981, 1984, 1987, 1990, 1994, 1997 and 2000. Since 2000 it has been somewhat trickier. Ray Merriman of MMA Cycles also describes a 6.125 year cycle that normally divides into two 36 month cycles but could divide into three 25 month cycles. If that were correct then we had a low in March 2002 (26 months after the 2000 low) and another one in June 2004 (27 months after the March 2002 low). That pegs the next low and the trough of a possible 6.125 year cycle to occur somewhere between March 2005 and February 2007 with a mean around February 2006 (Merriman). Note that 6.125-year cycle lows occurred in 1981, 1987, 1994 and 2000. After that low is made we would expect bond prices to rally once again. If as we expect that it could be because of severe recessionary conditions into 2008/2009. The question is how low could we go as even our long-term chart shows that there is a fairly good up channel from the 1981 lows. The bottom of that channel is currently near 102^24 some $12 below current levels. US Treasury bonds have been making a series of lower highs and lower lows so that too suggests that bonds could be topping out here and due for a further drop to new lows. The drop to a 103 level or so doesn't seem like much but it would raise long yields north of 5% and that would trigger all sorts of problems. Fundamentally, cyclically and technically we do appear to on the cusp of bond debacle. So what of the US Dollar if we were to have a bond debacle? Oddly the US Dollar may just waffle through the period before beginning a bigger downdraft to targets of 60 later in the decade. Certainly looking at a longer-term chart of the US Dollar it is suggesting that a possible descending wedge pattern may be unfolding. The recent decline in the US Dollar took us back to the lows of both 1991 and 1995. Unfilled and not yet tested are the lows of 1992 near 78.50. So we are in an area of considerable support that could give rise to a series of dollar falls and rallies over the next year within the context of a possible descending wedge. Currently we are near the top of the channel and the US Dollar's recent rally is running out of steam. Any country that runs trillion dollar deficits can not expect to have a strong currency and this will continue to weigh on the market as expectations are that little will be done to improve it. Even a modest decline to the bottom of the channel just below 80 could spark a rally in Gold to the targets of $480 - $550. That area would signal another temporary top in Gold and a sharp decline we suspect would get underway from those levels. The last 18.5 monthly low for Gold was in May 2004 targeting the next one for sometime between August 2005 and March 2006. This should also coincide with the trough of the 4.25-year cycle.

David Chapman |