Volume 8 Issue 1

From Greece to America

Acamar Journal

Aug 1, 2011

The crisis in Greece is not so much about

Greece, which is irrelevant in the greater scheme of things (at

2% of the EU economy). It is about the German, French and British

banks and the consequences if Greece defaults, followed by Ireland,

Italy, Portugal and Spain (the infamous PIIGS).

These countries will default on their

sovereign debt; it's just a question of when. The ratings agencies

were late to the game again but are now relentlessly downgrading

PIIGS debt, making the solution more difficult.

Creditors worldwide had a combined direct

exposure to the PIIGS of almost $2.4 trillion, according to the

Bank for International Settlements, as at Dec 31, 2010.

To put this in context, the total profits

of all the EU banks for the six months ended June 2010 were just

€46.8 billion while total equity was €1.8 trillion,

according to European Central Bank data.

In a surprising turn of events, US banks

also have significant exposure to the PIIGS debt, as they have

sold a substantial amount of Credit Default Swaps (CDS) to European

banks. Yes, those CDS made infamous by the housing bust, which

brought down AIG and other financial institutions during the

financial crisis, after which taxpayers were forced to bail out

Wall Street.

CDS are essentially insurance policies

against debt defaults by the PIIGS and the US banks are betting

that there will not be a default in the near-to-medium term or

at all (in which case, they would pocket the premiums on the

CDSs with no liabilities). This is, I believe, a spectacularly

poor bet and the Europeans have happily laid off some of their

exposure to these US banks.

Thus, while Bank of America only has

$500 million of direct exposure to Greece, it has collected over

$9.1 billion in CDS premiums covering the PIIGS by the end of

2010 (which means it has several multiples of potential liability

against such premiums).

Source:

BIS report, June

2011

Source:

BIS report, June

2011

and Betting

on the PIGS

US creditors (primarily US banks), which

own only 7% of debt directly, are on the hook for up to 42% of

all indirect exposure, in case of default and contagion.

In addition, the European Central Bank

is itself highly exposed to the PIIGS debt, which it took from

European banks, just as the Federal Reserve took toxic assets

off US banks. Both have become highly leveraged, with assets

in the range of 15-20 times their capital.

You have to feel for the Germans. Having

tried militarily to conquer Europe twice in the last century,

this time they tried to dominate it economically. Their intention

may even have been honourable: economic integration and the free

movement of people and trade to help prevent the endless wars

Europe has seen throughout history.

Their attempts to bring Europe together

into a common market allowed countries like Greece to tap into

capital markets at virtually the same rates of interest as the

Germans, with just a 20 basis point spread on 10 year bonds.

Greece took on far more debt in an era

of easy money than it could afford to pay back, with the government

now so bloated that it accounts for 46% of GDP. The long-term

solution is cutting back on government spending through

austerity measures, despite the riots. But this not only causes

pain through high unemployment and reduced government services,

it worsens the problem in the medium term.

It is the high debt/GDP ratio that forced

the crisis. Austerity measures require government to reduce spending,

which shrinks GDP. This makes the debt/GDP ratio worse, precipitating

more calls for cutting spending. It is a vicious downward cycle,

as shown by Greece's first quarter GDP which fell 5.5%.

Now the spread between Greek and German

10 year bonds is 1,400% and its unemployment rate is 16.2%! And

their public assets are to be privatised at fire sale prices.

Goldman Sachs helped make this excess

possible, by helping to hide the level of debt that Greece took

on when capital ran amok. But the average Greek, young and old,

will pay a severe price for this chicanery. Unemployment is projected

at between 17% and 23%, by the end of 2011. And, as GDP falls,

many small businesses with less than five employees (which accounts

for 97% of all registered business) are failing. 60,000 of them

(out of 960,000) went out of business in 2010.

The food banks already cannot feed all

the people in their line-ups and hungry people of all age groups

are turned away. Unemployment benefits, at less than €500

per month, run out after one year and there is no safety net

after that. A large segment of the population is being driven

into grinding poverty.

The EU experiment itself is being severely

tested. The Danish Parliament has now passed legislation introducing

permanent customs controls, in violation of the Schengen Agreement.

They first justified this as necessary to prevent eastern European

gangs wreaking havoc in Denmark, then changed the reason to the

need for tariffs. I suspect the real motive may be to intercept

economic refugees fleeing high unemployment rates from the PIIGS

countries.

Ironically the German people anticipated

a north-south divide in the EU. I reported in the Acamar Journal

in

June 2008 that, before the worst of the crisis, 59% of Germans

polled said they did not trust the Euro and were swapping Euros

printed in Greece and other countries for those printed in Germany.

When the consumer and corporate debt

crisis came in 2007-2008, it was massive government intervention

that saved the global financial system. But governments took

on unprecedented levels of debt and the next major crisis will

arise from a sovereign debt default(s).

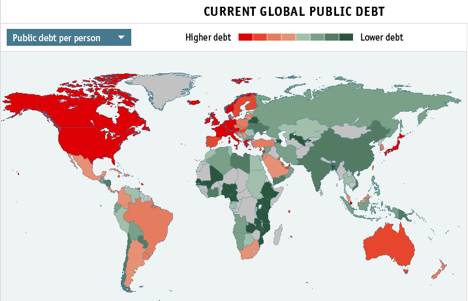

The problem is not limited to the EU,

as the chart below from The Economist shows.

The debt problem lies fundamentally with

the EU, North America and Japan. Conventional wisdom holds that

a debt level over 100% of GDP is a tipping point. While Greek

debt was 130% of GDP at the end of 2010 according to the IMF,

Japan was 225%. Germany came in at 74%, France at 84%, Britain

at 77%, Canada at 81%.

The US debt/GDP ratio stands at 93%.

But the problem the Western developed countries face is a demographic

one. Their populations are aging at a dramatic rate and living

longer.

While US debt is currently $14 trillion,

Professor Kotlikoff at Boston University estimates that the fiscal

gap is 15 times worse, at $202 trillion. In a Bloomberg opinion

piece titled "US

Is Bankrupt And We Don't Even Know It" he says that

the unfunded liabilities are simply unsustainable. It would take,

for instance, a doubling of taxes to close the fiscal gap, or

massive cuts to Medicare and Social Security.

So while the US government faces enormous

political pressure to deal with its deficits (the next showdown

in the US will be the August 2 deadline to raise the debt ceiling),

Americans have generally not saved up for retirement.

In a March AP poll, 24% of US baby boomers,

who began to retire last year, have no savings and say they will

have to work till they die. Of the remaining 76%, only half have

saved more than $100,000.

64% of boomers see Social Security as

a keystone of their retirement earnings. But Social Security

is already paying out more than it receives in contributions

and its trustees expect it to run dry in 2036.

In Homer's epic poem Odyssey, Odysseus

and his crew have to navigate between Scylla and Charybdis,

two dangerous sea creatures that lay on either side of a narrow

strait. The end result is that he barely survives but loses his

men and ship in those dangerous waters. The developed countries

are caught between the dangers of potential sovereign debt default

if deficits are not reduced and populations heavily dependent

on ever-expanding unfunded liabilities, which are rioting in

protest as governments make painful budget cuts.

I took a year-long break from writing

the Acamar Journal, waiting to see if the lessons from the financial

crisis that I had predicted had been learnt. They have not.

Wall Street has passed on its losses

to the taxpayers and is back to taking substantial risks and

paying outrageous bonuses. The US Government is being lobbied

to continue to transfer wealth from the middle class to the rich

and is dramatically eroding civil rights. The European countries

are trying to shield bondholders from the consequences of their

improvident lending in yet another round of "privatised

gains, socialised losses."

The pain imposed on the Greeks will become

untenable and Greece will default at some point. The Greek riots

may be a prelude of things to come in other developed countries.

There is a real danger that there will be another, deeper financial

crisis. The danger with a deep economic crisis, apart from the

direct economic pain, is that it may spawn authoritarian regimes

as people demand solutions at all costs. It will be truly ironic

if the country that was the cradle of democracy helps initiates

such a reversal.

###

Acamar Journal

Disclaimer

The

Acamar Journal is intended to provide factual and timely research

on general economic trends, opinions about trends in specific

industry sectors, information on specific companies, references

to other publications and reports that may be of interest to investors,

and information on general trading strategies. Zabina Ventures

Inc. ("Zabina") is not a registered investment dealer

or adviser.

Although the

statements of facts in this report have been obtained from and

are based upon sources Zabina believes to be reliable, we do not

guarantee their accuracy, and any such information may be incomplete

or condensed. All opinions and estimates included in this report

constitute Zabina's judgment as of the date of this report and

are subject to change without notice. Zabina makes no warranties,

express or implied, as to results to be obtained from use of information

in this report, and makes no express or implied warranties of

merchantability or fitness for a particular purpose or use.

This report

is for informational purposes only and is not intended to be advice,

or an offer or a solicitation with respect to the purchase or

sale of any security. This report does not take into account the

investment objectives, financial situation or particular needs

of any particular person. Investors are advised that investing

in securities entails certain risks, and they should obtain individual

financial advice and undertake extensive due diligence based on

their own particular circumstances before making any investment

decisions.

Zabina may from

time to time perform corporate communications or other services

for companies mentioned in this report. Zabina and/or its principals

may be compensated for such services, in the form of fees and/or

options. In addition, Zabina or any individuals preparing this

report may at any time have a position in any securities or options

of issuers mentioned in this report. Directors, shareholders or

employees of Zabina may be a director or officer of officer of

a company mentioned in this report.

Copyright ©

2004-2011. All rights reserved.

Visit:

www.acamaronline.com

for a unique perspective on global economic events!

321gold Ltd

|