|

|||

|

Good Reasons To Be BearishRick Ackerman

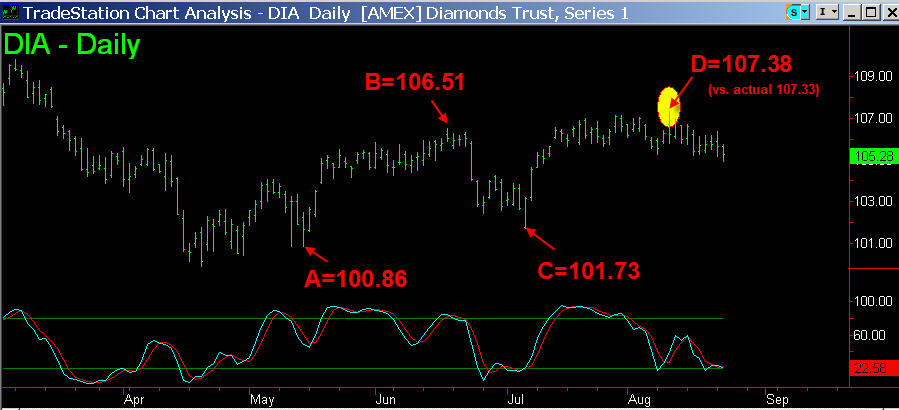

The chart below suggests that although we missed a great opportunity to short the Diamonds a couple of weeks ago, we're likely to get another chance, and probably soon. Note that the most recent rally produced a price peak of 107.33 on August 10. That high came within just 0.05 points of an important hidden pivot at 107.38, strongly implying that the three-month bull cycle that produced it is completely spent. For this reason, we should expect the bear to dominate in the weeks ahead and perhaps longer.

I'm not sure why I didn't notice the telltale symmetry of this ABCD pattern earlier, but it is more compelling than any I can discern in other vehicles we trade regularly, including the S&P futures, the mini-Nasdaq and the mini-Russell. Like many of you, my eagerness to short this market has been waxing for months. But because it felt like the averages wanted to go higher, we've kept our bets small. Now, though, it's time to get more aggressive, and I've detailed a low-risk strategy for doing so in today's Touts. Meanwhile, if you're looking for more reasons to hate stocks at these levels, the following piece, from Gary North's Reality Check, is powerfully persuasive. North's daily e-mail service is one of the best freebie's on the Web, so if you don't subscribe to it already I'd urge you to give it a try by clicking here. Here's North, explaining in his most recent dispatch why many consumers and homeowners in the U.S. are headed for BIG trouble in the not-too-distant future: Credit Squeeze Ahead If you are looking at your financial position, you should consider your assets in relation to your liabilities. What you should do, a bank by law must do. Banks have assets. A huge asset on the books of the biggest American banks is credit card debt. That money is owed by borrowers. Interest rates paid on these cards is far higher than rates obtainable by banks from any other class of loans. The written credit card debt contracts are also beneficial to banks. Low card rates can be hiked without warning overnight to 20% or even 30% per annum if a borrower misses a payment to his mortgage company or any other creditor. This missed-payment information goes from the third-party creditor to a credit rating agency, and from there to the bank. Credit card debtors have agreed to contracts that pass most of the power to the lending agencies, which are banks. All this sounds like good news for the banking industry. But then the banking industry got into the game of politics. (Actually, I can think of few industries that got into politics earlier: the fifteenth century at the latest.) The banks began to pressure Congress last year to pass legislation to toughen the bankruptcy law. Congress complied with bank lobbying early this year, and President Bush signed this legislation into law, just as he has done with every proposed law that Congress has put on his desk since January, 2001. Shrinking Assets Few people understand that the minimum monthly payment required by banks kept the borrower in debt for over two decades. Now, that's a loan that pays and pays and pays! The borrowers, not understanding compound interest and paying attention only to the monthly payment's effect on their budgets, willingly locked themselves into a long-term debt contract. This was a bonanza for the banks, which was why American banks since 1965 have dramatically increased the assets on their books attributable to credit card loans. On October 17, the new bankruptcy law will go into effect. That is the day that the banks will see their cash cow wander off into the field toward the butcher's. The new law cuts those juicy 20-year loans to 10 years. Monthly payments will jump accordingly. Also, the new law requires borrowers to repay these loans even after bankruptcy. The banks asked Congress to intervene and make things less risky for the banks. Congress did as it was told, but there will be a cost: the doubling of the minimum-balance monthly payoff. That will hit borrowers like any unexpected bill does. They will have to adjust their monthly budgets. This will come at a time when gasoline price increases are already forcing major budget readjustments. So, it will become more difficult for banks to increase the number of takers when they advertise their "low, low, low" rates. An asset that had been ideally suited for growth -- a long-term loan based on low monthly payback -- will now find new market resistance. Here is the assessment of business journalist Dana Blankenhorn, who has been in the field for 25 years. Faster write-downs of credits by borrowers means fewer assets for credit card banks. Forcing borrowers to pay back their loans, even after bankruptcy, means those assets can't be written-off, and those bankrupt borrowers can't be extended new credit. It's a squeeze on bank assets, from both sides of the ledger. So two things happen, even in the best of all possible worlds. Assets decline, while new assets become harder to generate. For the industry that, more than any other, is an industry of contracts -- banking -- a change in the terms of contracts can have repercussions. The bankers know what's coming. The average Joe, who is up to his eyeballs in credit card debt -- maxed out -- doesn't see what's coming. He will in November, when he gets his new bill on his credit card statement. It's the law! Millions of people (I have no idea how many, but the number may be in the 10s of millions) are already at their limits, squeaking by and paying the minimum on their credit card balances. To protect themselves, the banks made it the law that rates on balances that fall past-due automatically jump to over 30%. But this is, in fact, no protection at all. The banks' assets are frozen, and while they might be paid back in time, the chances of raising more assets (remember, loans are assets to the banks) declines dramatically once the hammer falls on borrowers. The Mortgage Market New home owners have gotten in late. They are paying up to half of their monthly take-home pay to live in their newly purchased homes. Property taxes have not been hiked. This tax hike is coming. OPEC is also squeezing them. Now comes the new bankruptcy law. People have been encouraged (by subsidies, and the fact that banks can always sell their loans to Fannie Mae and Freddie Mac) to create a mortgage "asset bubble," with interest-only and adjustable-rate loans. People were then encouraged to furnish these palaces through credit cards or second-mortgages. This has happened nationwide, not just in the areas where the supply of new housing has been tight. So let's say you're stretched and October rolls around. The credit card bill jumps. The natural inclination (the one encouraged by banks) is to tap the home equity. But that may already be tapped. With many tapped people forced to put homes on the market (to stave off bankruptcy) a downward spiral begins. Home equity values fall, and with each turn more over-extended homeowners find themselves with negative equity. Home equity loans must be called, mortgage loans start to default, foreclosures add more assets to the pile. (Those who deal in foreclosures are already cheering.) No doubt, this chain of events in the housing market will be described as a side effect of the new bankruptcy law. The biologist Garrett Hardin once wrote that there are no side effects. There are only effects. Those effects that are both unpleasant and unexpected are called side effects. The Federal Reserve will probably continue to announce increases of .25 percentage points at the next three FOMC meetings scheduled for 2005. This will push up short-term rates, which will negatively affect the adjustable rate mortgage market. Blankenhorn's conclusions are what mine were even before I read his article. My advice is to get in the best equity position you can before the hammer falls. Look for stocks in companies that export. Look for hard assets, foreign assets. The natural inclination in this situation will be for the government to print more dollars, but the government too is overextended, thanks to Iraq, pork and tax cuts, so when more dollars are printed the value of each dollar falls. Thus, you don't want to be in dollars. He is speaking of dollars in relation to foreign currencies. But it's better to be in dollars during the early phase of a recession than to be in the stock market. He is predicting a recession. I will be when I see the interest rate on 90-day T-bills above the 10-year T-bond rate. We are approaching this scenario. The NASDAQ Mania, 2000 In February, 2000, I sent out my monthly issue of Remnant Review. I titled it "The Madness of Crowds." I began with this paragraph: The combined market valuation of the proposed Time Warner/AOL conglomerate is expected to be $350 billion. That is more than the market valuation of Spain's stock market, according to Bill Bonner's "Daily Reckoning" (Jan. 14). The company will sell in the range of 200 times profits. I said this was madness. I use AOL as a back-up e-mail service. I pay $5 a month for the service. There are 40 million users. AOL gets newcomers onto the Internet, but once onto the World Wide Web, AOL has no competitive advantage -- and far less tech support -- than a local Internet service provider. AOL has to keep people by means of its non-Web services and features -- suspiciously like the local bulletin boards of the late 1980's and early 1990's. But the power of the Web is so great that it overwhelms anything resembling a bulletin board. The sense of community necessary to sustain 40 million customers' interest is difficult to achieve, precisely because the customer base is so large. Breaking AOL down into sub-communities is the obvious way to go, but AOL has no powerful advantage over Yahoo! or other "Web portals." It has no advantage at all over specific Web sites -- millions of them today -- that offer very tightly focused information and chat forums. I then launched into a discussion of the mania of the NASDAQ, which was selling at a price/earnings ratio of 206. The basis of sustained increases in price is profitability. Without earnings, a stock rises only on expectations of future earnings. But when the entire NASDAQ looks like this, then mania has hit. Where will the earnings come from to validate a 206/1 P/E ratio? They won't. To spend $206 to buy $1 of earnings -- which are not dividends -- is irrational, except on the assumption of the "greater fool" theory. There sits a stodgy U.S. government bond, paying well over $6 per $100. New investors don't consider anything so lackluster. Only in a recession or depression would there be capital gains to bonds through falling interest rates. Who expects a recession or a depression? No one under 50. While the average stock has continued to fall in price in the last two years, the Internet and technology stocks soar to new heights. The discrepancy is becoming more obvious as time goes on. Investors are persuaded that the wave of the future is in Internet stocks. The wave of the future is assumed to be positive. But the discrepancy between the performance of the two worlds tells us that the mania cannot be sustained. When investors at last lose confidence in the ability of their portfolio to perform except on the basis of the "greater fool" theory, they will search for more conventional returns. When they do, a crash in this sector will take place. Reality will intrude. This was obvious to me in February, 2000. In early March, 2000, the NASDAQ peaked at 5040, then began to fall. It has never recovered. I thought at the time that the AOL/Time Warner merger was the poster child of the NASDAQ mania, and so it proved to be. The FED today is making short-term debt look like a more reasonable place to be than the U.S. stock market. It keeps announcing that short-term rates should rise, implying that it will enforce tighter monetary policy to achieve this result. The federal finds rate promptly rises. The banks are being put in a squeeze. They must now pay more to depositors to get the money they use to loan to credit card debtors. This is another component of the squeeze on bank profits. Not only will they see their asset base facing new resistance because of higher risk to borrowers (the bankruptcy law), they will have to pay more to depositors. Conclusion The new bankruptcy law will backfire on the banks. They asked Congress to intervene and change the law. Instead of adjusting contracts or imposing new policies through competitive action, the banking industry asked for the state to intervene and change the rules. This was done in order to protect the banks. What we are likely to see, beginning early next year, is another case study of Ludwig von Mises' observation: whenever the government intervenes into the market in order to achieve a specific goal, a result opposite to the official justification for the intervention will occur. *** Taming the Mini-Futures Trading the S&P futures with a stop-loss of one point or less? Come visit our archives to see how it's done. You can get a free one-day pass to visit the site, or a two-week trial subscription with no risk, by clicking here. Rick Ackerman 321gold Inc |