Casey Files Casey Files

Recession, GDP and Inflation:

Conventional Wisdom or Data

Bud Conrad,

Casey

Research

Mar 12, 2008

That we are moving into

- or already are in - a recession is practically a given. But

what will it be: inflationary or deflationary? Casey Research's

Chief Economist Bud Conrad weighs in with his findings...

The debate is coming to a head

over whether we will see inflation or deflation. Will the coming

recession bring deflation from the housing-related credit crisis

in which many forms of debt are disappearing in default; or will

the lack of confidence in the dollar and the government stimulus

bring us inflation?

The consensus of economic opinion

is that the recession that is just starting could lower demand

and thus bring a lowering of prices. "It's just like Japan!

Credit collapse is like the Depression! Those were deflationary!"

say many respected practitioners of the dismal science.

Some deflation! Crude over

$100; wheat hitting $25 a bushel; gold at $970. What is going

on? Yes, housing is dropping 7% in price, and the stock market

is back and forth going nowhere. So which is it? Inflation or

deflation?

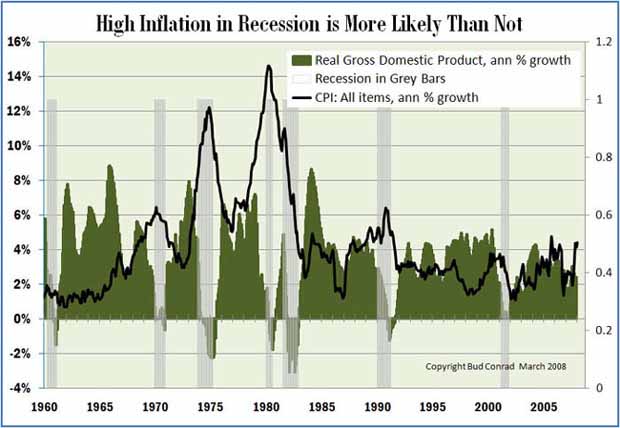

I always say "Let's look

at the data." I have been looking at previous recessions

to see what happened to gold and gold shares in the last two

issues of BIG GOLD. Here I just look at the Real Gross Domestic

Product, which is the biggest measure of how well our economy

is producing wealth, to compare to the inflation level. I use

the most quoted government inflation number, the Consumer Price

Index (CPI).

During periods of recession,

the GDP was falling - no surprise there, as that is sort of the

definition of recession. But look at the inflation. It wasn't

falling during recession, it was higher. In two of the seven

recessions someone might argue whether or not it was higher,

but it wasn't noticeably lower. It is amazing how convincing

a look at history can be.

We have been describing the

"Rock and a Hard Place" problem for the Fed, in that

if they lower interest rates, the dollar collapses and eventually

inflation appears; or if they defend the dollar with higher rates,

then the economy collapses. This analysis shows just how serious

the bind is. Historically, when inflation jumped, mostly spurred

by the big oil shocks, we saw both big recessions as well. At

the time, it was acknowledged that the commodity shock caused

the recessions by driving inflation and interest rates higher.

So the stagflation is really not so

new or rare an occurrence. I have been predicting this for a

long time. We are now there. Bernanke's performance has been

lackluster and not inspiring confidence, to say the least. He

might as well have said "Let the dollar be dammed, full

speed ahead with the helicopters." Instead of a determined,

cigar-smoking disciplinarian like Volcker, he just looks weak. So the stagflation is really not so

new or rare an occurrence. I have been predicting this for a

long time. We are now there. Bernanke's performance has been

lackluster and not inspiring confidence, to say the least. He

might as well have said "Let the dollar be dammed, full

speed ahead with the helicopters." Instead of a determined,

cigar-smoking disciplinarian like Volcker, he just looks weak.

To some extent history has

already predicted the result, so it is really beyond one man's

attempt to push a lever behind the curtain. Really, there's not

that much for him to do but watch the dollar collapse and the

U.S. economy to slow. Stagflation.

Bud Conrad is Casey Research's

chief economist and a regular contributor to BIG

GOLD, a monthly advisory for the more conservative resource

investor. BIG GOLD focuses on large-cap gold producers and near-producers,

gold mutual funds, ETFs and much more.

With gold now up over $970

an ounce, the investing masses will soon catch up to its timeless

value as an inflationary hedge. When that happens, BIG

GOLD subscribers will already be well positioned to benefit

from the incoming tide. Sign up for a risk-free trial subscription

with 100% money-back guarantee today and take a full 3 months

to decide whether BIG GOLD is for you click here to learn more.

###

Doug Casey

Casey Archives

321gold Ltd

|